Champion the european specialised private credit market

Nicolò Miscioscia, Partner and Head of Private Markets, Co-Manager DECALIA Private Credit Strategies

- Competition in direct lending gets messy

- Diminishing returns, deteriorated security packages, extended duration

- The absolute and relative value of specialised credit

- Barriers to entry allow strong risk/return profiles

- The complexity of the European market further reduces competition enhancing the risk/return opportunity, but investing is complicated

For this DECALIA Private Markets Focus issue we have drawn inspiration from the winter Olympics currently unfolding in Italy.

Investors can learn from athletes chasing for gold medals : study the discipline, refine skills, develop a solid strategy and act tactically.

This paper wishes to provide tactical insights for sophisticated investors chasing yield with a compelling risk-adjusted return in today’s market.

THE DIRECT LENDING RACE GETS OVERCROWDED

The once-niche world of direct lending – the practice of non-bank lenders providing private credit to private equity sponsors – has officially entered a „crowded“ phase. Data from 2024 and 2025 indicates that the massive influx of capital into the asset class, combined with the aggressive return of the Broadly Syndicated Loan (BSL) market, has created a „race to the bottom“ in terms of pricing and protections.

The global private credit market reached approximately $3 trillion by early 2025, growing nearly tenfold since 2009. However, the rate of deployment is slower than fundraising: according to McKinsey’s 2026 Global Private Markets Report, the share of dry powder aged two years or older peaked 40% in 2025.

The “crowding” is not only in fundraising. Leverage to the sector has also expanded. The Federal Reserve documented that committed credit lines by the largest U.S. banks to private credit vehicles (private debt funds and Business Development Companies “BDCs”) rose roughly 145% over five years, reaching about $95bn as of 2024 Q4.

Diminishing returns

As a result, the „illiquidity premium“ – the extra yield investors expect for locking up capital – is under severe attack, particularly in the upper middle market.

As of 2025, many „core“ private credit deals are pricing at levels previously reserved for public markets, despite the private loans remaining illiquid: the diminishing spread versus high-yield bonds makes the risk-adjusted case for generic direct lending harder to justify for institutional allocators.

PitchBook described a repricing wave showing how spreads migrated down the stack: as of September 2024, nearly 30% of unitranche facilities held by BDCs were in the S+500–549 bucket (up from 11% at end-2023), and the share of sub-500 spreads rose to 12.5% (from <4%).

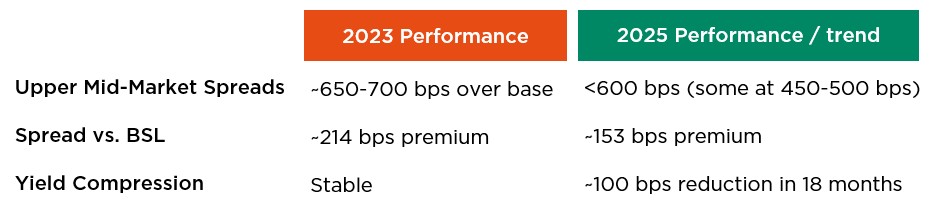

SPREADS UPPER MID-MARKET

Source: Pictet; Bloomberg; McKinsey; Travers Smith

What this means in practice: absolute all-in yields may still look high but the incremental premium (spread) earned for sponsor risk is getting competed away, especially in the most common structures (first-lien / unitranche, sponsor-led, broadly syndicated-like documentation).

Deteriorating security packages

As competition intensifies, „covenant-lite“ structures, once exclusive to the public BSL market, have become a standard concession in large-cap direct lending.

According to S&P Global Ratings, deals executed in 2024-2025 show significantly less covenant headroom. Lenders are increasingly forced to accept leverage-based pricing grids and PIK (Payment-in-Kind) toggles, allowing borrowers to defer cash interest.

A major sign of lender weakness is the rise of „portability provisions“ which allows a private equity sponsor to sell a company without the debt being repaid, keeping the lender’s capital locked in under a new, potentially unknown owner.

The „Flight to Quality“ Paradox: because lenders are desperate for „safe“ assets, they are willing to strip away protections to win mandates for top-tier companies. Pictet reports that deals are now closing in the 450–500 bps range often „without the benefit of any maintenance covenants.“

Duration extensions and defaults

Evidence from 2024 and 2025 confirms that generic direct lending is facing a „liquidity crunch“ characterized by extended exit timelines and mounting pressure on investor cash flows. PwC (using PitchBook data) notes that thousands of private equity exits have been delayed over the last two years, increasing pressure to return capital.

The primary reason for delayed exits is the mismatch between the expected 3–5 year hold period and the reality of a sluggish M&A market. Generic direct lending tends to be highly correlated to these macro cycles when loans are provided to private equity sponsors looking to return capital typically through a sale or an IPO.

Market participants describe “amend-and-extend” as increasingly common in private credit. Dechert, a major law firm, notes that in tougher conditions and with fewer new financings, borrowers are increasingly looking to “amend and extend” financing arrangements, i.e. pushing out maturities rather than refinancing or repaying on the original schedule.

Lincoln International (which values 5,500+ portfolio companies per quarter) reports that over the last 12 months it observed 730+ amendments (~16% of companies valued) and notes that many amendments are driven by liquidity needs and/or “being done to extend maturities and extend hold periods.”

“Continuation deals” in private credit are rising as a liquidity workaround because loans aren’t being repaid on time. The Financial Times reports record “continuation deals” (~$15bn in 2025 vs $4bn in 2024, per Jefferies) where managers create new vehicles to buy loans from older funds.

S&P Global (2026) notes that „selective defaults“—such as maturity extensions without adequate compensation—now account for the majority of defaults in the sponsored middle market.

SPECIALISED CREDIT IS ATTRACTIVE BUT FOR SKILLED PARTICIPANTS ONLY

As the „generic“ direct lending market becomes increasingly commoditized and crowded, Specialized Credit has emerged as a high-alpha alternative. This strategy shifts the focus from simple capital preservation to return maximization by exploiting market dislocations and complex corporate needs.

While generic direct lending typically involves providing senior secured „unitranche“ loans to stable, PE-backed companies, Specialized Credit is more flexible.

Strategies typically include:

§Sponsorless Lending: Lending directly to founder-owned or family businesses that lack a Private Equity sponsor, requiring more intensive due diligence and structuring.

§Capital Solutions: Tailored capital (senior, subordinated or preferred equity) for M&A, refinancings, or „spin-offs“ where traditional bank capital is insufficient.

§Asset-Backed Finance (ABF): Lending against specific, complex assets (e.g., IP, equipment, or receivables) rather than just corporate cash flow.

§Special Situations: Providing „rescue“ or bridge financing to companies facing temporary liquidity crunches or broken balance sheets.

§Distressed Debt / Stressed Credit: Purchasing deeply discounted debt of troubled companies to benefit from a „pull-to-par“ or through a restructuring process.

Less competition…

Specialised Credit is technically applicable to any company, the addressable market is large but the current market size is way smaller than direct lending, evidencing an imbalance between demand and offer or capital.

Preqin reports that direct lending secured 77.4% ($152.7bn) of total private debt capital raised in 2024, while all Specialised Credit strategies attracted in aggregate $24.8bn.

This fundraising split is a simple but powerful indicator: far more capital is trying to do plain-vanilla direct lending than opportunistic/special-situations style credit.

The Specialised Credit market has a lower number of participants, mainly due to:

Barriers to Entry: Generic lending is a „volume game“ where the largest managers (Ares, Blackstone, Blue Owl) compete on price and speed. Specialised Credit require deep legal expertise and specialized restructuring teams, which many new private credit entrants lack.

Sourcing Difficulty: Unlike sponsor-backed deals which are brought to lenders by private equity firms, opportunistic deals are often proprietary. Carlyle notes that „sponsorless“ and „tailored capital solutions“ require a level of origination capability that only a limited number of established platforms possess.

…drives higher returns…

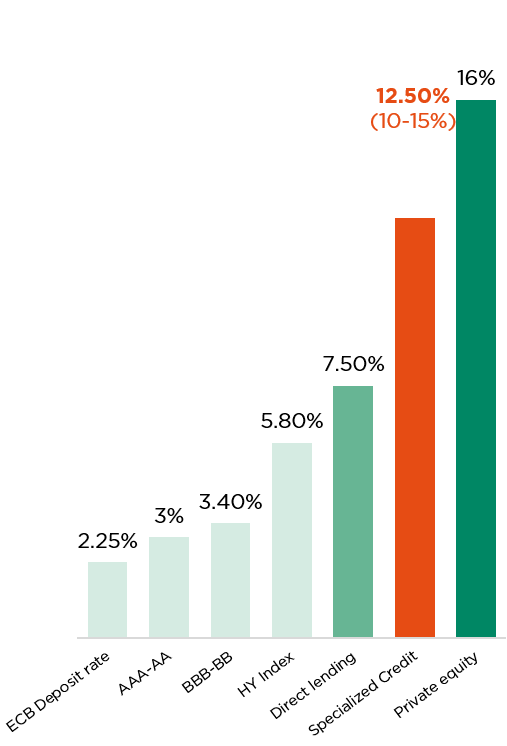

According to CAIA and Morgan Stanley (2026 Outlook), while senior direct lending yields have settled in the 8% vicinity (in USD), return-maximizing opportunistic strategies typically target mid-to-high teens IRRs. This „alpha“ is generated not just from higher interest rates, but from original issue discounts (OIDs), equity kickers (warrants), and restructuring gains.

…with no additional risk or duration issues

While „Credit Opportunities“ (Special Situations, Capital Solutions, etc.) are often perceived as higher-risk due to their complex nature, data from the 2024–2026 market cycle suggests that their risk profile, when measured by default stability, volatility, and correlation, is often superior to or more resilient than generic direct lending.

The risk in credit opportunities is often „priced in“ at entry, whereas the risk in generic direct lending is frequently „hidden“ by loosening terms.

Risk indicators (ND/EBITDA)2

According to UBS Global, private debt, and specifically opportunistic sleeves, exhibits lower volatility than conventional public debt with similar ratings. This is due to the „mark-to-model“ nature of the assets and the bespoke, bilateral negotiations that prevent the „forced selling“ spirals common in broadly syndicated loans (BSL).

Data from the European Investment Bank (EIB) 2024 Report shows that private credit contracts average a recovery rate of 72.2%. Specialised Credit managers, who specialize in restructuring and legal enforcement, often achieve higher ultimate recoveries than „tourist“ managers in the generic space who lack the infrastructure to manage a work-out.

A critical advantage of credit opportunities is its low correlation to both the public equity markets and the private equity deal cycle.

Generic direct lending is 80–90% correlated to the PE sponsor cycle. When M&A activity stalls—as it did in 2024/2025—generic lenders face a „deployment drought“ and cash flow pressure.

Specialised Credit can also build protection from more varied forms of guarantees: strategies like Asset-Based Finance (ABF) and Special Situations depend on contractual cash flows from specific collateral (IP, equipment, receivables) rather than the general corporate enterprise value. This results in a significantly lower correlation to the broader equity market, providing a true diversifier in a portfolio.

Counter-intuitively, credit opportunities strategies often respect original maturities more reliably than generic sponsored credit.

- Independent Exits: Credit opportunities often provide transitional capital. Because these lenders are not beholden to a PE sponsor’s exit timeline, they structure deals with hard triggers and „self-liquidating“ mechanisms (e.g., cash flow sweeps).

- Exits in credit opportunities is typically a refinancing event or a specific asset sale, which is less dependent on the „high equity multiples“ required for a PE sponsor to pay back a generic unitranche loan.

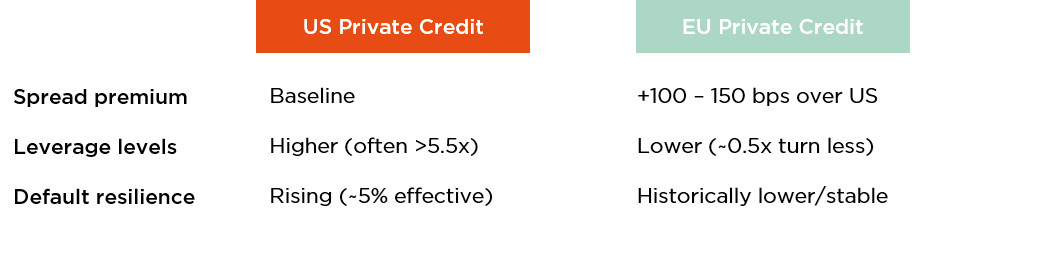

EUROPE OFFERS THE STRONGEST OPPORTUNITY

While the U.S. market is deeper and more mature, its homogeneity has led to extreme competition. In contrast, Europe’s „patchwork quilt“ of legal, cultural, and linguistic barriers creates a complexity premium that rewards managers with deep local expertise.

Europe remains a collection of distinct markets. This heterogeneity significantly reduces the number of managers capable of operating effectively across the continent.

- Multilingual & Cultural Barriers: Sourcing „off-market“ credit opportunities in the European lower-mid market requires local boots on the ground.

- Legal Fragmentation: bankruptcy regimes vary wildly: while the UK’s „Administration“ is well-understood, legal precedents in Germany or France often privilege different stakeholders, requiring bespoke legal structures for every deal.

- Regulatory Hurdles: The ECB and European Investment Bank (2023-2025) continue to report that „fundamental legal barriers“ in post-trade services and national tax laws remain unaddressed. This prevents the „mass-market“ scaling of credit funds, leaving the field open to Specialised Credit players.

Source: Morgan Stanley, CFA Institute, Scope ratings

Obstacles to succeed in the yield race

While the fragmentation of the European market creates the „complexity moat“ that protects high yields, it also presents a significant paradox for investors: the same barriers that generate alpha make it incredibly difficult to achieve a structured, diversified allocation. In contrast to the U.S. market, where an investor can gain broad exposure to the asset class through a few „mega-funds“, the European Specialised Credit segment requires a much more granular and labour-intensive approach.

- Hyper-Specialization: Managers tend to be „local heroes.“ A firm might have a 20-year track record in Nordic distressed debt but zero presence in Spanish restructuring. For an investor, this means that a single fund commitment rarely provides true „European“ diversification; it usually provides a concentrated bet on a specific sub-region or legal system.

- Due Diligence Fatigue: According to Allianz Global Investors (2026 Outlook), outperformance in this space depends on „rigorous analysis and disciplined underwriting.“ For an institutional allocator, performing due diligence on 10 different specialist managers across 10 jurisdictions is exponentially more expensive and time-consuming than vetting two or three large-scale U.S. managers.

- Small Deal Sizes: Many of the best European opportunities are in the lower-middle market (companies with €10m–€50m EBITDA). Large pension funds or sovereign wealth funds find it nearly impossible to do so in this segment without significantly increasing their „manager count,“ which leads to higher administrative overhead.

- Adherence to Maturities vs. Diversification: As discussed, while these managers respect maturities better because they aren’t tied to the PE equity cycle, this very „independence“ means their cash flows are lumpy and unpredictable. This makes it harder for an investor to build a „laddered“ portfolio of maturities compared to the more standardized BSL or generic direct lending markets.

Conclusion

Europe’s Specialised Credit market offers a durable complexity premium, supported by fragmentation across legal systems, languages and restructuring regimes. Yet that same fragmentation increases execution dispersion and makes structured, diversified access more challenging than in more unified markets such as the United States. As a result, while the opportunity set is attractive, capturing it requires institutional-grade platforms capable of coordinating multi-jurisdiction sourcing, underwriting, and risk management across Europe.

1 Source: Listed indexes ICE BofA, iShares, Invesco. For direct lending the target net IRR of 7.5% comes from Preqin, whilst the average net money multiple used is 1.4x which is on the higher end of the TVPI for European direct lending reported by Pitchbook between 2012 and 2022. For private equity we assumed a 16% net return, in line with Pitchbook 2010-2020 data for European Buyout and Growth private equity funds and a 2x TVPI in line with the higher end the results for the same group. Specialized Credit return is in line with DECALIA Private Credit Strategies current track record at >12.5% net IRR in aggregate between fund I and II as at September 30th 2025.

2The estimates of avg ND/EBITDA for the various asset classes come from Pitchbook, S&P, ICG, McKinsey, Baird. The avg ND/EBITDA of DPCS is calculated as the weighted average of Q4 24 leverage KPIs of DPCS I and II

Copyright © 2026 by DECALIA SA. All rights reserved. This report may not be displayed, reproduced, distributed, transmitted, or used to create derivative works in any form, in whole or in portion, by any means, without written permission from DECALIA SA.

This material is intended for informational and marketing purposes only and should not be construed as an offer or solicitation for the purchase or sale of any financial instrument, or as a contractual document. The information provided herein is not intended to constitute legal, tax, or accounting advice and may not be suitable for all investors. The market valuations, terms, and calculations contained herein are estimates only and are subject to change without notice. The information provided is believed to be reliable; however DECALIA SA does not guarantee its completeness or accuracy. Past performance is not an indicator of future results.

Some of the information presented in this paper is based on the direct experience of DECALIA as manager of collective investment schemes such as DECALIA Private Credit Strategies. Any intended or implicit reference to DECALIA Private Credit Strategies is not meant to represent a solicitation for the purchase or sale of the strategy or other strategies of DECALIA. Private markets strategies are not destined to the large public and its suitability must be evaluated in relationship to the risk profile, objectives and financial situation of any investor and the rules and limitations of each jurisdiction.