- Nowadays, high-calibre managers, rather than capital, are what define the top hedge funds

- Evolving compensation packages reflect this increasingly competitive race for talent

- Still, recruiting excellent fund managers is not enough: they also need to be put to work as a team

Within the hedge funds universe, financial capital is no longer necessarily the scarcest resource. Large multi-strategy platforms now have extensive balance sheets, powerful technological infrastructure and global access to financial markets. The real competitive advantage lies elsewhere: in the ability to attract, mentor and retain the best managers.

In some respects, this development is reminiscent of modern football. Running a very successful club is not just a matter of having a fine stadium or a large budget: it is about identifying the right players, integrating them into a coherent system and maintaining a balance between individual talent and collective discipline. Major alternative investment platforms follow a similar logic. They seek out the best specialists, but above all strive to ensure that each team contributes to overall performance, within a strict risk framework.

This race for talent has become so prominent that some fund managers are now represented by agents, much like professional sportspersons. According to The Wall Street Journal, Laurel Lake Advisors, a specialist agency founded by a former Citadel and Millennium fund manager, has reportedly negotiated some USD 180 million in compensation packages for 12 clients.

The figures mentioned in the financial press provide an indication of the scale of this competition. Bloomberg reported back in 2023 already that a senior portfolio manager had been recruited by a major New York fund with over USD 120 million in guaranteed payments, whilst several recruitment deals were said to have exceeded USD 50 million. These figures should be treated with caution, as they are not generally confirmed publicly by the respective funds. Nonetheless, they illustrate a reality: in strategies with strong alpha-generation potential, individual talent has become a strategic asset.

This development can be explained by the very model upon which multi-strategy alternative platforms operate. Capital is allocated across several specialised teams: arbitrage, long/short equities, credit, macro, quantitative analysis or relative value. Each team must demonstrate its ability to deliver risk-adjusted returns, all the while adhering to a strict framework.

As with a top football team, simply amassing talent is not sufficient: it is the quality of the system, the management and the discipline that makes the difference over the long run.

Compensation packages reflect this scarcity. According to a Financial Times article that quoted Goldman Sachs, traders at the highest-paying firms are said to have received an average 24.5% of the profits generated in 2025, up from 22% in 2022. At the same time, Goldman Sachs Asset Management reports that some 83% of multi-manager hedge funds now charge so-called “pass-through” fees, vs. 63% in 2022. Passing such costs on to end clients enables these platforms to invest heavily in their teams, data, technology and risk management.

For investors, these trends do not call into question the merits of hedge funds. Rather, they serve as a reminder that the sector has become more institutionalised, more competitive and more complex to analyse. Not all managers have the same access to talent, the same infrastructure or the same economic situation.

As such, selection is key. And a fund of hedge funds can play a useful role in this regard: identifying the most robust platforms, diversifying the sources of alpha, comparing access conditions and assessing whether the level of fees is justified by the quality of the organisation. As talent becomes scarcer, access to excellent managers becomes a source of value in itself.

François Botta, Senior Portfolio Manager

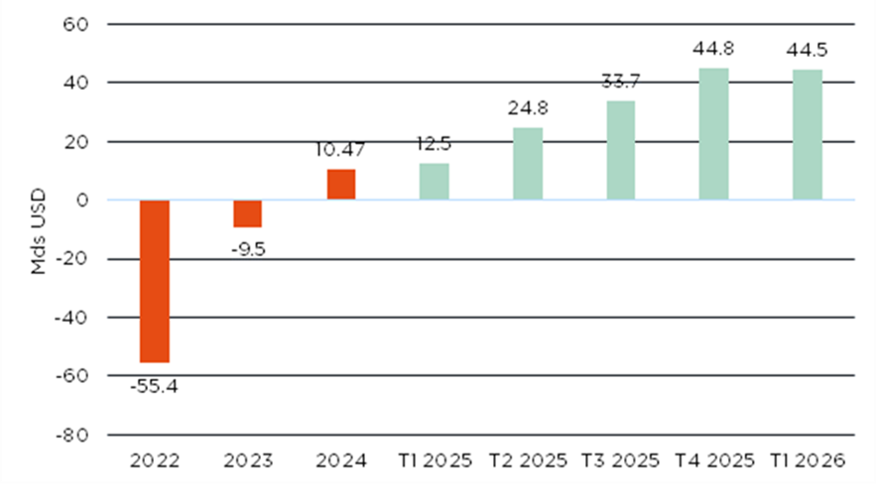

Positive trend in the normalisation of payments to hedge funds

Is Wall Street increasingly diverging from Main Street?

- Bending but not breaking: market and macro resilience, with AI in the driving seat

- Steady but increasingly uneven growth – within a more fragmented world

- Structurally higher inflation and volatile backdrop, but not necessarily bearish

Global markets have continued to grind higher despite a still fragile geopolitical backdrop, marked by a prolonged disruption of the Strait of Hormuz. Markets have increasingly been supported by ongoing hopes of a US-Iran peace deal, as well as resilient macro and corporate fundamentals – with a growing divergence between a still solid US economy and a much weaker Europe. The former continues to benefit from booming AI-related capex, resilient manufacturing activity, infrastructure spending and robust corporate earnings. Europe meanwhile is being weighed down by higher energy prices and weaker domestic momentum. Inflation pressures have re-emerged globally, largely driven by the energy shock, forcing markets to reassess the “rate cuts only” narrative and progressively reprice a higher-for-longer monetary regime, with some central banks even contemplating additional hikes.

Still, risk assets have remained resilient as investors increasingly view the current environment less as a recessionary shock and more as a regime of moderate growth, sticky inflation and continued fiscal support. Global equities have continued to post new highs, led primarily by US and Asian technology stocks, especially semiconductors and hardware beneficiaries of the AI capex boom, with energy names also outperforming. Despite an excellent US earnings season (broad positive surprises and upward revisions), market participation remains narrow and concentration has increased further, meaning that the new market highs are accompanied by deteriorating breadth. Sentiment and positioning have also become less supportive, moving from fear to greed and from oversold to increasingly overbought conditions.

Our central macro scenario remains one of resilient but increasingly heterogeneous global growth, within a more fragmented and uncertain world. The US should remain the main global economic engine thanks to AI-driven investment, fiscal support and resilient manufacturing activity, while Europe will likely remain constrained by higher energy costs and weaker cyclical momentum. Inflation dynamics have again become more challenging following the recent energy shock, leading to a pause in the global disinflation process and forcing markets to adjust to a higher-for-longer policy environment. Still, we believe inflation should remain broadly manageable over the medium term, particularly if growth moderates gradually and second-round price effects remain contained.

In this environment, monetary policy is likely to remain highly data-dependent, with some developed market central banks potentially contemplating additional tightening before any meaningful normalisation can resume. Our downside scenario remains centred around a stagflationary regime involving persistently high core inflation, tighter monetary conditions and rising risks of recession or financial instability, potentially amplified by further commodity price shocks, private credit dislocations or a sharper slowdown in China. Conversely, the upside scenario would require an improvement in geopolitics, lower energy prices, faster disinflation and stronger productivity gains from rapid AI adoption, ultimately supporting both growth and risk assets.

This leads us to maintain a cautious but not defensive tactical allocation stance, remaining slightly underweight equities while acknowledging that resilient growth, strong earnings momentum and the ongoing AI investment cycle continue to support risk assets.

We continue to favour high quality companies with strong pricing power, visible cash flows and structural growth exposure, while also maintaining selective exposure to cyclicals, value and small- & mid-caps, which could benefit from an improvement in market breadth. Regionally, we still prefer the US and Switzerland given their superior earnings visibility and quality bias, and remain more cautious on Europe, the UK and those emerging markets that are exposed to higher energy prices and tighter financial conditions.

In the fixed income space, we continue to favour high quality investment grade credit in the 3- to 5-year segment, as an attractive carry opportunity without excessive duration risk. Within alternatives, we still value uncorrelated strategies such as CTAs, market neutral and arbitrage approaches in an uncertain macro and policy environment. We also stick to our constructive medium-term views on gold, selected commodities and defensive currencies such as the CHF, while becoming incrementally less bearish on the USD given the resilience of the US economy and fading prospects of near-term Fed easing.

Overall, the macro regime continues to evolve toward a more complex equilibrium characterised by resilient but uneven growth, structurally higher inflation volatility, more constrained central banks and persistent geopolitical tensions. Although this backdrop argues against excessive risk-taking and calls for greater selectivity across asset classes, it does not yet point to an imminent recessionary or systemic market scenario. Markets are increasingly adapting to a world of higher nominal growth, stronger fiscal involvement and ongoing AI-driven investment dynamics, even as monetary policy becomes less supportive. As such, maintaining diversified exposure to high-quality assets, selective cyclicals, carry opportunities and opportunistic hedges remains, in our view, the most appropriate way to navigate the coming months.

Fabrizio Quirighetti, CIO & Head of Multi-Asset

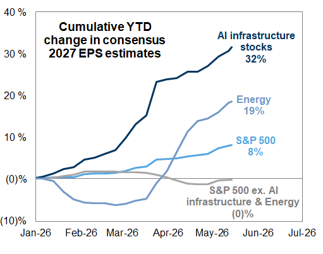

EPS growth largely driven by AI

External sources include: LSEG Datastream, Bloomberg, FactSet, Goldman Sachs, Hedge Fund Research.