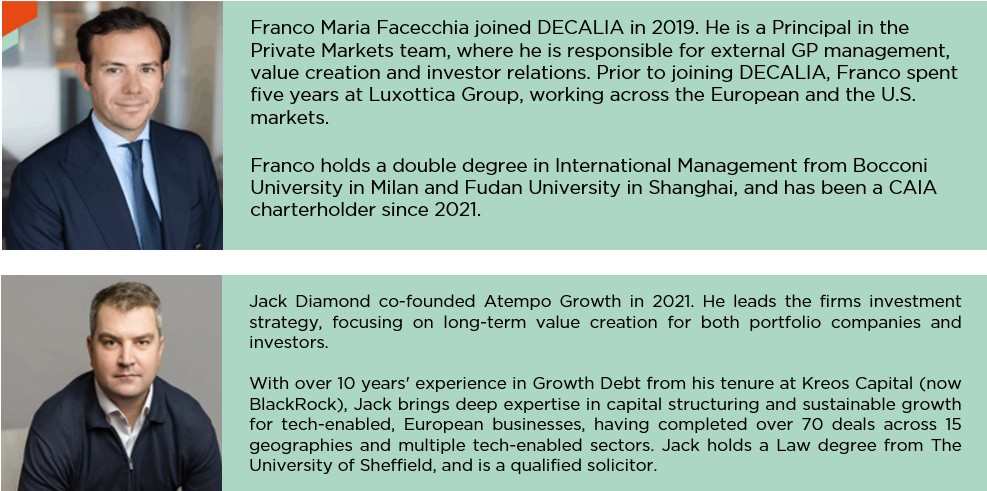

A conversation with Jack Diamond, Co-founder & Partner – Atempo Growth

Franco Maria Facecchia, Principal Private Markets – DECALIA

The ‘Software Apocalypse’ — how real is the AI disruption risk

- Private credit markets under stress in Q1 2026

European vs. us market

- Structural differences and insulation

Atempo growth portfolio positioning

- Atempo Fund I & II updates and key investor message

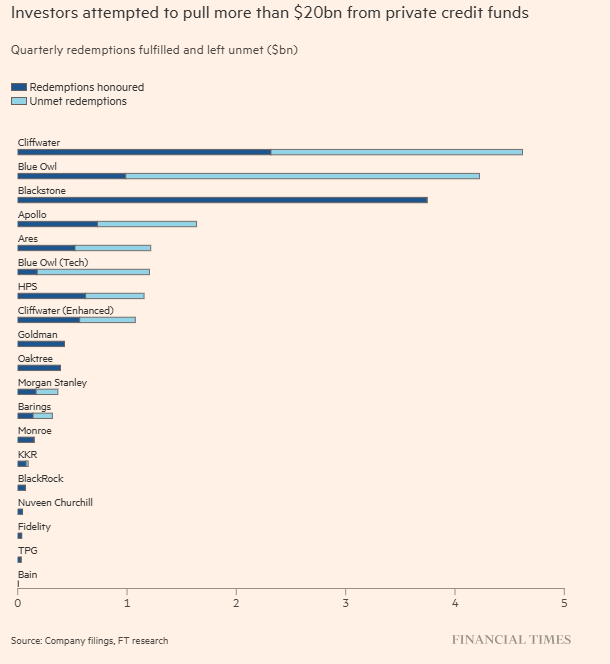

FF The private credit market has been under significant pressure in Q1 2026. Can you set the scene for us?

JD

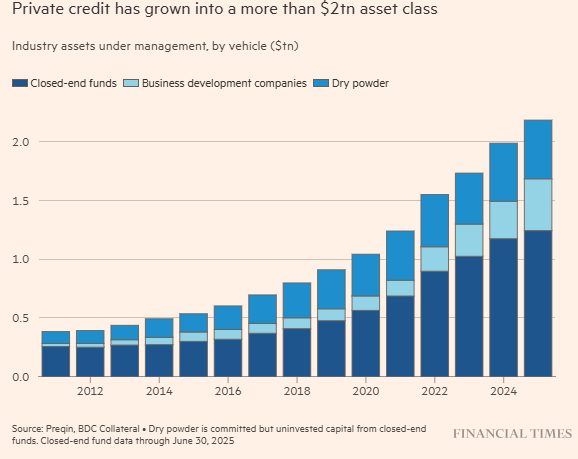

Global private credit is experiencing its first meaningful stress test since the asset class’s rapid expansion over the past decade, surpassing two trillion dollars in global AUM. In late 2025, the global private credit markets experienced a series of high-profile leveraged loan defaults, a sharp increase in payment-in-kind toggles, and rising amend-and-extend transactions to defer stress on weaker credits.

This came into sharp focus in early March 2026 when a major asset manager decided to mark down the value of its technology-related loan collateral. This single move sent shockwaves through the industry, triggering sell-offs in shares of major alternative asset managers and prompted a wave of elevated redemption requests across non-traded private credit funds.

In our view, the era of broad, beta-driven returns in private credit is over, validating the approach of managers who have been building with discipline and selectivity from the start. Not all private credit is created equal, and the current environment is making that distinction impossible to ignore.

FF A major part of the current stress seems concentrated in software. There is talk of a ‘Software Apocalypse.’ How real is this risk?

JD

The risk is real, but the label is overstated. What we are seeing is not an apocalypse, but a repricing of AI disruption risk in credit portfolios that were built on assumptions that may no longer fully hold.

Software has been a cornerstone of private credit, representing roughly twenty per cent of overall exposure and around seventeen per cent of BDC deal count, with significant concentration in large unitranche financings originated in the low-rate era. Many backed application-layer SaaS companies — CRM tools, project management platforms, HR software — financed at five to seven times EBITDA with covenant-lite structures.

AI is compressing the value of certain software categories by automating the very workflows those products monetise. The result is not immediate default, but gradual erosion — weaker retention, pricing pressure, and reduced debt capacity. UBS has estimated that in an aggressive disruption scenario, default rates in US private credit could climb to thirteen per cent, far exceeding the four per cent projected for high-yield bonds.

The Qualtrics situation illustrates this shift — a $5.3 billion debt package was pulled after investors raised concerns about AI exposure, and the company’s existing loan has fallen to around 86 cents on the dollar. That said, the stress is concentrated. Mission-critical platforms with deep workflow integration and high switching costs remain resilient.

“Systems built around proprietary data, complex workflows, and industry-specific knowledge cannot easily be replaced by a general-purpose AI tool. These platforms are not being displaced by AI; they are being enhanced by it.”

FF: The headlines are very US-focused. How is the European market different, and does European growth debt face the same risks?

JD

The European market is a fundamentally different animal. The US private credit market has grown to approximately $1.5 to $2 trillion, driven heavily by large-cap leveraged buyouts of software and technology companies where the concentration risk sits.

European private credit is roughly a third of the size at around €530 billion, and it is growing from a lower base with more discipline.

European growth debt operates in a segment that is structurally better insulated. We are talking about growth-stage technology companies with ticket sizes of €3 to €25 million — far removed from the $500 million to $2 billion highly leveraged US unitranche loans under stress. These are smaller, capital-efficient businesses that have not been loaded with the aggressive leverage structures common in US sponsor-backed transactions.

The European growth debt market has also matured significantly. Dedicated providers like Atempo Growth, alongside the European Investment Bank and national development banks, have built a more mature, structured and disciplined ecosystem. The EIB Group has committed €70 billion under its TechEU programme to support innovation. These companies are largely domestically focused services businesses, insulated from cross-border tariffs on physical goods.

FF: How is ai disruption risk different across the stack?

JD

AI disruption is largely concentrated in large-cap, US-centric, application-layer SaaS. By contrast, vertical domain-specific software — systems embedded in healthcare, logistics, transport, regulatory compliance, and ERP — are built around proprietary data and cannot easily be replaced by a general-purpose AI tool. Infrastructure and middleware — data pipelines, cybersecurity, integration platforms, DevOps tooling — are enablers of the AI ecosystem and are seeing increased demand as AI adoption accelerates.

FF: Let’s talk specifically about Atempo Growth’s positioning. How is the portfolio exposed to — or protected from — these risks?

JD

Our portfolio is intentionally positioned in the most resilient layers of the software stack. We lend to the European mid-market ecosystem and have supported more than 32 portfolio companies with flexible growth financing since 2022. Our typical ticket size of €3 to €25 million into smaller, often founder-led businesses with conservative capital structures is a contrast to the highly leveraged, take-private transactions driving volatility in the US credit markets.

The companies we finance are focused in software segments genuinely harder to disrupt by AI. Across our portfolio — which spans logistics, fintech, compliance, and beyond — we consistently see businesses whose value is embedded in proprietary workflows, regulated processes, or infrastructure that AI depends on rather than replaces.

Our borrowers are not over-levered. Our underwriting emphasises sustainable growth over financial engineering. Borrowers typically carry lower leverage multiples, meaningful financial covenants, and clear paths to profitability — a stark contrast to the covenant-lite, PIK-heavy structures now causing problems in larger direct lending.

Finally, we work collaboratively with the venture capital ecosystem ensuring active portfolio oversight, including board observation roles. We lend to companies backed by professional investors with committed follow-on capital, which creates equity cushions, sponsor support in stress scenarios, and management teams accountable to sophisticated governance. structures.

“We consistently see businesses whose value is embedded in proprietary workflows, regulated processes, or infrastructure that AI depends on rather than replaces.”

FF: Beyond AI, the macro backdrop is volatile — trade tensions, tariffs, geopolitical uncertainty. How does this affect European growth debt?

JD

While macro volatility has increased — driven by trade tensions, tariffs and geopolitical uncertainty — the direct impact on European growth debt is limited and manageable.

US tariff policy has pushed the effective tariff rate to levels not seen since the 1940s, and the legal uncertainty around IEEPA versus Section 122 tariffs has added another layer of volatility. However, most estimates put the GDP impact of US tariffs on Europe at 0.1 to 0.2 per cent.

As ICG noted in their 2026 macro-outlook, private markets investors tend to have very limited exposure to the manufacturing and industrial sectors most affected by tariffs. The bulk of investments sit in less cyclical services businesses that are well-insulated from the direct effects of the trade war.

European growth debt markets are concentrated in services businesses with limited direct trade exposure. If anything, the current environment sharpens the relative appeal of European growth debt — a market that is growing from a disciplined base, supported by institutional infrastructure, and oriented toward the domestic European economy.

FF: Can you give us an update on Atempo’s platform and Fund II? And what is the key message for investors navigating this environment?

JD

We are in a strong position. Our first fund closed at €272 million in 2022, backed by the European Investment Bank, the British Business Bank, Santander and DECALIA, and was fully invested within three years. That is a testament to the depth of the opportunity in European growth lending.

In April 2025, we announced the first close of Atempo Growth II at €300 million, bringing total platform AUM above €800 million. Our target is €500 million by final close. The investor base includes Santander, the European Investment Fund, British Business Investments, CDP Venture, DECALIA, together with a leading European insurance group, reflecting the institutional credibility of the strategy.

Our team has now provided capital to over 32 companies across Europe, and the founding team has collectively financed more than 100 technology businesses over the past twenty years. A number of Fund I investments have now been repaid in full, including through refinancing transactions that triggered make-whole provisions, and with earlier investments approaching contractual maturity – underscoring the disciplined underwriting and portfolio management approach applied from inception through to realization. We take a hands-on approach — sitting on boards, working closely with management teams, and leveraging our network to help companies accelerate growth.

Key message for investors

Private credit is at an inflection point. AI disruption is real but its impact varies significantly — the companies most at risk are large-cap, US-centric application-layer SaaS businesses carrying heavy debt loads. European mid-market growth debt, and Atempo Growth specifically, is structurally positioned in a different part of the risk spectrum: smaller companies with lower leverage, meaningful covenants, resilient software layers, and alignment with the VC ecosystem — precisely the type of differentiated credit investing this environment demands.

“European mid-market growth debt is structurally positioned in a different part of the risk spectrum. In a market where selectivity and discipline are being rewarded, that is precisely the type of differentiated credit investing this environment demands.”

Image: Der Wanderer über dem Nebelmeer, Caspar David Friedrich, 1818

Sources P2: Atempo Growth; JPMorgan March 2026 loan valuation update; Bloomberg BDC index data; UBS private credit research Q1 2026; PitchBook leveraged finance report Q1 2026.

Sources P3: UBS private credit AI disruption scenario analysis Q1 2026; Bloomberg/PitchBook CLO sector performance data; Qualtrics debt market reports (Reuters, Bloomberg); Atempo Growth proprietary analysis. EIB Group TechEU programme disclosure; Bloomberg European private credit market data; ICG 2026 macro outlook; PitchBook European venture debt market report 2025.

Sources P4 for this supplementary analysis include: Financial Times (December 22, 2025), Fortune (March 14, 2026), CNBC (March 5, 2026), Bloomberg (various, November–December 2025), Morningstar (March 2026), Howard Marks / Oaktree Capital – “Cockroaches in the Coal Mine” memo and “Gimme Credit” memo (October–November 2025), JPMorgan Chase Annual Shareholder Letter 2025 (published April 2026), InvestmentNews (April 2026), HedgeCo Insights (February 2026), WebProNews (February 2026), Within Intelligence Private Credit Outlook 2026, Reuters (December 2025), Yahoo Finance / Apollo (December 2025), Puck (November 2025). Image: Der Wanderer über dem Nebelmeer, Caspar David Friedrich, 1818

Sources P5: Atempo Growth portfolio data (32+ companies financed since 2022); Atempo Growth Fund I and Fund II investor materials; company-level analysis by Atempo Growth investment team. ICG 2026 macro outlook; IMF/OECD GDP tariff impact estimates on Europe; Atlantic Council analysis on IEEPA tariff legality; Atempo Growth portfolio composition data.

Copyright © 2026 by DECALIA SA. All rights reserved. This report may not be displayed, reproduced, distributed, transmitted, or used to create derivative works in any form, in whole or in portion, by any means, without written permission from DECALIA SA.

This material is intended for informational and marketing purposes only and should not be construed as an offer or solicitation for the purchase or sale of any financial instrument, or as a contractual document. The information provided herein is not intended to constitute legal, tax, or accounting advice and may not be suitable for all investors. The market valuations, terms, and calculations contained herein are estimates only and are subject to change without notice. The information provided is believed to be reliable; however DECALIA SA does not guarantee its completeness or accuracy. Past performance is not an indicator of future results.

Some of the information presented in this paper is based on the direct experience of DECALIA as manager of collective investment schemes such as DECALIA Private Credit Strategies. Any intended or implicit reference to DECALIA Private Credit Strategies is not meant to represent a solicitation for the purchase or sale of the strategy or other strategies of DECALIA. Private markets strategies are not destined to the large public and its suitability must be evaluated in relationship to the risk profile, objectives and financial situation of any investor and the rules and limitations of each jurisdiction.