Markets, much like sports, have a habit of humbling consensus views just when confidence appears strongest. In Italian Serie A football, Cagliari is all but safe from relegation following its impressive and unexpected victory over Atalanta (3-2) and its well-deserved draw against Bologna (0-0). In the NBA, the past few days have delivered a similar lesson: a first round of playoff dominated not by certainty, but by tension, resilience and an unusual number of Game 7s, “Where Amazing Happens” as the smallest momentum shift has repeatedly overturned expectations. Financial markets have offered their own version of these surprises. In recent weeks, some of the traditional safe havens that investors instinctively turn to during periods of uncertainty such as government bonds, the Swiss franc and gold have failed to behave according to the usual script. Correlations that once seemed reliable suddenly looked fragile, leaving investors to navigate a market where historical reflexes no longer guarantee protection.

As in sport, the current environment is a reminder that periods of stress rarely unfold exactly as anticipated. Favorites stumble, outsiders seize opportunities, and strategies built on old certainties can quickly be tested by a changing landscape. Consequently, it is hardly surprising that investors are questioning, more than usual, how to protect their portfolios in the current environment. “But against what exactly?” is the missing part to eventually deliver a useful answer. Inflation risk? Rising interest rates? Or a severe economic recession?

Before addressing the central question of how to protect a portfolio, two preliminary remarks are necessary. First, it is far from certain that the next recession is as imminent as recent market fears suggest. Admittedly, the conflict in Iran and the energy crisis resulting from the disruption of the Strait of Hormuz are increasing risks and will undoubtedly weigh on growth, thereby slowing economic activity. However, the base-case scenario still remains one of continued economic expansion over the coming months. Second, in order to properly answer the question of how to protect a portfolio, one would ideally need to understand beforehand what the underlying causes of these potential problems are likely to be, how intense and long-lasting they may become, what policy responses – both monetary and fiscal- will be implemented (or not), and what the longer-term consequences could eventually be. Otherwise, it would be akin to asking a doctor to prescribe a “miracle cure” against illness in general.

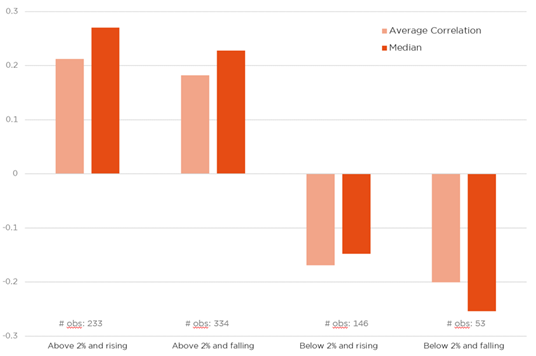

In one of my previous weekly letters, I had already discussed the reasons why bonds may fail to act as a safe haven by providing diversification in the current environment («More inflation, less growth and some headaches for central bankers», 16 March 2026). Put simply, when inflation is already problematic -meaning above central bank targets- and continues to rise, the diversification benefits traditionally associated with bonds tend to disappear.

Don’t expect govies to always be a diversifier to your equity allocation!

Historical Equity/Bond 1y correlation depending on US inflation levels & trends (monthly data since 1962)

This is even more true when inflation is triggered by war or uncontrolled public deficits (see the NBER research paper “Are government bonds safe in times of war and pandemics?”). In such circumstances, equities themselves may ultimately prove to be the best protection to preserve the purchasing power of savings. A protection or a safe haven, in certain circumstances, may indeed come with its own risks and volatility…

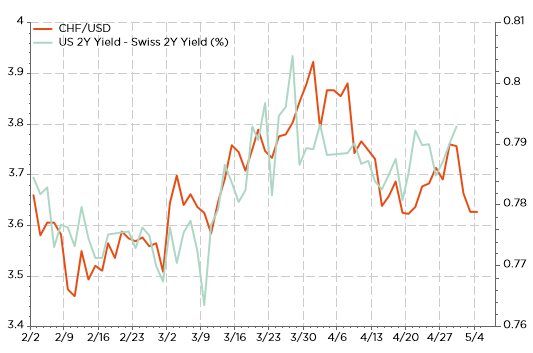

As for the Swiss franc, the explanation is relatively straightforward if one considers that the primary effect of the current energy shock is to fuel inflation and force central banks to reassess their monetary policy trajectories over the coming months, potentially leading to rate hikes in the euro area and delaying rate cuts in the United States. So that’s not the usual risk-off shock’s playbook leading to… lower rates! In fact, basic rules of thumb suggest that a $10 per barrel increase in oil prices typically acts as a tax on consumers, raising headline inflation by approximately 0.3–0.4% while reducing global GDP growth by around 0.1% to 0.2% over the following year. This also explains why markets remain relatively calm for now regarding growth prospects, as economic activity continues to display a degree of resilience. In such an environment, interest rate differentials become the key driver behind many currency pairs. With rates rising faster outside Switzerland than domestically, it is therefore not surprising to see the Swiss franc weaken when crude oil prices rise and strengthen again when they retreat.

“CHF/USD (RHS) & US-Swiss 2-year bond yields: it’s the interest rate differential, stupid!”

Let us now return to our main subject and assume instead that we are facing a more traditional recession caused by a sharp collapse in demand, leading to a sudden decline in equity markets. In that scenario, inflation fears would likely fade rapidly, central banks would cut rates, and public spending would partially offset the gap left by the private sector. In such a context, sovereign bonds or very high-quality fixed-income assets would probably outperform (at least initially) alongside gold and more defensive assets such as the Swiss franc, as well as equities in less cyclical sectors (healthcare, consumer staples, etc.) featuring strong balance sheets, good business visibility, high margins and, ideally, reliable dividend streams.

More broadly, investors should favor mature and liquid markets (notably the United States), quality assets across equities, bonds and currencies alike, as well as simplicity and transparency, i.e. avoiding black boxes or overly complex structures that often generate unpleasant surprises in finance. Holding a certain amount of cash can also prove useful, both to dampen volatility and to seize opportunities that inevitably emerge during periods of crisis. However, since it is extremely difficult to predict the timing, intensity, duration and longer-term consequences of such scenarios — and therefore unrealistic to believe that one can completely reposition a portfolio just before turmoil strikes — investors should always maintain at least some exposure to these defensive ingredients, depending on their risk profile and convictions.

Finally, it is always possible to purchase insurance through option strategies designed to cover part of the downside risk should a market accident occur. But here too, there is no perfect solution. The cost can become prohibitive, especially once smoke is already visible on the horizon, and there is never any guarantee that all the hidden risks embedded within a portfolio will be fully covered. Once again, the parallel with everyday life and sports is quite fitting: despite all the precautions we take and the many insurance policies we buy, it is rarely possible to eliminate all the risks inherent to daily life. For investors, “zero risk” unfortunately does not exist. The best one can do is manage risk as effectively as possible. And, to borrow a famous NBA slogan, that is precisely why “I Love This Game.”

Economic calendar

Welcome to May! A month when you “do whatever you like” according to the French idiom… though markets or Donald J. Trump may still insist on having the final word. The main highlight of the week, according to the known macro agenda, will be the US April jobs report due on Friday. The consensus foresees payrolls increasing +65k, down from +178k in March, with a slightly faster wages growth rate (+0.3% vs +0.2% in March) and a steady unemployment rate at 4.3%. Before that, we will get several other labor market indicators such as the JOLTS and ADP reports, on Tuesday and on Wednesday, respectively, as well as the weekly jobless claims (they fell below 200k last week…) or the ISM services labor-related subcomponent (Tuesday).

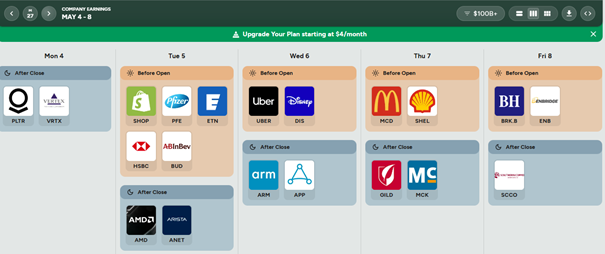

Other US economic data worth considering include the University of Michigan’s consumer sentiment for May (Friday), where some rebound is expected as it reached last month the lowest level ever since this indicator exists (i.e. 1978), the ISM services index (Tuesday) and Q1 unit labor costs and productivity (Thursday). Elsewhere, central banks in Australia, Norway and Sweden will meet and decide about their target rate. The former is widely expected to hike +25bps to 4.35% on Tuesday, supporting the AUD, while the remaining two Nordics should stay pat on Thursday at 4.00% and 1.75% respectively. Staying with central banks, there will also be plenty of speakers from the Fed and the ECB over the next few days. European indicators will include the Swiss April CPI (Tuesday), German factory orders and industrial production in March (Thursday and Friday), whereas UK local elections on Thursday may also impact UK Gilts market and the Cable (GBP/USD). Finally, corporate earnings agenda will be again packed enough to keep my equity colleagues busy and wide-awake with Palantir & AMD in the tech sector, big consumer stocks such as Walt Disney, McDo, AB InBev, Toyota, Sony or Nintendo; or Rheinmetall and Leonardo in defense, among many others.

https://earningshub.com/earnings-calendar/week-of/2026-05-04

This is a marketing communication issued by DECALIA SA. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The information and data presented in this document are not to be considered as an offer or invitation to buy or sell any securities or financial instruments nor to subscribe to any services. The information, opinions, estimates, calculations etc. contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Investments in any securities or financial instruments may not be suitable for all recipients and may not be available in all countries. This document has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Before entering into any transaction, investors should consider the suitability of the transaction to individual circumstances and objectives. Any investment or trading or other decision should only be made by the client after a thorough reading of the relevant product term sheet, subscription agreement, information memorandum, prospectus or other offering document relating to the issue of the securities or other financial instruments. Where a document makes reference to a specific research report, the document should not be read in isolation without consulting the full research report, which may be provided upon request.