- Municipal waste comprises a significant share of recoverable materials

- Metal concentration is higher in urban vs. traditional mines – with also full national control

- Listed urban mining companies are still little known, but also stand to benefit from the AI era

What if cities, with their lucrative reserves of recycled materials, were to take precedence over primary mining? At a time when technological advances are causing demand for critical metals to skyrocket, recovering them from urban waste represents a promising path for the future – at the very heart of the circular economy principle.

Massive investments in AI data centres, the trend towards electrification and smart grids, as well the necessary energy transition in the face of climate and geopolitical challenges: all these developments are currently fuelling demand for critical metals.

Compared to traditional mining, investing in recycling delivers both faster results and much higher metal concentrations. Furthermore, improved recycling helps strengthen the resilience of supply chains – a priority for many governments in this post-pandemic and conflict-prone world.

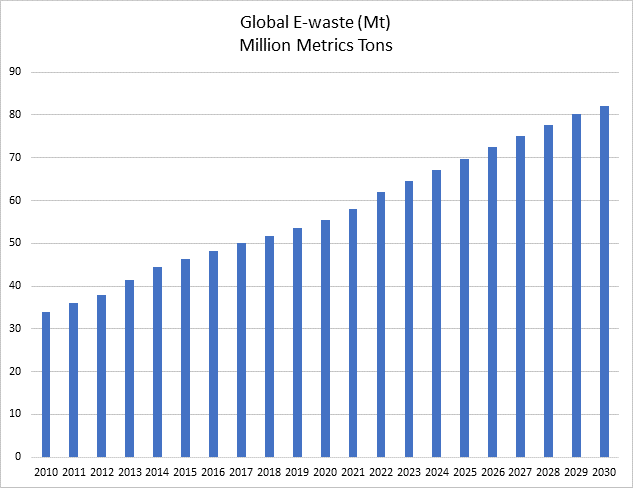

Here are some figures to illustrate our case. Within the 2.2 billion tonnes of municipal waste generated annually, the share of recoverable materials is significant (ca. 70% according to some estimates). Electronic waste alone amounts to some 60 million tonnes, a figure set to grow by 30% through 2030. With only 20% of such electronic waste currently being recycled, the value of “lost” resources – critical and precious metals – is estimated at over USD 60 billion per annum. Copper is a particularly telling example: its concentration in waste is 30 to 200 times higher than in primary mines.

From an investment standpoint, three segments appear particularly interesting. First, the aforementioned electronic waste, which includes smartphones, laptops, servers, telecommunications equipment and IT hardware used in data centres. Second, used batteries, whether from electric vehicles, energy storage systems or consumer products. And finally, industrial and infrastructure waste, such as electrical cables, motors and turbines.

When discussing AI deployment or the energy transition, the names that spring to mind are the stock market titans. Urban mining involves much lesser-known – but equally promising – companies. Sims Ltd, for instance, is currently the world’s largest listed recycler of metals and electronic equipment, with revenues projected to exceed USD 6 billion this year. Operating in 13 countries, but particularly dominant in North America, the company is active throughout the waste value chain: collection, recycling/recovery, refining and resale on secondary markets.

Befesa, a small cap listed on the Frankfurt Stock Exchange, illustrates a complementary business model. It specialises in the treatment and refining of waste generated by heavy industries, notably the steel and aluminium sectors. Active in the US since 2021, following the acquisition of American Zinc Recycling, Befesa has become a leader in the recycling of steel mill dust.

These are just two of many companies that, in our view, exemplify the benefits of a circular economy approach – and stand to be significant beneficiaries of the ongoing structural transitions in the technology and energy sectors.

Sandro Occhilupo, Head of Discretionary Portfolio Management

The global E-waste Monitor 2024 – Electronic Waste Rising Five Times Faster than Documented E-waste Recycling: UN

To infinity and Beyond?

- Hormuz off, Hormuz on…

- A diverging but resilient business cycle, moving closer again to a Goldilocks backdrop

- In this context, earnings growth and upward revisions should remain supportive

After 38 prior proclamations of an imminent deal with Iran, a Memorandum of Understanding (MoU) has finally been signed and oil prices have slipped back below USD 80 per barrel. For sure, a MoU is no final peace agreement. Plenty could go wrong in the next 60 days of negotiations. Still, if the US has indeed accepted the 14 draft conditions reportedly laid out by Iran, this deal reveals just how eager the White House was to secure some form of ceasefire before the G7 summit and ahead of the July 4th celebrations marking America’s 250th anniversary. The timing could hardly have been better for another close friend of the President… just one day prior to the launch of the intergalactic SpaceX rocket IPO.

Contrary to President Trump’s portrayal of events, Iran thus appears the clear winner. Fortunately for investors, markets care less about (geo)political narratives than about energy prices, inflation, economic growth and liquidity. Summer is here and the Strait of Hormuz should reopen soon. As we slip into the usual warm season lethargy, a refreshing macro rehydration break may be exactly what markets need. The reversal in energy prices should bring welcome (headline) inflation and rates relief, as well as improved growth prospects, especially in Europe and Asia.

To date, the macro backdrop has in fact remained broadly resilient, albeit increasingly uneven across regions and sectors. Growth is being supported by a handful of powerful engines, most notably AI-related capex, manufacturing activity, mining and infrastructure investments, which continue to offset pockets of weakness elsewhere. At the same time, inflation is proving stickier than initially expected, limiting the scope for policy easing and keeping monetary conditions moderately tighter than anticipated. Geographically, economic activity is also increasingly divergent. The US continues to deliver upside surprises, while the euro area lags with more frequent downward revisions, reflecting weaker domestic demand and softer services activity, even as manufacturing shows signs of stabilisation. In China, the recovery remains unbalanced, with domestic demand still subdued and growth increasingly reliant on strong exports. Against this backdrop, a key open question is whether Europe can re-accelerate, assuming energy prices remain contained (Brent below USD 80). We think “yes it can!”

While our central scenario remains unchanged, it must thus be acknowledged that the likelihood of an adverse scenario has decreased, in sync with the retreat in oil prices, bringing the global situation closer to a Goldilocks mix. The more interesting question is what happens next. Investors have been busy celebrating lower oil prices, but another risk has crept back onto the stage: a more hawkish Federal Reserve (Fed). Its latest communication was notable not for what was said, but for how little was said. Speak less, act more… The statement was shortened, simplified and concluded with a message that leaves little room for interpretation: „The Committee will deliver price stability.“

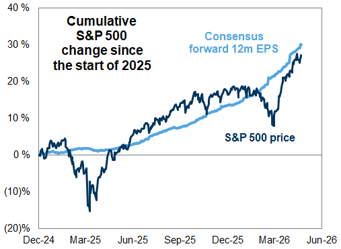

Taken literally, a Fed genuinely committed to returning inflation to 2% would require substantially higher rates (the Taylor Rule would imply ca. 5% Fed Funds nowadays). Reality, however, is rarely that simple. For the time being, bond yields appear to remain below the pain levels that would seriously challenge equity valuations or reignite concerns over government financing costs. Equally important, the market’s dominant narrative, AI-driven capital expenditure, remains intact. In this context, earnings growth and upward revisions should remain supportive.

As a result, we have tactically moved equities up to a neutral stance, reflecting a meaningful improvement in the overall risk-reward balance – with tail risks continuing to recede. The combination of lower oil prices, easing geopolitical tensions following the US-Iran MoU and more resilient global growth has materially reduced downside macro uncertainty. At the same time, earnings momentum remains solid and broadening, with positive revisions supporting an increasingly constructive medium-term growth outlook. Valuations have even cheapened somewhat in the US, especially within the IT sector/growth style. On the technical side, sentiment has normalised back to neutral despite recent highs, and market price momentum remains supportive, as indices hover near record levels with contained volatility and strong issuance absorption. Overall, the upgrade to neutral reflects a more balanced configuration where risks are no longer skewed decisively to the downside, but where selectivity remains essential given dispersion across regions, sectors and styles. Regionally, we have also upgraded Europe to a slight overweight as it certainly figures among the main beneficiaries of lower energy prices.

Elsewhere, the US dollar has been upgraded to a slight overweight, currently supported by resilient US growth, the AI “exceptionalism” boom and the Fed’s recent U-turn. Furthermore, Kevin Warsh appears as a very credible new Fed Chairman, while the greenback diversifier/risk-off hedge feature is regaining some appeal. Finally, and consistent with the prior decision and its rationale, we are also turning more cautious on gold (slight underweight), which now appears capped, especially after its strong run last year, and faces headwinds in the form of higher-for-longer rates and a stronger USD.

Fabrizio Quirighetti, CIO & Head of Multi-Asset

Impressive US earnings resilience

External sources include: LSEG Datastream, Bloomberg, FactSet, Goldman Sachs, Ewastemonitor.info.