The US Supreme Court ruled last Friday that the President cannot use “emergency” authority to impose tariffs at will (i.e. the use of the International Emergency Economic Powers Act (IEEPA) to impose broad based tariffs is unconstitutional). While that’s a great victory for the “rule of law” and thus somewhat reassuring politically speaking, it brings again another round of uncertainties as Trump administration will likely be able to reimpose many tariffs on other legal grounds, at least for some time.

When, at which rates, to which countries, to which goods and services, for how much time? The only certainty it that the overall tariffs rate will likely be lower than the one prevailing until now. It was close to 13% a few months ago but it has already declined to 11% more recently due to some exclusions –in order to soften inflationary pressures– as well as some imports rebalancing from companies. Will the prior tariffs have to be repaid? This could raise interesting questions about fiscal policies (no additional stimulus checks before mid-terms and/or renewed concerns about US debt trajectory), inflation and companies’ margins (will consumer-related companies reduce their selling prices in accordance or keep the refund for themselves to increase their margins?), as well as politically as some Republicans could be reluctant to re-install other “legal” forms of tariffs, which are clearly unpopular among US citizens, before the mid-term elections.

In the meantime, the really good news for investors comes, once again, from both the earnings season and the latest round of US economic data, which proved both reassuring. Here is a quick and even if certainly not exhaustive overview, through tables and graphs, of the latest releases.

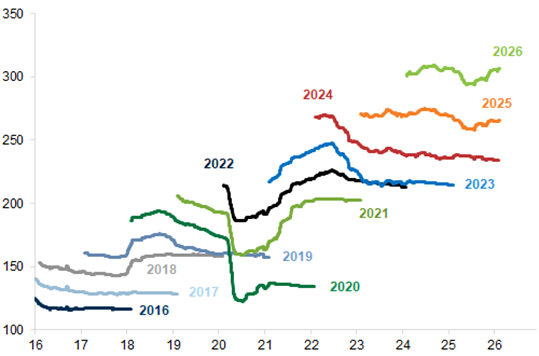

Starting with the earnings season, it has been strong across the board with positive revisions for 2026 (essentially coming from tech and cyclical sectors) at a time when usually companies prefer to set the bar lower…

MSCI AC World EPS estimates in USD

Source: Goldman Sachs

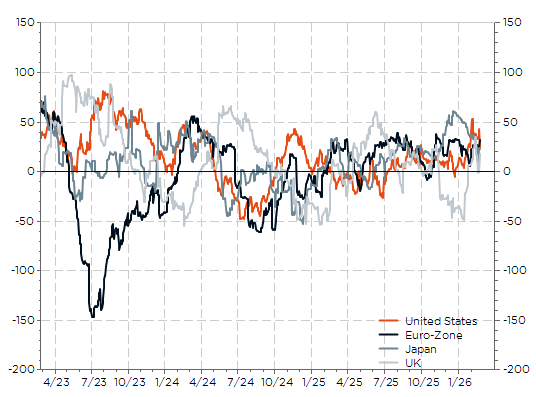

Then, economic surprises have remained positive in most DM economies.

Citi economic surprises in developed economies

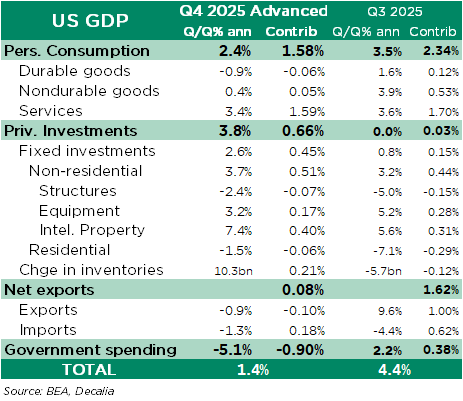

Although US headline Q4-2025 GDP first estimate came below expectations (+1.4% a.r. vs. +2.8%), domestic demand still shows resilience with positive contribution from both consumer spending (up +2.4%) and private investments (+3.8%). In fact, the main culprit of last quarter weakness was government spending, which shaved as much as -0.9% to overall growth, due to the more than 6 weeks long shutdown…

US Q4-2025 GDP (1st estimate) breakdown

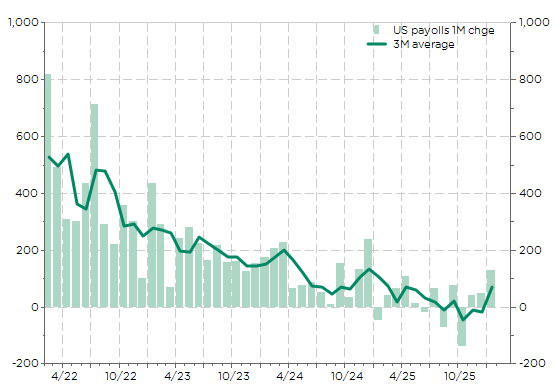

US labor data tended to confirm that the Fed sis in no hurry to ease further as payrolls surprised on the upside (+130k in January), while the US unemployment rate declined to 4.3% last month

US 1M payrolls change and 3M average: not so terrible after all

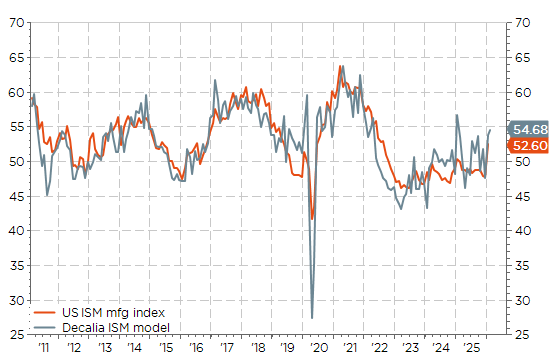

Finally, our ISM model, based on the Philadelphia Fed and Empire manufacturing indices, shows that the US ISM manufacturing index should remain above 50 this month, signaling therefore an ongoing expansion in US industrial activity.

US ISM model

In conclusion, the economy remains on solid footing. Strong growth, healthy employment, and resilient consumer demand, as well as ongoing disinflation and potentially lower rates to keep the economic engine on, provide the underlying support that allows markets to absorb elevated valuations and geopolitical uncertainty without lasting damage. It is typically when economic momentum slows or contracts that excesses are exposed and risks are repriced. In other words, overvaluation and geopolitical tensions matter most when the economic engine weakens; when activity is robust, markets can generally sustain and digest these pressures with limited lasting impact.

Economic Calendar

March madness is coming but, in the meantime, we should have a quiet and light last week of February as far as economic data releases are concerned. In the US, Nvidia earnings releases on Wednesday, the State of the Union address to be delivered by President Trump on Tuesday, as well as ripple effects from the Supreme Court decision invalidating Trump’s “Liberation Day” tariffs, will likely steal the show from the macro. The main US data highlights will just include the Conference Board’s consumer confidence for February on Tuesday and the January PPI on Friday.

Turning to Europe, the focus will be on economic sentiment indicators for various large economies over the week (starting this morning with the German IFO, which was slightly ahead of expectations), and more specifically for the whole Euro Area on Thursday. On Friday, we will also get the preliminary February CPI prints for Germany and France and the Swiss Q4 GDP. Finally, still on Friday, Japanese activity data for January will take center stage in Asia with the releases of industrial production, retail sales and housing starts.

Wrapping up with the earnings season, the big event will be the Nvidia’s results on Wednesday’s evening (after the close). We will also get also the Salesforce figures at the same time, as well as the results of several US retailers over the week (Home Depot, TJX, Lowe’s) and from the 2 largest Canadian banks (RBC & TD) on Thursday. In Europe, the main earning releases include HSBC and Allianz in financials, Deutsche Telekom, Schneider Electric and Iberdrola.

Non-exhaustive list of major earnings releases over the week (market cap > $100bn)

Source: https://earningshub.com/earnings-calendar/week-of/2026-02-23

This is a marketing communication issued by DECALIA SA. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The information and data presented in this document are not to be considered as an offer or invitation to buy or sell any securities or financial instruments nor to subscribe to any services. The information, opinions, estimates, calculations etc. contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Investments in any securities or financial instruments may not be suitable for all recipients and may not be available in all countries. This document has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Before entering into any transaction, investors should consider the suitability of the transaction to individual circumstances and objectives. Any investment or trading or other decision should only be made by the client after a thorough reading of the relevant product term sheet, subscription agreement, information memorandum, prospectus or other offering document relating to the issue of the securities or other financial instruments. Where a document makes reference to a specific research report, the document should not be read in isolation without consulting the full research report, which may be provided upon request.