While China is facing structural risks from the 3Ds of Debt, Demographics and Deflation as recently coined by Morgan Stanley, the macro backdrop could be defined as CCC with economic data sending Confusing and somewhat Contradictory messages in an overall still Challenging context. Let’s take the latest US data released on Friday. Beyond the upside surprise in the August payrolls print (187k vs. 170k expected), there were also weaknesses as past prints were revised once again lower (-110k in total for June and July), hourly wage growth slowed (+0.2% vs. +0.4% the prior month) and unemployment rate rose to 3.8% in August from 3.5%. In the same time, the US ISM manufacturing index came slightly above expectations, increasing last month to 47.6 from 46.4 with the prices paid component rebounding strongly to 48.4 from 42.6 (vs. 44.0 expected).

Is the US economy really experiencing a soft landing or will it end badly (excluding exogenous shock, hard landings always look like soft landing at the beginning…)? What about a reacceleration as suggested by the rebound in manufacturing activity? Especially if China news flow start improving. Are inflationary pressures definitively under control? What if energy and commodity prices rebound and/or USD weakens suddenly? Uncertainties about the future aren’t unusual but the current dispersion of macro outcomes remains remarkably large. In my views, it’s because this time -compared to previous cycles- we have to deal in a multi-dimension context (growth, inflation, monetary and fiscal policy), with two unsynchronized global growth engines (US and China), in the midst of major structural challenges (ageing population, energy transition, changes in globalization trends and flows, debt overhang) following uncharted events (pandemics, war and a decade-long of interest rates suppression). So, challenging may even be too weak in describing the current macro backdrop…

The both funny and scary aspect of this current confusion is that there is something for everyone, which also means there could be (nasty) surprises and (major) disappointments for the vast majority of soft-landing optimistic investors, including ourselves to some extent. While far from gloom & doom, our macro scenario still foresees a marked economic slowdown with lower inflation (but above central banks’ targets in the foreseeable future) leading to hawkish “hold” monetary policies. Hence, with no major correction for risky assets driving valuation back to more attractive levels and forcing central banks to adopt a more dovish stance expected anytime soon, we anticipate a continuation of the tug of war between restrictive monetary policy headwinds on the one hand and unusually resilient growth & sticky inflation on the other… until something eventually breaks. In other words, latent risks persist and are potentially growing under the surface. In this CCC context, some Cautiousness in terms of overall asset allocation, with a Counter-balancing all-terrain approach to portfolio construction, keeping also a Cash bucket as an uncorrelated volatility buffer, a “high and non-volatile” yield source and a dry powder if/when other assets valuations become more reasonable. Or you just get more Convictions.

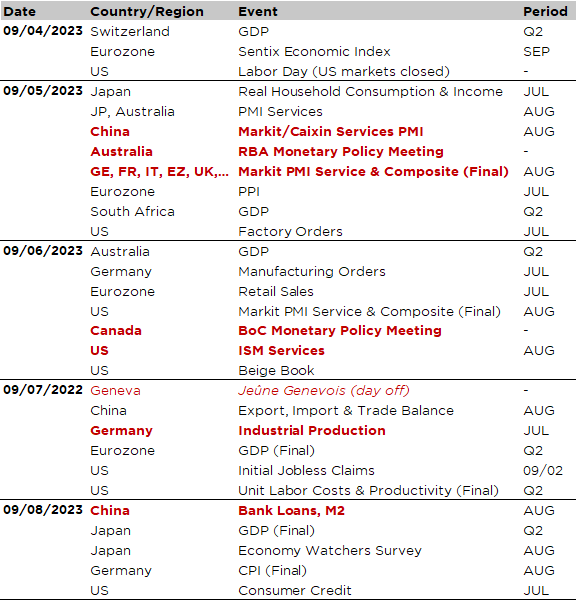

Economic Calendar

It will be kind of mix platter on this week’s menu with the releases of some important, but not really key, macro data from the major economies, as well as a few “second tier” central bank’s meetings. Starting with the US, the ISM services index for August (Wednesday) will likely be the main event. The consensus expects a stabilization of the ISM gauge around last month level (52.7), consistent with a moderate expansion in the services activity. On the same day, we will also get the Fed’s Beige book, which may confirm, after last week reassuring inflation and labor market data, that the Fed may stay pat when they meet again on September 20. Note also that there won’t be any releases today as US markets are closed for the Labor Day. So, it should be a quiet week ahead in the US as far as economic news are concerned.

Over in Europe, the focus will be on Germany with the release of manufacturing orders on Wednesday and industrial production for July on Thursday given the current downbeat sentiment surrounding euro area, and especially German, growth. After last week’s releases of sticky flash CPI prints for August, it may be worth keeping an eye as well on the Eurozone PPI reading for July (tomorrow), especially as this week set of macro data are the last ones before ECB meet on September 14.

Turning to Asia, both China and Japan will be under the spotlight. The former with the Markit/Caixin PMI services index for August (tomorrow) and the last month trade data (Thursday) in the hope to get some signs of growth stabilization through the exports-imports trends. In Japan, it’s more about a confirmation of the slow improvement of the growth backdrop accompanied by underlying reflationary pressures, which may convince the BoJ at some point to abandon the YCC and/or even hike rates eventually. In this context, August PMI services index, July household spending and income (both released tomorrow) and the latest economy watchers survey (Friday) will be scrutinized.

To conclude with monetary policy, the RBA and the BoC will meet tomorrow and on Wednesday respectively. They are both expected to keep their policy rates unchanged at 4.1% (RBA) and 5.0% (BoC), which may be interpreted as a prelude to what will happen the following weeks with the Fed (very likely) and the ECB (less likely in my views). The long list of ECB speakers throughout the week may also bring more insights about ECB’s next move(s). Finally, note also that the G20 Summit will kick-off on Saturday September 9 in New Delhi.

This is a marketing communication issued by DECALIA SA. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The information and data presented in this document are not to be considered as an offer or invitation to buy or sell any securities or financial instruments nor to subscribe to any services. The information, opinions, estimates, calculations etc. contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Investments in any securities or financial instruments may not be suitable for all recipients and may not be available in all countries. This document has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Before entering into any transaction, investors should consider the suitability of the transaction to individual circumstances and objectives. Any investment or trading or other decision should only be made by the client after a thorough reading of the relevant product term sheet, subscription agreement, information memorandum, prospectus or other offering document relating to the issue of the securities or other financial instruments. Where a document makes reference to a specific research report, the document should not be read in isolation without consulting the full research report, which may be provided upon request.

Unless specifically mentioned, charts are created by DECALIA SA based on FactSet, Bloomberg or Refinitiv data.