In the mid-2000s, the figure of the “Polish plumber” became a powerful symbol in the French and UK public debate, embodying fears linked to globalization and the enlargement of the European Union. An estimated two million workers from Eastern and Central Europe arrived between 2003 and 2007 in the UK, half of them were Polish. The stereotype of the Polish plumber was cited as a factor in the referendum that led to the withdrawal of the UK from the EU. Twenty years later, this image deserves to be reversed: far from representing a social threat, Poland now stands as one of the most remarkable economic success stories on the continent. Its trajectory, marked by rapid convergence with Western Europe, can rightly be described as a “revenge.”

Since joining the European Union in 2004, Poland has experienced sustained and steady economic growth. Over the long term, its GDP has increased dramatically, rising by roughly 170% over two decades. More recently, the momentum has remained strong, with growth reaching around 3.6% in 2025, compared to just 0.8% in France. The contrast is equally striking with the United Kingdom, where growth since 2010 has been widely described as lackluster and constrained by weak productivity. Poland has thus distinguished itself through its ability to maintain a faster pace of expansion than major Western economies.

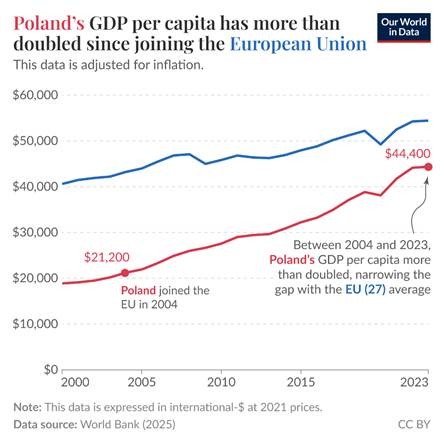

Poland vs. EU GDP per capita: catching up fast

The catch-up is even more visible in terms of living standards. Poland’s GDP per capita, which was less than half the European average in the early 2000s, now exceeds 80% of that average. The gap remains, but it has narrowed considerably. In purchasing power parity terms, convergence is even more pronounced, with GDP per capita exceeding $44’000 in 2024. In other words, Poland is no longer a “low-cost” economy, but a country approaching Western standards of living.

Labor market performance is equally noteworthy. For several years, Poland has maintained a low unemployment rate, often below that of France, where unemployment remains structurally high. This improvement reflects successful industrialization, an upgrading of the productive base, and effective integration into European value chains, particularly those centered on Germany. By contrast, the United Kingdom continues to face persistent challenges related to productivity and job quality.

Public finances provide another revealing point of comparison. Poland’s public debt remains relatively contained, at around 65% of GDP, compared with 95% in the UK and over 110% in France. This relative fiscal discipline contrasts with the chronic imbalances observed in Western Europe. Similarly, Poland’s current account balance has improved over time, supported by industrial competitiveness and exports, whereas the United Kingdom frequently runs significant external deficits.

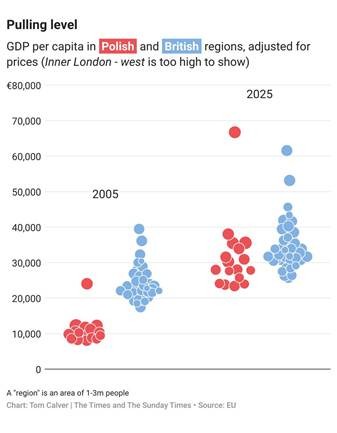

Poland vs. UK GDP per capita… tables have turned 20 years later

According to an article from the Times (November 2025), 12 out of 17 Polish regions are now richer than West Wales. It has faster internet, cheaper electricity and more high-speed rail than Britain. When it comes to regional development it’s the UK, France and other European major economies, not Poland, that need to catch up now…

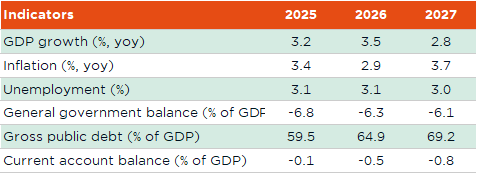

Admittedly, Poland is not without vulnerabilities. Inflation has been more volatile in recent years (it spiked close to 20% at the beginning of 2023 before receding to 3% more recently), and the country faces significant demographic challenges, particularly rapid population aging. Yet these limitations do not overshadow the broader trend: a fast-growing economy that has successfully leveraged European funds, trade openness, and internal reforms into sustained growth.

Poland Key Economic Indicators

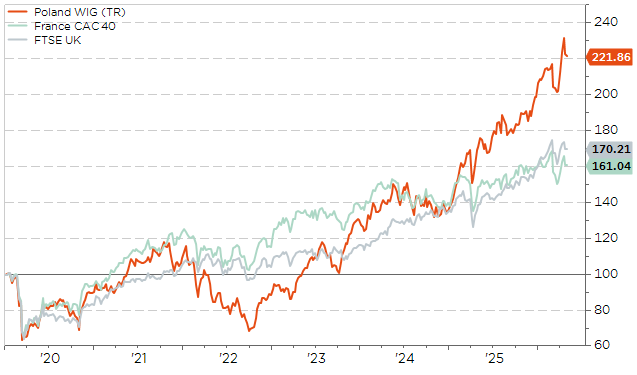

Finally, financial markets also reflect this transformation. Polish equities have benefited from domestic growth and foreign investment inflows, delivering attractive long-term performance, often outpacing that of more mature and less dynamic economies.

Total Returns in EUR of Poland WIG, France CAC40 and UK FSTE (rebased at 100 on 31.12.2019)

The “revenge of the Polish plumber” is not merely a provocative phrase, but a reflection of a genuine shift. In one generation, Poland has moved from the economic periphery to becoming a central driver of European growth. While France and the UK still enjoy higher levels of wealth, their relative dynamism now appears less impressive. This reversal highlights a fundamental lesson: in the global economy, hierarchies are never fixed, and convergence can happen quickly when the right political, economic, and institutional conditions are in place. Another deeper lesson is that “low-cost worker” can become tomorrow’s contributor to prosperity, provided the broader economic environment allows for upward mobility and integration as it has been the case in both Switzerland and the US over the last two centuries. So, there is a second lesson of the Polish plumber: those you fear today may be the ones who power your prosperity tomorrow.

This is the original humorous poster from the Polish tourism board in 2005, using the Polish Plumber stereotype, to invite the French to come visit Poland.

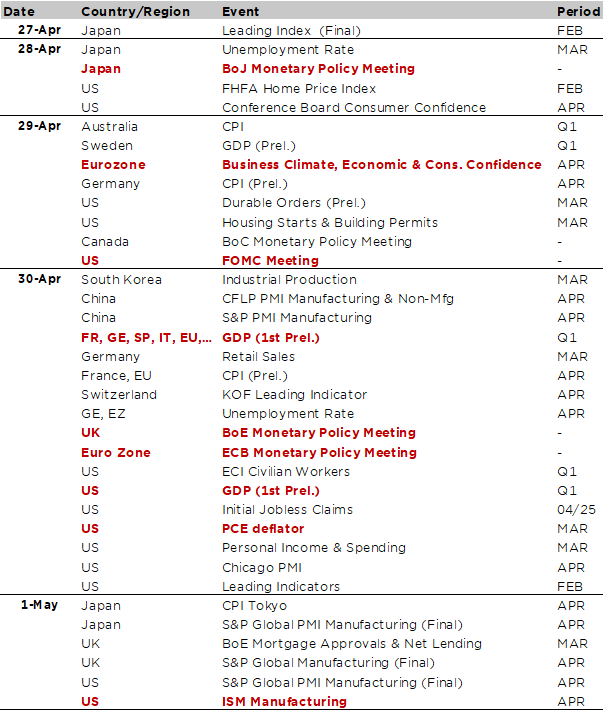

Economic Calendar

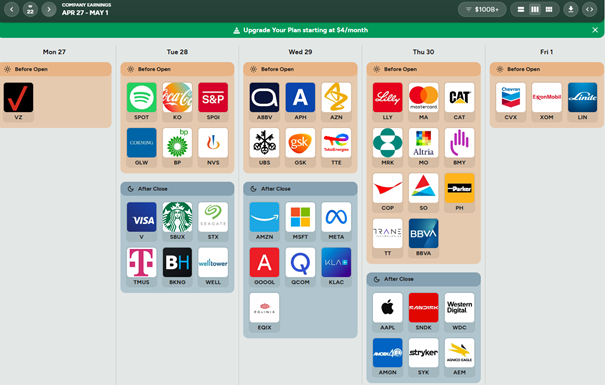

Despite the ongoing cacophony surrounding the Iran conflict and the theorical re-opening of the Strait of Hormuz after two months of conflict (Iran offered a proposal to the US last night to reopen the strait and end the war but without putting their nuclear capabilities on the negotiations table), markets will likely be less sensitive to geopolitical distractions going forward, bar an unexpected major escalation or strong deal peace. Indeed, this week agenda will be busy and packed enough to divert investors mind and focus to more fundamental macro and micro stories as we will get big five central bank meetings and companies results, including the Fed (Wednesday), the ECB and the BoE (Thursday) as well as the BoJ (Tuesday); the Q1 GDP estimates for the US and Europe (Thursday) along with some inflation gauges releases (Wednesday and Thursday); and a very busy schedule for corporate earnings with 44% of the S&P500 market cap reporting next week (Alphabet, Microsoft, Amazon, Meta and Apple are scheduled to release results)

As far as monetary policies are concerned, the consensus expect no change (hold from the BoJ, BoC, Fed, ECB and BoE at 0.75%, 2.25%, 3.5%-3.75%, 2.0% and 3.75%, respectively) but the statements, press conferences and Q&A following the decisions will be scrutinized to get some insights on the rate trajectories over the next few months. Worth also to mention that it will likely be Jerome Powell last dance as Fed Chairman because the Senator Thom Tillis agreed finally to lift his block on Kevin Warsh’s nomination to chair the Fed yesterday due to the DoJ’s decision late last week to drop its investigation into the Fed refurbishment (or eventually re-open it at a later stage).

Moving to economic data, the key US releases will include the first estimate of Q1 GDP on Thursday along with the March PCE deflator. The consensus expects real GDP growth at an annualized pace of +2.1% (+0.5% in Q4 2025) and forecasts a +0.3% MoM advance in the core PCE (+0.4% in February), which should push YoY increase to 3.2% from 3.0%. We will get also the Conference Board consumer confidence on Tuesday and the April ISM manufacturing index on Friday (our model forecasts a further increase to 57.1 well above the consensus, which foresees a more modest uptick to 53.0 from 52.7). In Europe, the focus will be the advance Q1 real GDP growth data in the main economies (Thursday), as well as the flash April CPI, with Germany and Spain among countries releasing the data first on Wednesday. To wrap up with corporate earnings, 44% of the S&P500 by market cap is due to report next week, with half of that on Wednesday (Alphabet, Microsoft, Amazon and Meta) and Apple following on Thursday. Earnings will be due from several other important tech firms, but also oil majors such as Exxon, Chevron, BP and Total, and plenty of other industry leaders (Coca, Novartis, Visa, Starbucks, Lilly, CAT, BBVA, Linde).

https://earningshub.com/earnings-calendar/week-of/2026-04-27

This is a marketing communication issued by DECALIA SA. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The information and data presented in this document are not to be considered as an offer or invitation to buy or sell any securities or financial instruments nor to subscribe to any services. The information, opinions, estimates, calculations etc. contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Investments in any securities or financial instruments may not be suitable for all recipients and may not be available in all countries. This document has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Before entering into any transaction, investors should consider the suitability of the transaction to individual circumstances and objectives. Any investment or trading or other decision should only be made by the client after a thorough reading of the relevant product term sheet, subscription agreement, information memorandum, prospectus or other offering document relating to the issue of the securities or other financial instruments. Where a document makes reference to a specific research report, the document should not be read in isolation without consulting the full research report, which may be provided upon request.