First real stress test for semi-liquid evergreen funds can trigger a long term confidence issue ?

Nicolò Miscioscia, Partner, Head of Private Markets and Digitalisation, Co-Manager DECALIA Private Credit Strategies

The evergreen semi-liquid model gets tested

- Redemption requests hit the industry

How do evergreen semi-liquid funds actually work

- Focus on operational service vs performance

- Complex tools to ensure the functioning of the semi-liquid mechanism

Redemptions & gates: financial, reputational, legal risk?

- May a confidence crisis trigger concrete risks?

- Similarities with the hedge fund industry after 2008

Private markets evergreen structures are sold as a bridge between illiquid assets and investors who want some liquidity.

We are now witnessing the first real wave of redemption pressure, which exposes the central fragility of the model: the underlying assets are fundamentally illiquid and slow-moving, while the client base is increasingly wealth, affluent and retail-adjacent, with expectations shaped by public-market habits.

This paper seeks to help investors form a knowledge to prevent surprises.

THE EVERGREEN SEMI-LIQUID MODEL GETS TESTED

In March 2026, we have observed an impressive wave of communications about redemptions hitting limits in semi-liquid funds, after investors’ requests surged.

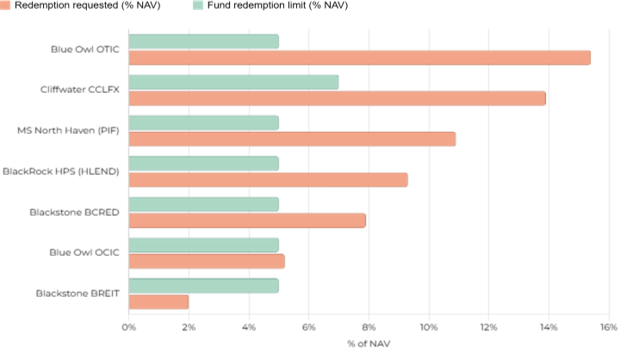

For example, according to the FT, Cliffwater’s ~$33 billion Corporate Lending Fund (CCLFX) received redemption requests equal to 14% of shares and limited redemptions to 7%, while Morgan Stanley’s $7.6 billion North Haven Private Income Fund capped withdrawals after requests reached 10.9%. BlackRock’s HPS Corporate Lending Fund (HLEND) limited withdrawals after investors sought to redeem about 9.3% of NAV, above its standard 5% quarterly liquidity limit. At Blackstone, the issue looked slightly different but still telling. BCRED did not fail to honour requests in the latest quarter; instead it had to increase its usual repurchase size. A March 2026 SEC amendment shows Blackstone Private Credit Fund (BCRED) increased the offer to buy back up to 7% of outstanding shares, above the normal 5% framework. Trade press and other coverage tied that change to a record 7.9% redemption request rate, equivalent to roughly $3.7 billion.

Redemption requests vs standard quarterly limits – Q1 2026 – % of NAV

Sources: SEC filings, Bloomberg, PitchBook, Morningstar, AltsWire — Q1 2026 tender offer results. Redemption limits are standard quarterly maximums per fund prospectus; some managers can raise limits via board approval. AUM figures approximate.

These are not isolated administrative quirks. They are the first visible evidence that the semi-liquid promise becomes fragile when many investors head for the exit at once.

HOW DO EVERGREEN SEMI-LIQUID FUNDS ACTUALLY WORK

Traditional closed-end private funds are typically organised through a sequence of: fundraising, investment period and harvesting. Investors can only enter the fund during the initial period and then can only exit when underlying investments are liquidated. The mechanic is devised to create a perfect liquidity match thus allowing managers to focus solely on the performance of underlying assets.

On the contrary, evergreen semi-liquid funds are structured for access, rather than performance, and their primary goal is to provide an investment experience similar to listed markets, avoiding the complications of commitments and capital calls.

An evergreen private fund is usually a perpetual or semiliquid vehicle that allows investors to subscribe on an ongoing basis and offers periodic redemption windows, often quarterly, commonly around 5% of NAV or outstanding shares, rather than full daily liquidity.

The key complexity is the liquidity mismatch. The underlying assets are typically private loans or private equity stakes, to a wide array of private companies. Those assets can generate cash, like interest payments in private credit, but they are not as easy to sell quickly, transparently and at stable marks as public bond, syndicated loans or listed equity.

So while investors may see a quarterly redemption feature, the fund’s balance sheet remains anchored in assets that are slow to refinance, slow to trade, and vulnerable to discounts if sold quickly.

In order to manage the liquidity promise managers must include a complex suite of tools in their funds, typically:

- Keeping a sleeve of liquid assets available for sale

- Continuous modelling of portfolio cash proceeds (exits, dividends, amortization, interest payments)

- Use leverage and credit lines

- Selling illiquid assets on the secondary market if needed

Blackstone, for example, told investors in a February 2026 filing that BCRED had over $8 billion of available liquidity, more than $5 billion of quoted investments, 0.7x leverage, and a 14% repayment rate in 2025. Cliffwater likewise pointed to a 21% liquidity position and plans to sell about $1 billion of assets, according to recent reporting (source: SEC).

Source: DECALIA

Gates are the ultimate tool that managers activate when all the above fail to be sufficient: these funds are designed precisely so that they do not become forced sellers. The gate protects remaining investors from a run dynamic and prevents a fund from liquidating good assets at bad prices.

These liquidity tools come at the cost of performance, because the paid-in capital is only partly allocated to instruments supposed to capture the illiquidity premium typical of private markets.

Another element of pressure on performance is the need of keeping at all times a high percentage of deployed capital, which can be challenging when large inflows of capital from new investors appear: that pressure to deploy can increase the adverse selection risk.

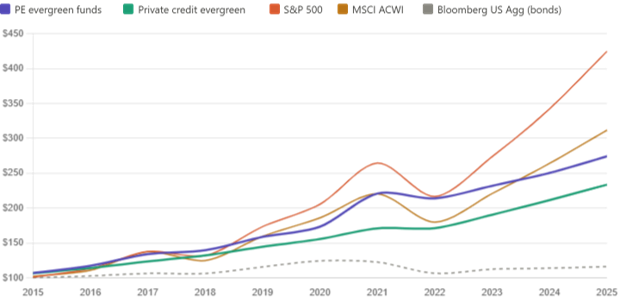

The above graph shows an average performance of evergreen funds vs. listed markets.

Cumulative growth of $100 – 2015 to 2025

Illustrative index-based estimates. PE evergreen: Morningstar/PitchBook & Hamilton Lane 13-fund analysis; Private credit evergreen: MSCI US Evergreen Credit Index & BDC averages. Public benchmarks: total return indices. Returns net of fees where applicable. Past performance does not guarantee future results.

Another important element to take into consideration is how valuations are carried out in semi-liquid funds.

Investors know that “fair value” is the result of the supply-demand equation: when supply exceeds demand the value of the assets decreases.

In public markets this price discovery exercise is carried out continuously from the interaction of buyers and sellers, each incorporating private information.

In private markets however the value is determined by periodic appraisal valuations of the underlying investments, typically conducted by third-party valuers. This is not price discovery – it is price administration: a professional judgment about value at a point in time, deliberately insulated from flow dynamics.

NAV-based pricing in closed vehicles rests on two arguments: first, that the underlying assets are long-duration and fundamentally valued, so short-term flow pressure is noise, not signal; second, that redemption gates exist precisely to prevent fire-sale distortions from contaminating the valuation of remaining investors’ assets.

Investors looking at evergreen semi-liquid funds should be aware of this important distinction: we will explore in a later paragraph the potential distortions that this may create in times of high volatility.

WHO ARE MARKET PARTICIPANTS

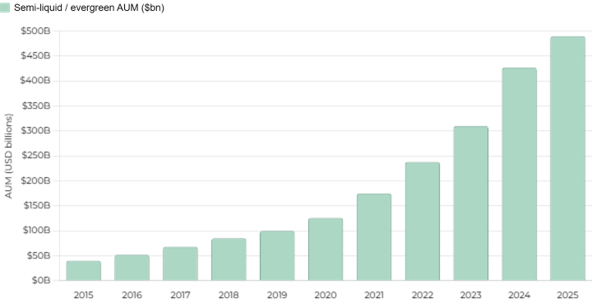

MSCI reports that in March 2026 evergreen / semi-liquid structures were “rapidly approaching $500 billion in AUM,” after growing more than 30% over the prior 12 months.

Within that, private credit is the dominant strategy. According to PitchBook direct-lending evergreen AUM had tripled since 2022, including both non-traded BDCs and interval funds.

The manager concentration is also striking, for example Blackstone said in a February 2026 filing that BCRED had become the world’s largest private credit fund with about $82 billion in total investments.

The most important angle, though, is who the end-investors are. The growth engine here has been the private-wealth channel.

MSCI wrote that wealth investors now account for about one-fifth of evergreen AUM. PitchBook and related market commentary described wealth-focused evergreen vehicles as one of the fastest-growing areas in private markets.

A Morningstar’s 2025 reporting on Cliffwater explicitly said that the firm stood out for raising billions without relying on institutional sources, underscoring how central wealthy individuals and advisers have become.

That does not mean institutions are absent but the strategic push in evergreen products has plainly been about reaching individual investors, high-net-worth clients, and adviser-led wealth platforms rather than merely reinventing institutional LP formats.

So the best answer to the question “retail or institutions?” is: the capital base is mixed, but the marginal growth story is overwhelmingly wealth-driven.

Institutions helped validate the structure; private banks, advisers, HNWIs and affluent investors helped scale it.

REDEMPTIONS & GATES: FINANCIAL, REPUTATIONAL, LEGAL RISK ?

The marketing language across the industry has been consistent: access, democratization, institutional quality, convenience, income, and efficiency.

Managers recurrently used phrases as “providing access to institutional-quality private markets”; “democratization of private markets” and “better experience for individual investors”.

None of those statements are necessarily false. The problem is one of emphasis. When products are framed around access and smoother user experience, less sophisticated investors may hear “private markets, but easier”. They may not internalize the harsher truth: the liquidity is conditional, limited, and procyclical.

Source: DECALIA

If wealthy and retail-adjacent investors conclude that “semi-liquid” was presented as comfort while the real economics were closer to an illiquid fund with a customer-service overlay, then the industry could face the same kind of post-crisis backlash that hedge funds faced: more litigation around disclosures and suitability, more scrutiny of valuation methods and adviser compensation, and more skepticism toward distribution practices that blur the boundary between sophisticated and non-sophisticated clients.

Recent FT reporting on fee-sharing arrangements between private-markets firms and wealth distributors only adds to that concern, because it raises the question of whether products are being selected for fit or for economics.

The threat to private markets is now confidence risk, a trust test similar to that experienced by the hedge fund industry following the global financial crisis.

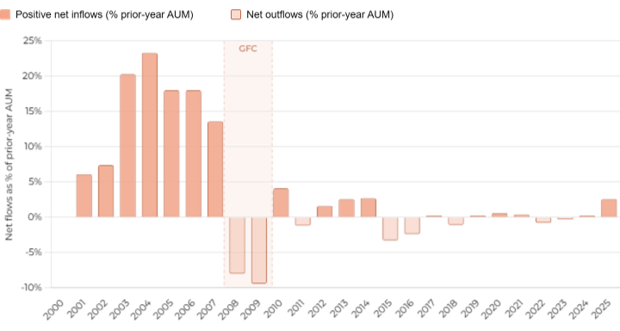

What did this mean for the hedge funds? At first glance, it translated in only 2 years of negative outflows followed by an interrupted run up to the current record high: the industry peaked $1.93tn in 2007 than lost 30% through 2009, recovered to peak in 2011-2012 and eventually has now reached a record high of $4.6tn (HFR Global Hedge Fund Industry Report; Barclays Hedge; Wikipedia; AuM reported to major databases).

However, the analysis of net new money without the market effect tells a different story.

Net new money allocated to hedge funds has been practically flat for a decade vs almost $2tn of performance gains. +15% new inflows per annum before 2007 collapsed to zero-to- negative for most years, including good years. The industry has been living off retained capital, not fresh conviction, until 2025, which marked a genuine inflection point.

Despite the general mistrust and anger of investors, there has been little litigation over hedge fund gates, but several cases related to mis-selling and suitability.

Fund documents invariably reserved the right to gate redemptions in explicit terms, making it very hard to argue breach of contract. Also, institutional investors — the predominant allocators — tend to resolve disputes privately to preserve commercial relationships.

Hedge fund industry – net new investor flows

Net flows as a share of prior-year AUM normalises for the growing size of the industry, making the pre- and post-GFC comparison meaningful. The pre-GFC era saw inflows of 10–15% of AUM annually. Post-GFC flows are consistently near zero or negative — investors stayed in but stopped adding. 2025 is the first year since 2007 where net inflows exceeded 2% of AUM. Sources: HFR; Bloomberg.

On the other hand, many institutional investors brought suits against Wall Street banks that structured and marketed mortgage-backed securities, collateralized debt obligations, and other complex financial instruments.

While these cases focused on structured products rather than hedge funds specifically, they established the legal template. In Europe, the pattern was similar but applied to derivatives: following the financial crisis of 2008, Italian public authorities filed thousands of legal actions against banks seeking redress for complex derivatives transactions, alleging that the transactions were mis-represented as hedges when they were actually speculative, that banks had not explained the nature and risks of the products, and that had failed to assess the investor’s risk profile (legal cases: Bear Sterns “High Grade Structured Credit Fund” 2007-2009; Banco Santander “Optimal Services” 2009; Picard vs Citibank, Merrill Lynch; Natixis, ABN Amro, Nomura, BBVA, Fortis 2010; Italian Public Authorities vs Multiple Banks from 2008).

Bank distributors largely escaped claims, on the ground of extensive risk disclosures in products offering, providing strong contractual protection. Suitability obligations for sophisticated or institutional investors were, and remain, far weaker than for retail clients. Private banking clients — who were the main victims of inappropriate hedge fund distribution — were typically classified as “professional” investors, reducing the legal duty of care owed by their bank.

Rather than investor lawsuits, it was the regulatory response that drove change. The Dodd-Frank Act in the US (2010) mandated SEC registration and specific reporting for large hedge fund advisers.

The EU’s AIFMD (2011) imposed marketing, disclosure, and risk management obligations on fund distributors. MiFID II (2018) significantly tightened suitability and appropriateness requirements for complex product distribution across Europe — requirements that were a direct reaction to the post-GFC evidence of mis-selling, even if the courtroom cases had been limited. In essence, regulators did what investors chose not to do: impose accountability on the distribution chain.

Another material question is posed by valuations. We discussed in an earlier paragraph how private markets exercises price administration rather than price discovery given the nature of the underlying illiquid investments. However, during periods in which redemption requests are unusually high relative to subscriptions, it is reasonable to question whether the published NAV continues to provide a fair representation of the value of the underlying securities. This question becomes even more pressing when managers choose to sell illiquid assets in secondary transactions at a discount. In such cases, should that discount be incorporated into the official NAV extending it to remaining assets?

The standard defence of NAV-based pricing in closed vehicles rests on two arguments: first, that the underlying assets are long-duration and fundamentally valued, so short-term flow pressure is noise, not signal; second, that redemption gates exist precisely to prevent fire-sale distortions from contaminating the valuation of remaining investors’ assets.

Nevertheless persistent net redemptions may hardly been seen only just as operational events, but rather they are signals. In a NAV-administered vehicle, these signals are explicitly suppressed.

Source: DECALIA

Listed closed-end funds provide a clear natural evidence. Shares trade frequently at 10-30% discounts to NAV as a result of the incorporation of the demand/supply dynamic of those shares. The market’s assessment of the portfolio’s worth diverges from the manager’s. Investors in evergreen vehicles are exposed to the same economic reality, but without the price signal.

CONCLUSIONS

It is difficult to draw robust guidance from past episodes with a high degree of confidence, given the meaningful differences between those precedents and the current market context.

The evergreen boom was built on a compelling proposition: to broaden access to institutional private markets without importing the most burdensome operational constraints of traditional private funds.

The current wave of redemption requests may point to a degree of misunderstanding between managers and investors. Semi-liquid structures can reduce some of the operational frictions associated with traditional private funds, but they cannot eliminate the underlying complexity and latent liquidity risk of the assets they hold.

Like it happened in the hedge fund industry after 2008, there is a meaningful possibility that fundraising for these vehicles will become temporarily more challenging.

Semi-liquid / evergreen fund AuM growth

Sources: Deloitte 2024 global semi-liquid fund study; MSCI Private Capital in Focus 2026; Morgan Stanley / PitchBook (Q3 2024); IQ-EQ / Preqin; SS&C ALPS Advisors (2025). 2015–2019 are back-cast estimates from industry data. 2025 figure reflects MSCI estimate of ~$490bn (>30% YoY growth through September 2025).

From a legal perspective, however, it is difficult to imagine material potential consequences at this stage, if any. Even if retail-type investors now represent a significant share of demand for these products, the regulatory framework is not the same as it was during the hedge fund stress episodes of 2008. Suitability and appropriateness rules are already in place; eventually the key question is whether they were applied rigorously and consistently.

This time round also regulators have, in some respects, encouraged this trend, as illustrated by initiatives such as the European Union’s efforts to promote retail-oriented structures like ELTIFs. Arguably, in this cycle, market enthusiasm has been shared by both product manufacturers and policymakers.

At the same time, private markets may have involved less ambiguity than hedge funds in the way liquidity was presented. Hedge funds may have been perceived as liquid products that could become temporarily illiquid under stress, whereas private market vehicles have more often been marketed as fundamentally illiquid investments with limited exit windows.

In any case private markets managers are very concerned about keeping intact the trust and reputation with investors, as it is evident from the temporary increase of redemption limits proposed by some funds (those who could afford it).

Valuations in evergreen funds are also an issue: can investors trust the NAV? The honest answer is “conditionally”. NAV can be trusted as good-faith estimates of intrinsic long-run value when underlying assets are frequently transacted, valuers have genuine independence, the fund’s flow dynamics are orderly and realisations are tracked against book value over time. Lacking the above, NAV should be treated with considerable scepticism.

Investors must be conscious that in public markets the price mechanism performs a continuous reconciliation between beliefs about value. In semi-liquid private funds, that reconciliation only occurs episodically – at the moment of realisation – and by then, the investor who redeemed at the administered NAV and the investor who remained have already experienced an irreversible wealth transfer between them. The gate is not just a liquidity mechanism. It is, in the absence of continuous price discovery, the only moment of truth — and it arrives far too late for those caught on the wrong side of it.

All the above considerations are legal, operational and somewhat philosophical. They should not distract from what ought to remain the central focus for investors. The economic rationale of private markets rests on a simple premise: investors accept reduced liquidity in exchange for the prospect of excess returns relative to listed assets. The illiquidity premium exists because private assets are more difficult to source, analyse and manage, and because information is less broadly and efficiently disseminated across market participants.

In our view, the evergreen frenzy may contribute to longer-term challenges for private markets in at least three respects.

- Reduction of information asymmetry: the democratization of private markets is contributing to the industry’s rapid expansion. As investor appetite broadens, the number of market participants is likely to increase, gradually eroding one of the main traditional sources of alpha: information asymmetry.

- Focus shift from performance to operations: the growth of evergreen structures requires managers to devote increasing resources to liquidity management, distribution, investor servicing and operational infrastructure. This may divert attention and capabilities away from core investment functions and, over time, weigh on return generation.

- Pollution of the risk-return profile: meeting the complex operational requirements of evergreen funds has a performance cost, while the underlying investment risks remain unchanged. Exchanging part of the illiquidity premium for operational convenience may prove a fundamentally unattractive trade-off for investors.

On this basis, should investors reconsider their allocation to private markets?

Not really, but investors must incorporate deep technical knowledge in their analysis.

The opportunity set in the non-listed economy is substantially larger than that of public markets. For many investors, it would therefore make little sense to forgo private markets altogether.

However, alpha is likely to become increasingly scarce. Simply buying broad exposure – or the private-market equivalent of an “index” like many evergreen strategies effectively propose – may no longer be sufficient to justify reduced liquidity.

Investors will need to sharpen their sourcing and underwriting capabilities, identify opportunities with greater precision, and focus on areas of genuine specialization where alpha is more likely to remain durable.

Source: DECALIA

Finally, structure matters. Investors allocating to open-ended semi-liquid vehicles should recognize that performance may be influenced not only by the underlying assets, but also by the behaviour of other investors in the fund. Short-termism and emotionally driven redemption decisions in semi-liquid vehicles – a pattern more commonly associated with less institutional investor bases – can impose costs on investors who understand that value creation in private markets is realized only over the long term and opt to remain in the fund.

At the same time, investors should carefully assess the cost of the operational features embedded in fund structures and the impact it creates on the net performance.

All these elements must be thoroughly considered by investors to determine the most appropriate investment strategies and structures for their own portfolio allocation.

Copyright © 2026 by DECALIA SA. All rights reserved. This report may not be displayed, reproduced, distributed, transmitted, or used to create derivative works in any form, in whole or in portion, by any means, without written permission from DECALIA SA.

This material is intended for informational and marketing purposes only and should not be construed as an offer or solicitation for the purchase or sale of any financial instrument, or as a contractual document. The information provided herein is not intended to constitute legal, tax, or accounting advice and may not be suitable for all investors. The market valuations, terms, and calculations contained herein are estimates only and are subject to change without notice. The information provided is believed to be reliable; however DECALIA SA does not guarantee its completeness or accuracy. Past performance is not an indicator of future results.

Some of the information presented in this paper is based on the direct experience of DECALIA as manager of collective investment schemes such as DECALIA Private Credit Strategies. Any intended or implicit reference to DECALIA Private Credit Strategies is not meant to represent a solicitation for the purchase or sale of the strategy or other strategies of DECALIA. Private markets strategies are not destined to the large public and its suitability must be evaluated in relationship to the risk profile, objectives and financial situation of any investor and the rules and limitations of each jurisdiction.