Let me reassure you right away: this week, I am not going to talk about Cagliari Calcio, which still isn’t officially safe from relegation after its undeserved loss 0-2 against Udinese, the conflict in Iran and its consequences on energy flows and prices (73 days long already and still counting), nor about the anthrax virus, which may eventually fuel additional geopolitical and health concerns. And I will not even dwell too much on the extraordinary speed at which AI is already reshaping our lives, our economies, and financial markets. No, the piece of news that caught my attention over the past few days was far more light-hearted, almost anecdotal: FIFA is ending its historic partnership with Panini after more than 60 years.

For an entire generation, Panini and the World Cup belonged to the same mental universe, especially in Switzerland, which is considered one of Panini’s strongest markets per capita. The albums, the stickers, the duplicates exchanged in school playgrounds… it all felt almost a permanent part of the World Cup soccer scene. And yet, even that is changing. This small story ultimately says something rather important: the old world no longer really exists. Or more precisely, no institution, no economic relationship, and no market dynamic is eternal. The world evolves -sometimes slowly, sometimes abruptly- but it evolves constantly: “There are decades where nothing happens, and there are weeks where decades happen” according to the famous quote attributed to Lenin. And this observation obviously applies to financial markets and economic indicators as well.

Back in the 1990s and early 2000s, some economic data releases had an almost sacred status. The US trade deficit and current account deficit could move the dollar immediately. Markets viewed these imbalances as critical drivers of the US currency. Similarly, the US ISM Manufacturing Index (still known as the NAPM at the time) was probably one of the best thermometers of the US and thus global business cycle. Every release at the very beginning of the month was scrutinized carefully and impacted both equities and bonds depending on the level, trajectory and the upside or downside surprise, at the aggregate level but also within these main asset classes (cyclicals vs defensives or sovereign vs. credit rotations). Today, however, the US economy has become far more service-oriented, while manufacturing represents a smaller share of overall activity. This structural shift has gradually reduced the explanatory power of the manufacturing ISM, partly compensated by the introduction of the ISM Services Index in the early 2000s.

The same applies to inflation and fiscal deficits. For a few decades, bond markets in major developed economies could largely ignore these issues, except during occasional episodes of stress. Investors implicitly assumed that most developed markets enjoyed a form of almost permanent fiscal credibility. Large deficits during recessions were usually followed by a degree of fiscal restraint during periods of economic prosperity. At the time, fiscal concerns and inflation issues were mostly associated with emerging markets or certain peripheral European economies such as Italy, Spain, Portugal, or Greece. The irony today is that some of these former “problem children” now appear almost more disciplined than several major developed economies. The new dunces have changed.

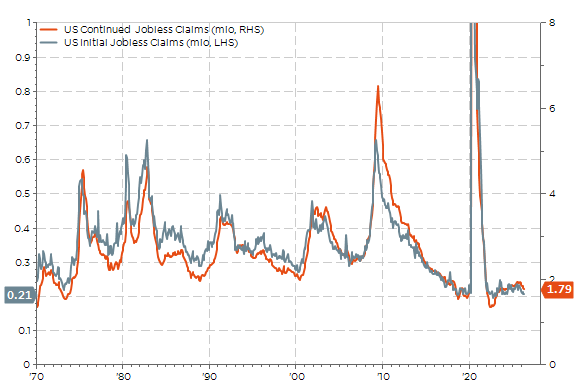

This broader shift is particularly visible today in the US labor market too. For decades, strong economic growth and significant job creation were necessary to maintain full employment. Likewise, weekly jobless claims above 400k were once considered a sign of a deteriorating labor market. That was two decades ago, at a time when the total number of civilian employees was about 140mio. Today, there are about 165mio employees and the latest weekly initial jobless claims were just 200k, a number would have looked almost impossibly low twenty years ago.

How low can you go? US weekly initial jobless claims (LHS) and continued jobless claims (RHS) in million

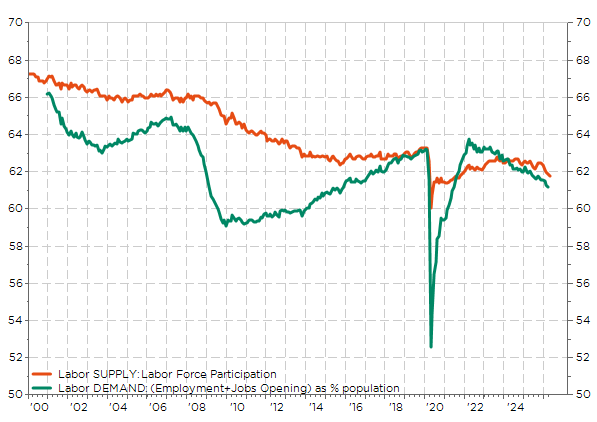

Today, the reality is different. Why? The US economy appears to require less growth and fewer job creations to maintain a relatively balanced labor market. Because labor supply and labor demand are now slowing simultaneously. Immigration has been halted in the US, whereas demographic aging is profoundly changing economic equilibria. The labor force is growing more slowly, hiring needs are moderating as well, and the threshold required to maintain full employment is mechanically declining.

US jobs supply & demand as % of population: trending down in tandem

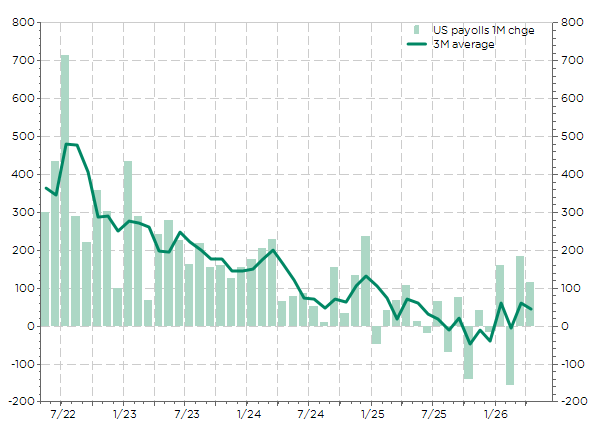

This is already visible in other aging economies such as Japan or large parts of Europe. Despite weak -and most of time mediocre to negligible – economic growth, unemployment, which was the primary concern of governments for several decades, is no longer necessarily the dominant source of government anxiety, despite the mounting difficulty of youth to enter into the labor market. As a result, economists now estimate that US economy needs to add about +50k additional payrolls per month to maintain a stable unemployment rate, while we were speaking about 200k when I started my career in the early 2000s.

US monthly and 3M average payrolls: neither weak or strong enough to alter current “wait and see” Fed’s policy outlook

Since then, political and social priorities have shifted. Today, purchasing power, housing costs, service inflation, and public finances dominate the debate. Or are clearly part of the game at least! Even central banking itself, and the way monetary policy is conduct, have changed dramatically over the past twenty-five years. Under Alan Greenspan, the Fed cultivated opacity almost as a policy tool. Greenspan famously joked that “If I seem unduly clear to you, you must have misunderstood what I said.” Fed minutes were published with a considerable delay and carried far less market relevance than they do today. Forward guidance barely existed, transparency was limited, and the central bank’s balance sheet was not considered an active monetary policy instrument.

Which is also why there is a strong probability that a future Fed Chair such as Kevin Warsh would introduce his own changes to the institution. It will certainly take time but a Warsh-led Fed may likely place greater emphasis on market discipline, less reliance on prolonged balance sheet interventions, and potentially a less activist communication style than the one markets have grown accustomed to over the past decades.

In conclusion, economic history regularly reminds us of one simple reality: markets change, indicators change, and priorities change. And investors must adapt accordingly. Because unfortunately -or fortunately, depending on one’s perspective- nostalgia has never been an investment strategy.

Economic calendar

All the eyes will be on the US inflation this week with the April CPI release on Tuesday. The consensus expects headline CPI to increase +0.6% MoM (+0.9% the prior month) with the annual inflation rate accelerating to 3.7% from 3.3%. More importantly, investors, as well as policy makers, will rather scrutinize the core index, foreseen to edge up +0.3% MoM (vs. +0.2% in March) and to tick up to 2.7% from 2.6% on annual basis, in order to be sure that little-to-no second-round effects are diffusing to the less volatile and not energy-related components of consumer price index.

On the same day, we will also get inflation data in Germany (final data for April) and Brazil, while the US PPI will follow the following day (Wednesday). Finally, China CPI and PPI did already pop up on our screen this morning. China PPI annual inflation rose from 0.5% in March to 2.8% last month on the back of imported price, with jumps in the price of fuel and petrochemicals essentially. As a result, these price pressures are relatively narrow in scope and consumer price inflation remained therefore fairly subdued too, only edging up slightly from 1.0% to 1.2%. Note that China PPI turned positive in March for the 1st time in… 41 months! Higher PPI does not necessarily lead to rising interest rates, unless domestic demand and bank lending also recover, which is not the case currently. The ingredients for a sustained reflationary impulse still appear to be missing indeed as overcapacity issues are unresolved and domestic demand remains sluggish.

As far as activity data and sentiment are concerned, the main releases will be the US NFIB Small Business Index (Tuesday), the 2nd estimate of the Euro Area Q1 GDP (Wednesday), the US April retail sales (Ascension Thursday) and the US industrial production (Friday). For the latest two, consensus still expects positive/resilient real growth.

Turning to geopolitics and international trade, next week’s summit between Xi and Trump on May 14-15 seems unlikely to deliver much beyond a continuation of the existing truce, although a shift in US language on Taiwan in exchange for pressure on Iran or large-scale purchases of US goods can’t be entirely ruled out. Soybeans, Rare Earth, Semiconductors could be also be put on the trade negotiations table. Wrapping up with the US earnings season, which is winding down as we wait for Nvidia’s earnings (on May 20), we’ll see the results from Alibaba and Cisco (Wednesday) as well as Applied Materials (Thursday) in the meantime.

This is a marketing communication issued by DECALIA SA. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The information and data presented in this document are not to be considered as an offer or invitation to buy or sell any securities or financial instruments nor to subscribe to any services. The information, opinions, estimates, calculations etc. contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Investments in any securities or financial instruments may not be suitable for all recipients and may not be available in all countries. This document has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Before entering into any transaction, investors should consider the suitability of the transaction to individual circumstances and objectives. Any investment or trading or other decision should only be made by the client after a thorough reading of the relevant product term sheet, subscription agreement, information memorandum, prospectus or other offering document relating to the issue of the securities or other financial instruments. Where a document makes reference to a specific research report, the document should not be read in isolation without consulting the full research report, which may be provided upon request.