- The deployment of humanoid robots has begun, with Chinese manufacturers in the lead

- Scale and continued hardware cost reduction will be key to reaching commercial viability

- Technical barriers also remain, particularly when it comes to (future) household applications

From being just a curiosity twelve months ago, humanoid robots went to taking centre stage at CES 2026. Indeed, this year’s edition of the Las Vegas “most powerful tech event” saw nearly two dozen humanoid robots on display. Robotics is entering a new phase of commercial acceleration, driven by AI breakthroughs, falling hardware costs and structural labour shortages – with Wall Street rapidly repositioning.

The shift from narrow-task robots to humanoids places far greater demands on AI: robots must now navigate unstructured spaces, interpret human behaviour and respond through physical action. Shipments are forecast to surge from ca. 20,000 units in 2025 to 10 million annually by 2035 with some projections putting the global robot population at 3 billion by 2060, outnumbering cars per capita! In turn, capital flows into the sector have grown from ca. USD 700 million in 2018 to ca. USD 4.3 billion in 2025, with over 50 companies globally now developing humanoid platforms and some 150 commercial models having been launched as of January 2026.

At this – still early – stage of commercialisation, China is the dominant force. The country accounted for over 80% of global deployments last year (Agibot and Unitree alone delivered over 70% of all commercial humanoids in 2025). Humanoids clearly constitute a strategic priority for the Chinese government, given the unfavourable demographics (ageing population and persistently low birth rate) that it is facing. Nevertheless, US companies are serious contenders, with Tesla reallocating, just this quarter, manufacturing capacity away from cars to its Optimus humanoid programme. Other players, notably Figure AI, Agility Robotics and 1X, are targeting the enterprise and early household markets.

From a business model standpoint, hardware costs remain a barrier. Western pilot-stage humanoids currently cost USD 90,000-100,000 per unit to develop, although standardisation and scale are fast compressing costs. The situation in China appears markedly different. Bank of America analysts estimate the bill of materials (BOM) for Chinese-built humanoids at USD 35,000 in 2025, falling to below USD 17,000 by 2030 and ca. USD 13,000 by 2035. The single biggest driver of costs are actuators, which account for more than half of the BOM at scale (a typical humanoid robot deploys ca. 30 actuators). Cost reduction in this space will thus be critical to commercial viability. Still, early return-on-investment evidence is proving encouraging: Boston Dynamics reports that customers typically recover costs within two years, even at the current price points.

Beyond the economics of the humanoid robot business, a number of technical barriers remain. Dexterity, battery life, fall safety and reliable operation in unstructured environments are all issues that have not yet been fully solved, meaning that household applications are still years away from early commercialisation.

From an investor standpoint, Nvidia is the clearest infrastructure play. Not only is the company well-positioned to be the sector’s backbone, but robotics also stands as an extension of existing AI chip demand, not a speculative new bet. Other high-conviction picks include component suppliers in actuators, sensors and precision motors, as the BOM trends down. Planetary roller screws, frameless torque motors, as well as coreless motors are projected to carry the highest per-robot content value. Broader, non-stock specific, exposure can be obtained via ETFs (e.g. KOID, BOTT, HUMN), although these carry significant legacy industrial robot and rare earth exposure, alongside pure-play humanoid names.

Christophe Reuter, Junior Portfolio Manager

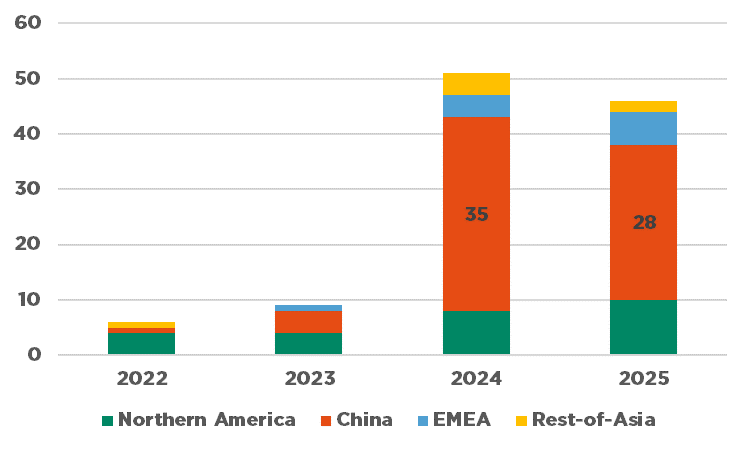

Humanoid unveils by region

Mind the AI disruption beneath the surface

- AI disruption: a “software-mageddon” beneath the surface with multiple ramifications

- One man’s misfortune is another man’s fortune

- Conditions still smell of Goldilocks but mind the tail risks – on both sides

The global macro focus has broadened from geopolitical volatility (even though tensions between the United States and Iran may intensify) to other themes, notably concerns over AI disruption. This has driven market dispersion beneath the surface, leading to a severe sell-off and derating of software companies, but improving therefore market breadth and overall market valuations, as well as sentiment and positioning indicators. In the meantime, the economic backdrop remains supportive with decent growth momentum, ongoing disinflation and a monetary policy easing stance. Earnings season has been reassuring too with broad-based earnings beat across regions and sectors and positive revisions for the whole year 2026 (coming essentially from tech and cyclical sectors) at a time when companies usually prefer to set the bar lower…

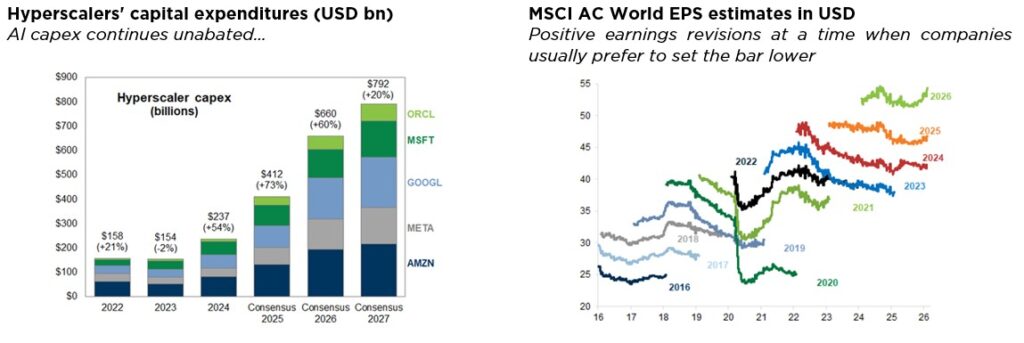

As a result, global equity indices, especially those outside the US and thus less exposed to AI disruption, have continued to benefit from this supportive macro backdrop. A weaker USD and somewhat lower US rates have helped them too, including US small caps. In this context, “Mag7” are lagging year-to-date, whereas EM markets, Japan, cyclical sectors and value style are outperforming. It’s also worth noting that the IT mega-cap companies have announced a further increase of their capex this year from $540bn initially expected to $660bn, which will now be more and more financed through new debt issues as this amount represents circa 90% of their free cash-flows. Paradoxically, we thus probably need to see less dramatic growth rate in AI capex to see these companies start performing strongly again. Elsewhere, bonds are also posting decent performances across the board with very contained rates and credit spread volatility, in line with our views that carry will matter more than rates or spread trends impact on prices this year. Here again, EM debt has continued to outperform as it was the case last year. Finally, gold and precious metals have been among the most volatile assets lately. This has contributed to a healthy cleaning of speculative positions in our views, while we still retain a constructive stance on gold.

Among the downside risks that are bound to arise unexpectedly along the way, a new one has erupted lately: a broad-based AI disruption resetting asset prices valuation, exacerbating deflation forces & leading to a new instable macro regime. While we assign a low probability to it and see only minor direct economic impacts in the foreseeable future (modest productivity gains and layoffs this year), it could still have some significant indirect impacts through financial markets dynamics in the short term. On the opposite, interest rate upward pressures (accelerating growth momentum, persistent inflation or concerns about the sustainability of certain fiscal trajectories) can’t be completely dismissed neither. A full-blown US-Iran conflicts may also become a game changer by plunging the global economy into stagflation.

As a result, we remain broadly neutral and in wait-and-see mode at the portfolio level, still constructively invested but cautiously diversified and balanced. This positioning reflects a prudent approach given the overall stretched valuations, high level of geopolitical uncertainty and wide range of potential tail-risk outcomes. It should help portfolios deliver better risk-adjusted returns by smoothing inevitable market bumps and sector rotations, while maintaining enough flexibility to adapt as conditions evolve. In this context, we have also implemented tactical hedges recently in portfolios with medium or higher risk profiles.

As diversification & selectivity remain a cornerstone of our current allocation, we are warming up on energy-related investments as they could benefit from higher oil prices in the next few months due to the escalating US-Iran tensions. Besides, we also remain selectively positive on other metals on the back of resilient economic growth, limited supply and growing demand related to AI boom as well as the ongoing structural energy transition.

Fabrizio Quirighetti, CIO & Head of Multi-Asset

External sources include: LSEG Datastream, Bloomberg, FactSet, Goldman Sachs, Morgan Stanley.