- Meeting massive power demand from data center projects across the globe will be a challenge

- Other bottlenecks are also becoming evident, on the regulatory, technical, labour & political fronts

- Ultimately, this might result in a slower-than-anticipated buildout cycle – but also less risk of overcapacity

In April, Maine nearly became the first US state to freeze the construction of AI data centers. In the end, the Governor vetoed the bill, on grounds that it did not exempt a project currently underway in a distressed town. In her decision communicated to the state Legislature, she did, however, signal some support for such a moratorium, owing to “the impacts of massive data centers in other states on the environment and on electricity rates”.

Procuring sufficient power, managing regulatory hurdles, securing technical staff and addressing local community concerns: these are but some of the headwinds facing the AI physical infrastructure buildout cycle. To the point of pushing it out in time… or into space?

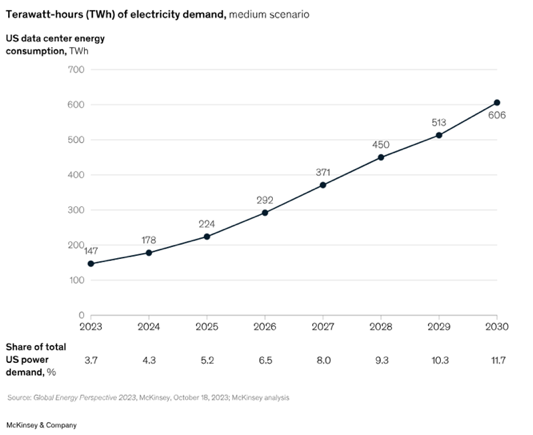

Across the globe, data center power demand looks set to expand massively over the next few years. A Morgan Stanley study projects 23% compound annual growth between 2023 and 2030 in the US and Asia, and a slightly lesser 16% pace in Europe. While such demand does not pertain only to AI data centers, they do represent a large chunk of the expansion, particularly in the US and Asia.

Some of the facilities projected by hyperscalers could require more than 1 gigawatt of electricity to run – roughly the consumption equivalent of 750’000 homes. Which of course begs the question of power availability going forward, and its cost, with the ongoing war in Iran only adding to the uncertainty. Dire predictions of a shortage of energy to power data centers have certainly been making the headlines recently.

Rather than attempting to secure greater supply from utilities or push to reinstate nuclear capacities – both potentially lengthy procedures – we note that a number of companies are trying to address the current energy availability issue by using gas turbines (Siemens Energy, GE Vernova) or fuel cells (Bloom Energy for instance).

In the US, the adoption of such technologies is of course helped by the country’s oil & gas self-sustainability. China, meanwhile, has a different advantage: that of having become a clean energy behemoth.

Bottlenecks, however, extend beyond just power. Tech industry executives are reporting that the buildout of major data centers is being delayed by permitting difficulties, as well as by a chronic undersupply of specialist workers and equipment.

The fact that projects are concentrated in some regions only compounds these problems and costs, by intensifying competition. And then there are the political hurdles associated with mounting complaints by local residents about noise pollution, potential water shortages and higher energy prices.

All in all, this could lead to the AI physical infrastructure buildout cycle lasting much longer than many currently anticipate.

This might cause disappointment in terms of monetisation of AI investments – which has certainly been the subject of much investor attention over the past months. Or it might be viewed in a somewhat positive light, because it serves to decrease the risk of a significant capacity overbuild.

Finally, it could provide impetus to the deployment of data centers in space, a topical subject given the upcoming SpaceX IPO !

Quirien Lemey, Lead Fund Manager

Demand for power for data centers is expected to rise significantly in the United States

Relief Rally vs. Reality Check

- Apocalypse Not Now! Not out of the woods yet, but the panic regarding Iran is over

- Still decent growth, more inflation in the near term and some hurdles for central banks

- Some caution warranted as the macro backdrop has become more challenging

We are not yet out of the woods as far as the conflict in Iran and subsequent blockade of the Hormuz Strait are concerned. However, the relief rally observed since the fragile and sloppy ceasefire makes some sense, negative fat tail probabilities having shrunk. It marked an inflexion point, paving the way for markets to refocus on fundamentals rather than being driven almost exclusively by oil price volatility. Equity indices, especially in the US, were able to recover rapidly and post new all-time highs, helped by surprisingly resilient economic activity data so far, still booming AI capex and a strong start to the earnings season. Cyclical sectors such as industrials and materials, technology and financials led the fast and furious rebound. Bonds and gold recovered about half their March losses, while the dramatic repricing of global monetary policy also eased. Consistent with the overall risk-on tone, credit outperformed sovereign bonds in April.

With the worse seemingly behind us, energy prices consolidating at ca. USD 100 per barrel and the Strait of Hormuz likely to reopen in the next few weeks, the probability of our central macro scenario has been revised up at the expense of the negative fat tail. Going forward, our base case involves a gradual de-escalation of the conflict, with incremental but bumpy progress and no clear resolution (there are too many negotiation pieces and players: uranium, Hormuz, Lebanon, etc.). Just enough for Donald Trump to get an upper hand at some point and declare victory. As a result, energy production and flows in the Persian Gulf should be restored before the summer, with oil prices heading towards USD 80 per barrel by year-end.

In this context, risks of a marked economic slowdown will persist in the Middle East, but they remain moderate overall and thus manageable elsewhere, with some transitory inflationary pressures. We continue to believe that the higher energy prices will not feed through to core inflation, as risks of second-round effects (a wage-price spiral) appear lower than at the outbreak of the war in Ukraine (the labour market is not as tight, and AI is generating productivity gains). Moreover, the global economy is less dependent on oil than it was in the 1970s, with the United States now a net exporter, whereas China has built up significant reserves on top of diversifying into green energy (and coal). The rest of Asia and, above all, Europe are the most strategically dependent/at risk.

The immediate task facing central banks has, however, become more complicated – even though the fragile ceasefire and subsequent pullback in oil prices have removed the urgency for most central banks, especially in Europe, to hike rates. Delivering the right dose, at the right moment, of the right monetary medicine is ever more challenging, especially as interest rates are not really the appropriate tool to deal with a supply shock.

At this point in time, our expectations regarding monetary policies are the following: Fed easing may be postponed until the very end of 2026, the ECB could eventually lift rates once or twice (although a status quo is still possible), the BoE is more likely to tighten than ease this year, and the SNB will remain on hold with a possible hike now in the cards.

Finally, it is worth noting that the Hormuz blockade will not be resolved soon in the sense that, even assuming a rapid and strong peace deal, without further energy infrastructure damage, several months will be needed to restore normal energy flows in the region.

Within portfolios, we thus decided to leave our slight underweight in equity unchanged following the strong April rebound. While the market’s willingness to “look through” adverse scenarios and geopolitical risks is not pure complacency (the AI theme, macro resilience, policy discipline – especially in EM – and demand for diversification continue to underpin risk assets), the recent impressive S&P 500 rally has been also driven, to some extent, by technical factors (short covering) and a big sentiment swing (from extreme fear to greed). It is not our intention to chase a short-lived, and likely somewhat exaggerated, positioning trade.

To conclude, caution continues to be warranted in a more challenging macro backdrop, with headwinds on growth, tailwinds for inflation and more intricate monetary policies. Admittedly, corporate earnings trends remain solid, Iran-linked geopolitical fears have likely peaked, and investor positioning is somewhat cleaner despite the market’s recent V-shaped pattern.

Still, valuation multiples leave only limited upside. In particular, “higher for longer rates” represent a significant risk for overall asset valuations, as well as the growth outlook as they raise the price of money. Lastly, the Hormuz blockade still requires resolution, while further strikes on energy infrastructure would also pose longer-term risks. In this context, we maintain a well-diversified all-weather approach to portfolio construction, across assets, sectors, regions and factors/styles.

Fabrizio Quirighetti, CIO & Head of Multi-Asset

No signs (yet?) of a significant slowdown on the horizon

External sources include: LSEG Datastream, Bloomberg, FactSet, Wisdomtree, International Energy Agency, McKinsey & Company.