After a breathless first half, the teams finally head back to the dressing room. The opening six months of 2026 have delivered enough twists and turns to fill an entire season. It all started at breakneck pace with the spectacular arrest of Nicolás Maduro, before investors were thrown into months of geopolitical suspense as tensions around the Strait of Hormuz kept oil traders, central bankers and portfolio managers glued to their screens. Just as markets thought they had become experts in tariff headlines, inflation staged an unexpected comeback, reclaiming center stage in central bank discussions.

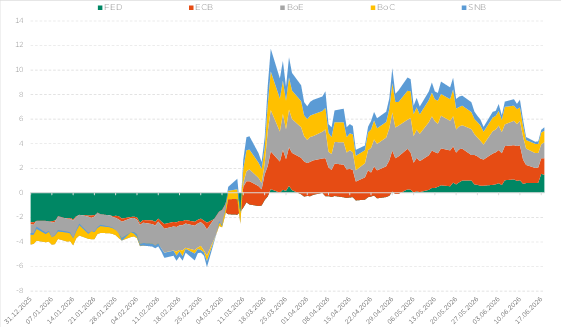

The consequences were swift. The Fed’s long-awaited easing cycle, confidently penciled in by markets at the start of the year, was kicked well into the long grass. The Bank of England followed the same playbook, while even the ECB -expected to remain on the sidelines- felt compelled to hike again its target rate last month.

The tide turned…

Expectations of rate cuts/hikes for this year

Yet, despite all the noise, the scoreline at half-time is probably not what many had expected back in January. The global economy has once again proved remarkably resilient. Corporate earnings have continued to surprise on the upside, fueled by an AI investment boom that shows few signs of slowing, but also by governments opening their wallets to strengthen energy security, critical infrastructure and national sovereignty. Once again, recession forecasts have struggled to survive contact with reality.

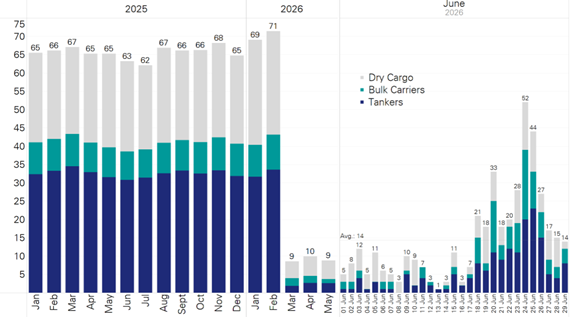

Hormuz off, Hormuz on…

SoH exits have picked up, but remain below pre-conflict levels

Source: Deutsche Bank

So, what can possibly happen over the summer? After months of relentless headlines, perhaps the biggest surprise this summer could be… the absence of surprises as the second half may not really begin until September.

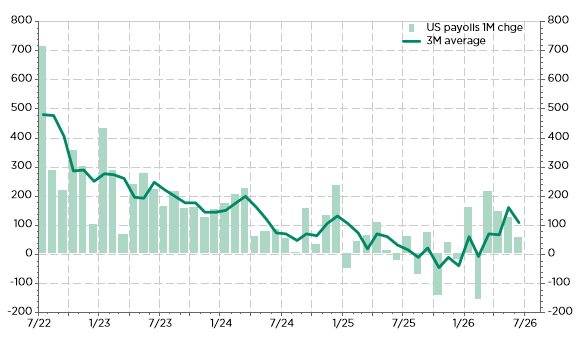

For the first time in what feels like forever, investors are no longer waking up every morning wondering whether the macro narrative has fundamentally changed overnight. The dust has finally settled. Kevin Warsh’s speech in Sintra last week reinforced the view that inflation is moving in the right direction and that the Fed can afford to be patient rather than pre-emptive. Likewise, June’s US employment report (slightly softer than expected but far from alarming) helped cement the idea that the next move from the Fed is unlikely to be another hike anytime soon.

US 1M payrolls change: not too hot, not too cold

Barring an upside surprise in the next US CPI, which will be released on 14 July, a sharp deterioration in growth, or yet another geopolitical plot twist courtesy of Donald Trump, the macro landscape suddenly looks remarkably… predictable. Growth should remain reasonably solid. Inflation should continue its gradual descent. And central banks may have finally earned themselves something they have not enjoyed for quite some time: the luxury of doing nothing. For markets, that may prove to be the most supportive outcome of all. For investors, that means the motorway to the summer holidays looks unusually clear. Seatbelts fastened, sunglasses on, plenty of hydration pauses along the way… and hopefully no unexpected roadworks (unless you have to drive through Geneva).

The irony, of course, is that doing nothing has once again turned out to be one of the year’s most successful investment strategies. That said, investors should resist the temptation to switch off completely. The next major test begins next week with the start of the second-quarter earnings season. After all, earnings, not geopolitics, not tariffs, not central banks, have been the single most important driver of equity markets this year, particularly in the US as the S&P 500 forward P/E has even decreased somewhat over the last few quarters. Consensus expects another very healthy quarter, with S&P 500 earnings projected to grow by around 22% year-on-year. That may sound ambitious, but it follows an even stronger 27% expansion in Q1. Strip out the mega-cap technology companies, however, and the picture becomes considerably less spectacular, but still remarkably solid, with median earnings growth expected to slow to around 9% from 13% previously.

Investors will also pay close attention to margins. Can companies continue to absorb higher labor costs and energy/tariff-related pressures without passing them on to consumers? The answer will matter not only for earnings, but also for the inflation outlook and, ultimately, for monetary policy.

But above all, one question continues to overshadow every other: is the AI investment supercycle still intact? Markets will thus be watching whether hyperscalers continue raising capital expenditure budgets or whether management teams begin hinting at a more disciplined spending path. Increasingly, investors are also asking the next logical question: when will all these investments start generating meaningful returns? The conversation should shift, at some point, from AI CapEx to AI ROI.

Even “token-maxxing”, i.e. the explosive growth in token consumption that has fueled infrastructure demand, has become a genuine line item in corporate cost structures. At some point, companies will need to demonstrate that ever-growing AI bills translate into higher revenues, better productivity and stronger profits. Until then, little else really matters.

Economic calendar

With the second half of 2026 having just kicked off, investors shouldn’t be too overwhelmed this week, given the light economic calendar with no significant macroeconomic data releases, no meetings of major central banks, and no crucial earnings reports yet (Q2 earning season will officially begin on Tuesday 14 July with the results of some major US banks).

In this context, investors will certainly have time to travel to their vacation destinations or watch the World Cup last round of 8 matches (Switzerland will play against Colombia Tuesday at 10pm) and the first quarterfinals (France-Morocco on Thursday at 10pm). Among the few key releases to keep an eye on, there will be:

- The US ISM services index on Monday, where the consensus foresees solid activity expansion to hold (54.1 in June expected vs. 54.5 in May) and prices pressures to ease (prices paid component expected to decline to 67.5 from 71.3)

- The FOMC minutes from last month meeting (Wednesday), the first under the new regime of Chair Kevin Warsh. Earlier on the same day, the Reserve Bank of New Zealand is expected to deliver a 25bp hike, taking its benchmark rate to 2.5%

- China CPI and PPI for June (Thursday), where deflation risks may come back in the forefront with the recent drop in energy prices and the ongoing subdued domestic demand and involution occurring in China

- Some inflation prints on Friday with the final reading of June CPI in France and Germany, but also June inflation figures in Denmark, Norway or Brazil.

- German activity indicators for May, including factory orders (Monday), industrial production (Tuesday) and the trade balance (Thursday).

Investors will also pay attention to the NATO summit (Tuesday and Wednesday) in Ankara (Turkey), where Russia-Ukraine conflict may come back in the forefront, whereas the US will likely continue to pressure European allies to carry more of the security burden.

This is a marketing communication issued by DECALIA SA. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The information and data presented in this document are not to be considered as an offer or invitation to buy or sell any securities or financial instruments nor to subscribe to any services. The information, opinions, estimates, calculations etc. contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Investments in any securities or financial instruments may not be suitable for all recipients and may not be available in all countries. This document has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Before entering into any transaction, investors should consider the suitability of the transaction to individual circumstances and objectives. Any investment or trading or other decision should only be made by the client after a thorough reading of the relevant product term sheet, subscription agreement, information memorandum, prospectus or other offering document relating to the issue of the securities or other financial instruments. Where a document makes reference to a specific research report, the document should not be read in isolation without consulting the full research report, which may be provided upon request.