Over the past few months, the macroeconomic narrative has shifted significantly. At the start of the year, investors broadly expected a gradual cooling of the US economy, a weakening labor market, and a continued disinflationary process as the effects of tariffs faded from annual comparisons. That scenario now looks increasingly outdated.

Recent US economic data have consistently surprised to the upside, culminating in another better-than-expected US job report. The US labor market remains remarkably resilient, with job creation continuing at a pace inconsistent with recession concerns. Government spending remains supportive, consumption has held up well, productive investment has accelerated thanks to the ongoing AI boom and fears of an imminent deterioration in economic activity have thus largely receded.

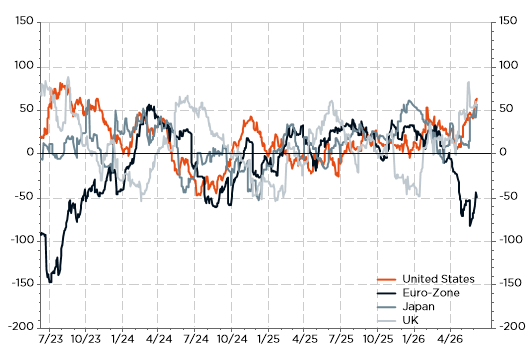

Citigroup Economic Surprises: US economy continues to defy gravity so far

Resilient global growth overall but with more dispersion depending on which economies benefit from the AI boom or suffer from higher energy prices

At the same time, the geopolitical backdrop has become more challenging. More than 100 days into the conflict involving Iran, there is still no credible path toward a lasting resolution. Most importantly for markets, there remains no clear prospect of a full normalization of traffic through the Strait of Hormuz. As a result, energy markets continue to incorporate a meaningful geopolitical risk premium, keeping upward pressure on global inflation expectations and driving also markets prices (negative correlation between stocks and oil, as well bonds and oil).

This combination of resilient growth and elevated energy uncertainty has materially altered the policy landscape. The Federal Reserve’s primary concern is no longer the possibility of labor market weakness. Instead, preserving purchasing power and preventing a renewed inflation cycle have moved back to the top of the agenda. In other words, the latest US job report has decisively shifted the balance of risks towards inflation concerns rather than a weakening labor market

Consequently, the disinflation process that many investors expected to continue throughout 2026 appears, at best, delayed by several months. While inflation may still moderate over time, the path is proving far less straightforward than anticipated at the beginning of the year. Markets, however, continue to price a relatively benign outcome. Risk assets remain well supported, thanks to strong earnings growth, and enthusiasm surrounding artificial intelligence has driven a new wave of speculative behavior, particularly within the technology sector. Valuations in several segments increasingly rely on the assumption that financing conditions will remain favorable and that policy rates will eventually move lower.

Yet investors should not underestimate the gravitational force of interest rates. Should the Federal Reserve determine that inflation risks warrant a tighter stance, higher rates would quickly challenge some of the excesses that have emerged across speculative corners of the market. The most obvious candidates would be the companies whose valuations have been propelled by AI-related euphoria rather than near-term cash-flow fundamentals.

This raises an increasingly relevant question for investors: if inflation remains stubborn and growth remains resilient, could the next Fed Chair be forced to remove the punch bowl rather than refill it? In less than ten days, all eyes will be on Kevin Warsh. Markets appear convinced that monetary policy will eventually become more accommodative. The risk, however, is that the next chapter of this cycle may require exactly the opposite.

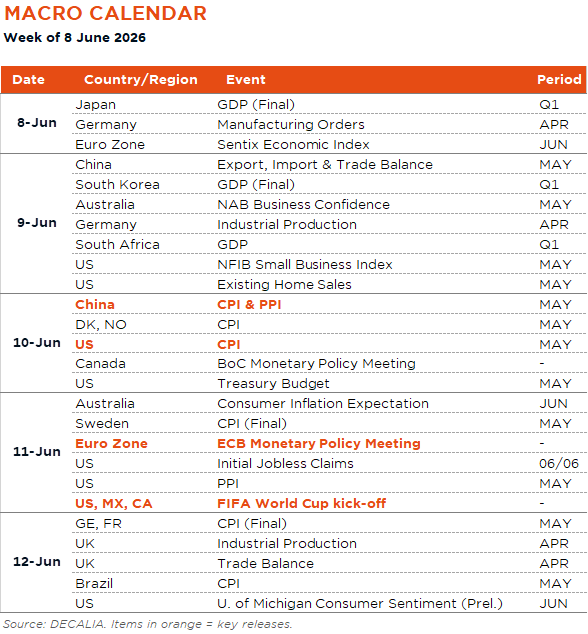

Economic Calendar

After the blowout US jobs report released last Friday (payrolls up +172k in May vs. 88k expected and a net upward revision of +93k over the previous two months), all eyes will be on US inflation next week, with May US CPI and PPI due on Wednesday and Thursday, respectively. They’ll be the last key data released ahead of the Fed’s next meeting on June 17 (the week after), which will be the first under the new Fed Chairman, Kevin Warsh. The consensus expects CPI to increase +0.5% MoM for headline (resulting to a 4.2% YoY rate in May vs. 3.8% in April) and +0.3% for core (+2.9% YoY vs. 2.8% the prior month). For the PPI, the annual rate is expected to exceed 6% for the headline and 5% for the core index. Upside surprises on these inflation figures would certainly not be welcomed by global markets. At the opposite, softer inflation figures will bring some reassuring balm to investors. Finally, other US economic data releases worth mentioning include the NFIB Small Business index (Tuesday) and the University of Michigan Consumer Sentiment (Friday), where consumer inflation expectations will certainly also be in focus…

Turning to Europe, several April indicators will give a snapshot of German economic activity including factory orders (Monday) and industrial production (Tuesday). There will also be May CPI reports for Denmark and Norway (Wednesday). But the other important event next week will be the ECB’s monetary policy meeting on Thursday, where a 25bps hike, lifting the deposit rate to 2.25%, is widely expected.

Before that, the decision from the Bank of Canada is due on Wednesday. The consensus points to a hold but there too the jobs market is getting suddenly hotter according to the latest data released this afternoon (unemployment rate unexpectedly declined to 6.6% form 6.9% with a net positive full-time employment change of +154k in May (-47k the prior month). So, likely a more hawkish hold than foreseen a few days ago.

In China, the focus will be on May trade balance (Tuesday) and, more importantly, the CPI and PPI reports on Wednesday. According to the consensus, economists expect China’s reflation to continue in May, with the PPI rising to 3.8% YoY from 2.8% and the CPI ticking up to 1.3% YoY from 1.2%. Elsewhere, the FIFA World Cup will kick-off on Thursday 11 June in Mexico (Mexico – South Africa, Group A). Many “small nation” teams will be competing in this prestigious tournament for the first time, while Italy will be sitting it out for the third time in a row… Finally, corporate earnings next week will include Oracle and Adobe, whereas the launch of Space X IPO has been set on Friday.

This is a marketing communication issued by DECALIA SA. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The information and data presented in this document are not to be considered as an offer or invitation to buy or sell any securities or financial instruments nor to subscribe to any services. The information, opinions, estimates, calculations etc. contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Investments in any securities or financial instruments may not be suitable for all recipients and may not be available in all countries. This document has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Before entering into any transaction, investors should consider the suitability of the transaction to individual circumstances and objectives. Any investment or trading or other decision should only be made by the client after a thorough reading of the relevant product term sheet, subscription agreement, information memorandum, prospectus or other offering document relating to the issue of the securities or other financial instruments. Where a document makes reference to a specific research report, the document should not be read in isolation without consulting the full research report, which may be provided upon request.