- Rare earths are to modern industry what saffron is to cooks: a small but irreplaceable component

- China’s grip on refining makes it the dominant supplier – providing leverage in trade negotiations

- Prices are driven not only by the current demand-supply gap, also by strategic considerations

While the 19th century was coal-powered and the 20th century oil-dependent, this one will likely come to be known as the time of rare earths. Vitamins of modern industry, their importance is strategic to numerous products, ranging from wind turbines to smartphones, and from electric vehicles to the defence sector. As is now widely known, rare earths actually belie their name: they are by no means rare in nature. What makes them strategic is not their scarcity, but their systemic irreplaceability. In fact, rare earths are increasingly described through the “saffron effect”: only a few grams are required, but without them industrial production as a whole – across 43 sectors and 17 supply chains – would come to a halt.

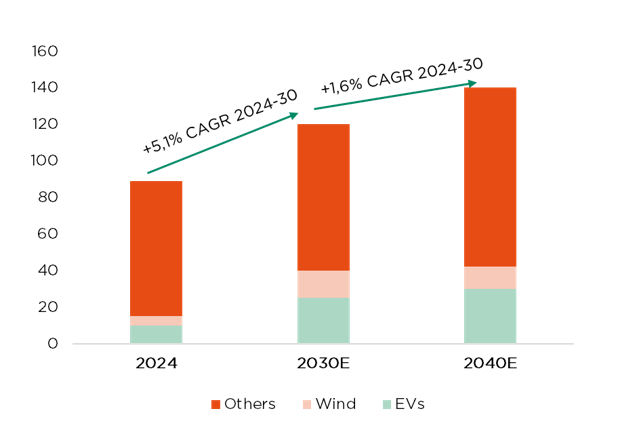

Demand for rare earths rests on three engines: the energy transition, technological advances (AI, digitalisation, advanced electronics) and geopolitics (defence, security, space). The most recent data points to 5% overall annual growth for the next 5 years, but with key segments growing at double-digit rates. Put differently, not all 17 rare earths are equal. Particularly needed are Neodymium (Nd) and Praseodymium (Pr), permanent magnets which form the core of industrial demand, as well as Dysprosium (Dy) and Terbium (Tb), heavy rare earths that are crucial for high-temperature applications and defence.

On the supply side, the real bottleneck lies in refining, not mining. Large quantities of rock must admittedly be extracted to obtain small amounts of rare earths. But it is then the refining stage that is very expensive – as well as environmentally impactful. China’s lower costs have led to the country now dominating production and using this leverage in trade negotiations. Heavy rare earths, in particular, have effectively become a Chinese technological monopoly. And this situation is unlikely to change soon, given the high degree of supply inertia. New projects take a decade or so to mature, with huge funding requirements and numerous environmental/political constraints to overcome.

Faced with Chinese export restrictions, and broader geopolitical tensions, Western countries are attempting to rebuild autonomous supply chains. However, relative to the prior globalised framework, this introduces a new paradigm, one of duplicated facilities, higher structural costs and inefficiencies. The US Department of War is for instance directly financing several domestic extraction companies, including MP Materials (whose main shareholder is, notably, Chinese). And the EU, through its Critical Raw Materials Act, has set ambitious 2030 targets: 10% domestic extraction, 40% local processing and 25% of demand covered through recycling.

The market for rare earths is, however, “imperfect”, meaning that prices do not always immediately reflect the demand-supply imbalance. Inventory levels, government intervention and industrial policies also come into play, making for still distorted and inefficient pricing – more akin to a strategic market than a classic commodity.

As such, the investment approach is also evolving. Understanding that this is no longer just a commodity story, but has become one of exposure to geopolitics, technology and industrial policy, is key. One must also acknowledge that physical markets are illiquid and more efficient exposure can be gained via equity ETFs. Performance drivers lie in reshoring and public incentives, technological demand growth and geopolitical tensions, while the main risks to be borne in mind pertain to execution of new projects, political intervention and non-linear volatility.

To conclude, rare earths are today far more than an industrial trend, they form a critical technological infrastructure. This implies greater state intervention, lower efficiency but higher resilience, pricing that is increasingly influenced by geopolitical factors, and a long-term investment horizon – albeit with short-term dynamics that can be difficult to interpret.

Edoardo Proverbio, Head of Investments DECALIA SIM SpA

Thousand tons & CAGR

Sailing through the strait of worries

- March Madness on the back of oil headlines roulette

- More inflation, less growth and some headaches for central bankers

- We cannot direct the wind, but we can adjust the sails: cautiousness warranted

The prolonged disruption to global energy supply due to the war in Iran and subsequent blockade of the Strait of Hormuz, alongside potential damage to energy capacities in the region, has shifted the global macroeconomic backdrop from a “good place” to a more complex and less favourable one. Risks, doubts and concerns about AI capital spending and disruption, government debt sustainability or private credit issues are still present but have been relegated to the background by this more pressing issue, which may actually even exacerbate them going forward.

With the US military operations in Iran escalating into a broader conflict and leading to the blockade of Hormuz, the Brent crude oil price has been the main market driver. Investors have so far priced in greater near-term inflation risks, which may prevent central banks from easing further this year, while damages to growth, down the road, seem manageable at this stage. As a result, bonds markets underwent a dramatic repricing in March, reflecting these inflation concerns and subsequent more hawkish central bank stance across the world. Global equities also lost ground, with the US market proving more resilient as the country is likely to suffer less from a supply oil shock than Europe or Asia. The widening of credit spreads has been quite contained and orderly to date, reflecting investors views about economic resilience. The US dollar has regained some colour, supported by a more resilient, diversified and “liquid” economy and markets, while gold has not acted as a diversifier, but rather borne the brunt of much higher rates, a somewhat stronger greenback, some profit taking or forced liquidation within less liquid markets. As such, places to hide have been few, outside of cash and the USD to some extent.

In this context, the probability of our central macro scenario has obviously declined. Going forward, we can envisage three main scenarios regarding the Iranian conflict and Brent crude oil price: a short and sharp conflict with the price of Brent returning to pre-conflict level by mid-year, a 1- to 3-month disruption to energy supplies with limited damages to Gulf energy infrastructure and Brent spiking above USD 120 before receding gradually towards USD 80 through year-end, and finally a more severe scenario with lasting damage to energy infrastructure, a spike in the Brent price above USD 150 then staying above USD 100 beyond 2026. With each passing day, the likelihood of the first scenario decreases, while the risks to inflation, in the immediate future, and to growth, down on the road, increase mechanically.

For central banks, the task of delivering the right dose, at the right moment, of the right monetary medicine is becoming more complicated, especially as interest rates are not really the appropriate tool to deal with a supply shock. Furthermore, “higher for longer rates” represent a significant headwind for overall asset valuations, capex, leveraged economic sectors (such as real estate) or just markets participants as it raises the price of money. It is also worth noting that the famous TACO trade (i.e. Trump Always Chickens Out) may not work in this case, as the US President can no longer unilaterally call the end of the war, and even less reopen the Strait of Hormuz or immediately repair the energy infrastructure.

At the portfolio level, we thus decided to downgrade our equity stance from neutral to a slight underweight, which effectively entails a cut of ca. 10% to the prior equity allocation (depending on the risk profile). While the deteriorating macro backdrop is the main trigger for this decision, it was also motivated by still elevated valuations. Meaning that risk assets have little room for absorbing additional shocks on rates and/or growth. Remember also that tactical protections were implemented in portfolios with medium or higher risk profiles before the conflict erupted. These should act as a cushion in the near term, if equity markets continue to trend down.

Within Alternatives, which overall can help diversify sources of income and return within portfolios, private markets were also downgraded from neutral to slight underweight, amid mounting concerns about private credit – especially when there is a liquidity mismatch such as in evergreen funds. Even though tactical rebalancing does not really apply to this market segment, (greater) cautiousness and selectivity is now warranted by favouring niche private markets and a robust manager selection, diversifying loan vintages and appropriately sizing allocations.

Bottom-line: cautiousness, diversification and quality are key when the storm hits. While we cannot direct the wind, we can adjust the sails. At the same time, history shows that attempts to “market time” geopolitical events often result in failure. Which is why we did not cut risk more aggressively (for the time being), and are also standing ready to reload exposure should a political or military solution fast restore oil and gas flows. Still, the path by which these flows through the Strait of Hormuz will be restored remains unclear, while further strikes on energy infrastructure would pose longer-term risks. To end on a positive note, periods of high volatility can also represent opportunities for investors looking to deploy cash, or attractive entry points… assuming some exaggerations. This may already be the case within the bond market, especially in the belly of the curve for high quality bonds, as inflation risks and hawkish central bank responses have now been well priced in. Less so within equity and credit, where complacency about growth prospects still dominates in our view.

Fabrizio Quirighetti, CIO & Head of Multi-Asset

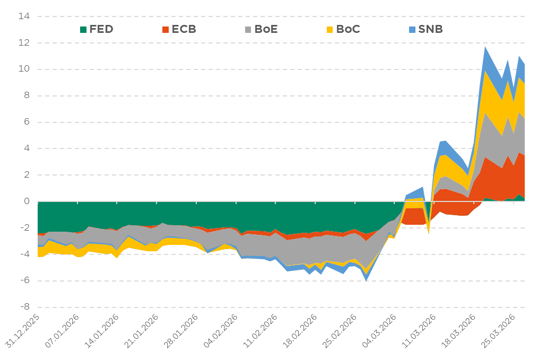

Expectations of rate cuts/hikes through year-end

External sources include: LSEG Datastream, Bloomberg, FactSet, Wisdomtree, International Energy Agency.