What’s coming next

Nicolò Miscioscia, Partner, Head of Private Markets and Digitalisation, Co-Manager DECALIA Private Credit Strategies

An analysis of insiders‘ pulse

- Explicit alarm: voices warning of systemic risk

- Defensive reassurance: statements that, read carefully, contain their own warnings

- Observable actions: what the money is doing, not saying

What the market thinks

- Public market data points that unveil investors feelings

- And semi-liquid vehicles allow the same observation in private markets

Conclusion

- Assessing the systemic risk of a private credit collapse

- What is the investor’s „true north“ in this environment

Much has been written in recent years about private credit. The debate first focused on its merits; more recently, it has shifted toward predictions of imminent disaster. This emotional swing has left investors uneasy and hesitant. Whether they have only just built an allocation, are still in the process of doing so, or are considering where to begin, many are asking the same question: and now, what?

This paper aims to assess how worried investors should be. Is the current stress simply part of a market cycle, or could it mark the beginning of something more systemic? It also seeks to offer practical clues about what should come next. To answer those questions, we draw on the words and actions of the best-informed participants in the market. Their behaviour often reveals more than public data. These are people with access to credit information across hundreds of billions of dollars of portfolios, direct relationships with thousands of borrowers, and the institutional memory of every credit cycle of the past thirty years. When they act – or when they speak with unusual candour – investors would do well to listen.

We group the evidence into three categories: 1) explicit warnings, 2) reassuring statements that nonetheless contain warnings of their own, and 3) observable actions taken by major firms. Read together, these signals produce a coherent picture. The best-informed participants in private credit are not panicking. They are not calling for emergency intervention and, with few exceptions, they are not predicting an imminent catastrophe on the scale of 2008. Yet they are almost uniformly concerned, and across the spectrum from bears to bulls they are positioning their portfolios in ways that suggest the problem is real.

Explicit Alarm: Voices Warning of Systemic Risk

Jamie Dimon, CEO, JP Morgan Chase, has been the most prominent and consistent external critic of private credit risk among senior banking executives. Over the past eighteen months, his warnings have grown both more frequent and sharper. In his annual shareholder letter published in early April 2026, Dimon identified deterioration in private credit as one of the three compounding risks facing markets heading into the second half of 2026, alongside war-driven inflation and the uncharted disruption of AI. In Q4 2025, following the bankruptcies of First Brands and Tricolor (a client of JP Morgan), Dimon publicly deployed his now-famous „cockroach“ metaphor: „When you see one cockroach, there are probably more“, explicitly arguing that the opacity of private credit means that what is visible likely represents only the leading edge of a broader deterioration.

His language deserves close attention. He argued, first, that credit quality has already begun to erode; second, that actual losses in leveraged lending are running ahead of what current market conditions would normally imply; and third, that because loan valuations lack the discipline and transparency of public markets, investor exits can begin well before any clear deterioration is visible in reported credit performance.

At the level of individual instruments, Dimon is openly concerned. At the systemic level, he has been more cautious – while still warning against complacency in the observation, „We have not had a credit recession in a long time, and it seems that some people assume it will never happen“.

Jane Fraser, CEO, Citigroup, has been more explicit in describing private credit risk as potentially systemic. Her framing comes closest to the pre-2008 analogy: when $1.7 trillion sits in a market with limited mark-to-market discipline and no centralised clearing, the possibility of correlated losses becomes real. Fraser also pointed to the interaction of three risks – opaque credit markets, geopolitical instability (Iran), and AI-driven technological disruption – as factors that could amplify one another in ways standard risk models are not designed to capture.

Former Goldman Sachs chief executive Lloyd Blankfein told that a liquidity mismatch had become more likely after such a long period without a major credit market crash. „When something goes off you’re going to find all the assets that have been carried at prices that can’t be realised in the market“.

Professor Edward Altman, NYU Stern School of Business, creator of the Z-Score credit default prediction model and one of the most rigorous academics working on credit risk, has also issued persistent warnings. His core concern is that headline default statistics are not merely incomplete but structurally misleading. Because private credit restructurings are bilateral, distress can be absorbed and hidden in ways that are not possible in public markets, where mark-to-market discipline is unavoidable.

Senator Elizabeth Warren, US Senate, is a political actor rather than a market participant, but her comments matter for a different reason. She referred to Blue Owl’s gate as the first visible sign of a much larger structural problem, signalling that private credit had crossed the threshold into political attention.

Historically, once financial-market stress reaches this level of visibility, regulatory action becomes far more likely.

Defensive Reassurance: Statements That, Read Carefully, Contain Their Own Warnings

The second category of signals is perhaps the most analytically interesting. The largest private credit managers have defended the asset class publicly, yet their choice of arguments, their acknowledgement of specific risks, and the contrast between their public statements and private actions tell a less reassuring story.

Marc Rowan, CEO, Apollo Global Management, is one of the clearest examples. Since late 2025, Rowan’s public positioning has followed a deliberate two-track strategy: an aggressive public defence of private credit as an asset class, combined with a quieter but systematic reduction of risk at portfolio level. He described investor concerns about systemic risk as „lost their minds“ territory. He wrote a Bloomberg op-ed setting out what he called the „four myths“ of private credit. He also announced a forthcoming book intended to define the asset class conclusively.

Privately, however, according to the FT’s December 2025 reporting from those present at Goldman Sachs investor meetings, Rowan’s message was markedly different. His „number one job“, he said privately, was to „have the best balance sheet possible“ so as to be positioned for when „something bad happens“. Those words have since been matched by tangible actions, described below.

The significance of this divergence is difficult to miss. Rowan’s public messaging reflects the obligations of a manager who must maintain client confidence, defend his firm’s franchise, and prevent redemption contagion. His private messaging, and the portfolio decisions that followed, suggest someone who genuinely believes risk has risen to an uncomfortable level and is using the remaining time to position defensively.

Steve Schwarzman, CEO of Blackstone, has taken the most aggressive public line in dismissing concerns. He argued that the bankruptcies that triggered market alarm were „misinformation“; that they were bank-led transactions rather than private credit; that Blackstone’s own default rate is only 0.3%; and that private credit is „actually much more conservative for the system“ than banks, which are leveraged 10:1. He framed the recent failures as cases of fraudulent collateral pledging – operator failure rather than structural weakness.

Yet Blackstone’s Q1 2026 experience with BCRED points in another direction. When $3.8 billion – 7.9% of the fund – was requested for redemption in a single quarter, Blackstone took the extraordinary step of raising $400 million from its own capital base and senior executives in order to satisfy those requests in full. This was not the behaviour of a firm confident that its retail credit product was functioning normally. It was a crisis-management response to a redemption spike that, had it gone unmet, might have triggered a broader panic.

Jon Gray, President, Blackstone, adopted a more nuanced public tone than Schwarzman. He acknowledged that lower-leveraged loans represent „a pretty good place to be“ – an implicit admission that more highly leveraged loans are less attractive. He also defended the structure of semi-liquid products with redemption caps as „a feature, not a bug“. Yet that argument is itself revealing when made in defence of a product whose cap has just been breached.

Howard Marks, Co-Chairman of Oaktree Capital Management, has offered the most intellectually careful and, taken together, the most balanced interventions. He explicitly acknowledged that the First Brands and Tricolor failures revealed investor „complacency and carelessness“. He wrote that „the coming period is likely to be more ‚interesting,‘ as errors that were made in those good times come to light“. He also affirmed that „it’s great to hold public debt that can be exited more readily if you sour on the credit“ – a direct concession to liquidity risk. Still, he stopped short of calling the troubles systemic: „No, I don’t think this is necessarily the beginning of a trend. It’s not an indictment of the whole sub-investment grade debt market or the whole private credit market“. His recommendation – to combine public and private credit – is the portfolio advice of someone who still sees opportunity in private credit, but not without meaningful constraints.

What Marks has not said publicly may be just as important as what he has. Oaktree has raised substantial capital for distressed debt strategies in 2025 and 2026 – over $100 billion in the sector across all managers, according to Within Intelligence. Distressed specialists raise capital in anticipation of stress, not after the fact. Oaktree does not raise distressed funds because it expects everything to be fine.

Alan Schwartz, Executive Chair of Guggenheim Partners, a $350bn private asset manager, said „there are cracks in the foundation of private debt market. Any time you get increased selling in illiquid assets that don’t have transparent valuations, it can cause significant spams in financial markets“. However, he then added that the „excesses in the market don’t look as deep and systemic“.

Observable Actions: What the Money Is Doing, Not Saying

Statements matter, but the actions of informed insiders matter more. The clearest signals come from what sophisticated participants are actually doing with their balance sheets, portfolios, and capital raising.

Apollo: Halved CLO exposure at Athene ($40bn -> $20bn). Purchased tens of billions in US Treasuries. Rapidly reduced software loan exposure. Running flagship fund at 0.58x leverage, below peers and prior periods. Actively cutting leveraged loans.

Blackstone: Committed $400 million of firm and senior executive capital to fully satisfy BCRED redemptions in Q1 2026 – an explicit balance-sheet intervention to defend fund stability. Pivoting marketing and capital deployment toward infrastructure and data centres (where loans are secured against hard physical assets) and away from software buyout lending.

JPMorgan: Cut off Tricolor’s warehouse facility, triggering its failure. Initiated structured products allowing clients to short private-credit-exposed asset managers – a trade with positive expected value only if the bank expects stress to materialise.

CalPERS, OMERS (large pension funds): According to reports, acted as „rescue capital“ providers into the Blue Owl situation – purchasing loans at a discount from the gating vehicle. The fact that these institutions were buying at a discount implies they believed there was a discount to be had – in other words, that stated valuations were above the price they were willing to pay.

Distressed debt funds broadly: According to Within Intelligence, distressed and opportunistic credit funds raised over $100 billion in the two years to Q1 2026. Apollo, Ares, Oaktree, Cerberus, and others have built or are actively deploying dry powder for distressed situations. Distressed capital is raised in anticipation, not reaction. The scale of this fundraise is one of the most revealing signals in the entire dataset.

Barings Private Credit Corp: Capped withdrawals at 5% in Q1 2026 after redemption requests surged to 11.3% of shares. This is not a manager acting defensively out of excessive caution; it is a manager responding to investor behaviour that has already moved beyond the normal range.

BlackRock: Restricted withdrawals from its $26 billion HPS Lending Fund in early March 2026 – the acquisition of HPS Investment Partners by BlackRock, completed in late 2024, was specifically intended to expand BlackRock’s private credit franchise. That the flagship fund of this acquisition is now gating within 18 months of completion is a striking development.

Morgan Stanley North Haven Private Income Fund: Received repurchase requests for 10.9% of shares – the highest level across any fund in this survey. As of the time of writing, this is one of the clearest quantitative signs that retail investor sentiment on semi-liquid private credit has shifted decisively.

What the Market Thinks

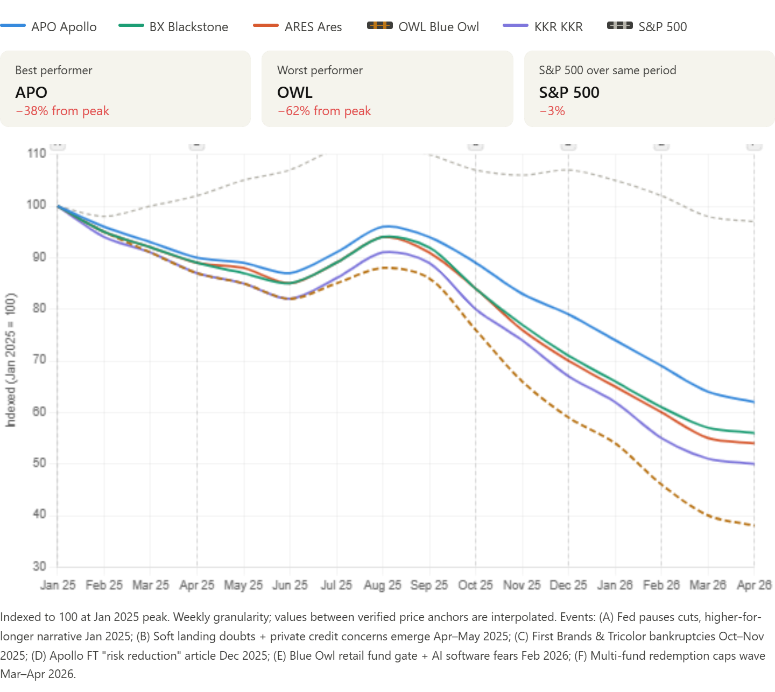

The concerns are shared by general market participants, as evident from their defensive actions. The major publicly traded alternative asset managers have suffered extraordinary destruction in market value from their peak levels to Q1 2026: Apollo down approximately 41% from peak, Blackstone 46%, Ares and KKR 48% each, and Blue Owl roughly two-thirds. Together, that amounts to more than $265 billion of erased market capitalisation. These are institutions valued in liquid markets with full access to SEC filings, BDC performance, and fund structures.

The shareholders selling these stocks are not simply retail investors reacting to headlines; they are predominantly institutional investors supported by sophisticated analytical teams. They are not selling because of „misinformation“. They are selling because the evidence available to them suggests that the earnings trajectories of these businesses are under meaningful pressure.

Stock prices are imperfect and can be wrong. But when liquid markets erase $265 billion from the leading participants in a $3.5 trillion asset class, while those same participants are restricting withdrawals, cutting risk, and raising distressed capital, the likelihood that concerns are merely perceptual rather than grounded in fundamental deterioration appears vanishingly small.

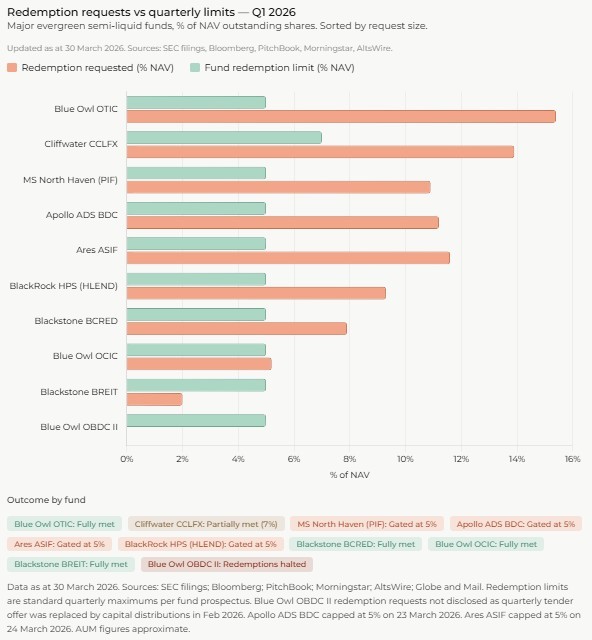

Similar to public markets, we are observing a selling wave in private semi-liquid vehicles. In our precedent publication „Easy Entry, Hard Exit“ published in March 2026, we have analysed the series of redemption requests placed by investors in these vehicles. The following is an updated graph as at the end of Q1 2026, showing the redemption requests vs fund redemption limits.

The same selling spree is visible both on public and private markets, with the additional complexity that semi-liquid vehicles, which are not marked-to-market daily, do not allow to see the economic level of mistrust that investors place into those portfolios.

Conclusion

Sophisticated market participants generally appear to exclude a systemic risk on the scale of 2008.

Among the many FT articles on the subject, one provided especially detailed and revealing data. The Office of Financial Research – the arm of the US Treasury Department tasked with promoting financial stability through the collection, standardisation, and publication of financial data – estimated banks‘ and non-bank financial institutions‘ lending exposure to private credit funds at up to $540bn. Large as that figure may sound in absolute terms, it remains small relative to the $33tn and $94tn of assets held by banking and non-bank financial institutions respectively. A major impairment in private credit would clearly have consequences, but on these figures the exposure does not appear large enough to bring down the financial system even if events deteriorate sharply.

If there is broad agreement on that point, there is near-unanimity on another: the condition of the private credit market is a cause for concern. Managers may continue to reassure the market in public, but they are also reshaping portfolios defensively and preparing to profit from a wave of distressed opportunities.

As always, the roots of any bubble lie in fundamentals: the core issue here is credit quality. The deterioration appears to stem from the sheer amount of capital the industry has accumulated – and the pressure that capital created to be deployed. That pressure weakened terms, compressing returns, and eroding security packages. Oaktree’s Howard Marks says „I imagine some direct lending managers accepted too much money and invested it too fast, applying standards that were too low and setting the scene for a correction“.

For investors, credit quality must remain the true north. In the search for it, it is also essential to recognise that the oversupply of money is concentrated primarily in the sub-set of private credit generally labeled „direct lending“, i.e. loans to private-equity-backed companies: this represents roughly 75% of the global private credit market, whereas private credit is a much broader and more heterogeneous asset class, spanning sponsored and sponsor-less corporate loans, asset-backed strategies, specialty finance, infrastructure debt, and more.

Although these areas require more sophisticated origination and underwriting capabilities, they still offer room to find genuine credit quality. Indeed, the current volatility may create the conditions for a prolonged period of higher-quality credit opportunities ahead.

Sources for this supplementary analysis include: Financial Times (December 22, 2025), Fortune (March 14, 2026), CNBC (March 5, 2026), Bloomberg (various, November–December 2025), Morningstar (March 2026), Howard Marks / Oaktree Capital – „Cockroaches in the Coal Mine“ memo and „Gimme Credit“ memo (October–November 2025), JPMorgan Chase Annual Shareholder Letter 2025 (published April 2026), InvestmentNews (April 2026), HedgeCo Insights (February 2026), WebProNews (February 2026), Within Intelligence Private Credit Outlook 2026, Reuters (December 2025), Yahoo Finance / Apollo (December 2025), Puck (November 2025).

Copyright © 2026 by DECALIA SA. All rights reserved. This report may not be displayed, reproduced, distributed, transmitted, or used to create derivative works in any form, in whole or in portion, by any means, without written permission from DECALIA SA.

This material is intended for informational and marketing purposes only and should not be construed as an offer or solicitation for the purchase or sale of any financial instrument, or as a contractual document. The information provided herein is not intended to constitute legal, tax, or accounting advice and may not be suitable for all investors. The market valuations, terms, and calculations contained herein are estimates only and are subject to change without notice. The information provided is believed to be reliable; however DECALIA SA does not guarantee its completeness or accuracy. Past performance is not an indicator of future results.

Some of the information presented in this paper is based on the direct experience of DECALIA as manager of collective investment schemes such as DECALIA Private Credit Strategies. Any intended or implicit reference to DECALIA Private Credit Strategies is not meant to represent a solicitation for the purchase or sale of the strategy or other strategies of DECALIA. Private markets strategies are not destined to the large public and its suitability must be evaluated in relationship to the risk profile, objectives and financial situation of any investor and the rules and limitations of each jurisdiction.