And here we go again for a new Italian Serie A championship with my favorite team, Cagliari Calcio, which kicked off with a good performance and a 1-1 draw at home against Fiorentina last night. If the championship ended there, Cagliari would be safe from relegation – which would be more than enough to make me happy – unlike Lazio and AC Milan, who stumbled on the first day. Of course, even though things are off to a good start, it’s far too early to jump to conclusions… In my humble opinion, investors also got ahead of themselves following Jay Powell’s speech last Friday in Jackson Hole. Admittedly, the tone was dovish, but there are still a few obstacles in the form of important economic data releases before the next Fed’s meeting on September 17th. In this context, Yogi Berra’s immortal and wise words ring true: “the game’s not over ‘til it’s over”.

For sure, Powell gave the markets (and to a lesser extent Trump) what they wanted in the form of a dovish tilt in his Jackson Hole speech. Basically, after he talked about inflation risks, a few sentences later he indicated they would make a rate cut, “…with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance”, which was what the market wanted to hear. Note that Powell did not commit to a specific date, but everybody understood -between the lines- that it would happen as soon as the next Fed’s meeting. As a result, market pricing of a Fed rate cut next month rose from 72% Friday morning to 86% this morning, while five cuts totaling 125bps, to a 3% to 3.25% range are still priced in by next year (September 2026).

The reason? Employment risks are increasing… “Overall, while the labor market appears to be in balance, it is a curious kind of balance that results from a marked slowing in both the supply of and demand for workers. This unusual situation suggests that downside risks to employment are rising. And if those risks materialize, they can do so quickly in the form of sharply higher layoffs and rising unemployment”. Personally, I am glad to see that we came to the same conclusions regarding the slowing in both the labor supply and demand and thus the unusual and thus fragile current balance.

What could go wrong in the next few weeks or months for investors? The story remains basically unchanged to a large extent: either growth peters out faster and deeper than expected and the Fed appears finally to be behind the curve; or inflation comes back in the forefront as a major issue, impeding the Fed to ease preemptively in the next few months. In the meantime, a third endogenous risk is emerging: investors overconfidence in the soft-landing narrative (or ongoing Goldilocks scenario), which is pushing assets valuation to extreme levels. Indeed, investors are certainly getting little ahead of themselves by considering for granted a rate cut in September. First, US August job report (released on Friday 5th September) as well as August PPI and CPI (10th and 11th September) may shift again the balance of risks before the next Fed’s decision. Then, the next few months will give tough year-over-year comparisons for inflation figures, even before considering some potential tariff effects. Should investors and will the Fed really look through those as totally transitory? Third, the real debate about how many rate cuts and how fast they will occur remains very open, in my view. On this key topic, there weren’t any major insights from Powell, who remained wisely vague by stressing that monetary policy “was not on a preset course”, adding “we cannot say for certain where rates will settle out over the longer run, but their neutral level may now be higher”.

So, we can’t rule out some form of “hawkish cuts” going forward. Last but not the least, a “too dovish” Fed may also lead to financial assets bubbles, on top of a much weaker dollar and a sharp increase in US long term rates -especially when coupled with the current accommodative fiscal policy- that will have undesired “too much of a good thing” ripple effects on the economy or inflation. In this context, the Fed may be forced to take away the punch bowl… too late and thus definitively.

Like sport’s fans, investors saw and heard what they wanted to last Friday, but beware of counting your chickens before they hatch as disappointment risks now loom bigger than ever.

Economic calendar

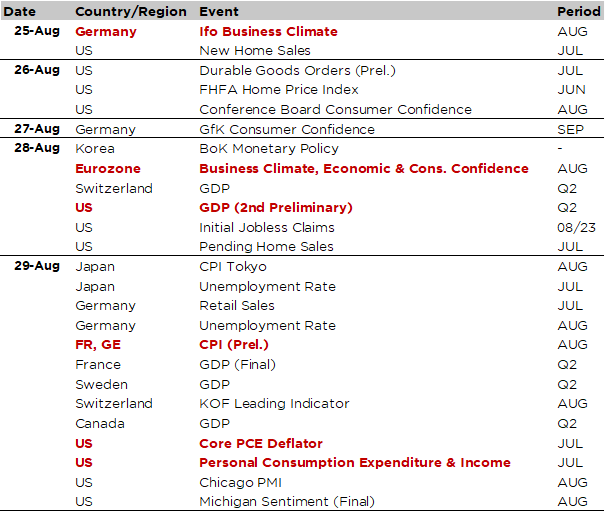

While we wait for the first week of September and the numerous key macroeconomic data releases scheduled for that time (Global PMIs, US ISM indices, US job report), there will still be some interesting figures to follow and analyze this week.

For once, let’s start with Europe, with the IFO index today, business climate and economic confidence on Wednesday, and preliminary inflation figures for August in Germany, Italy and France on Friday. These data could reinforce investors’ favorable sentiment towards the eurozone if (1) they confirm an improvement in growth prospects, particularly in Germany (see the preliminary PMIs published last week, which are generally slightly better than expected) and (2) allow the ECB to maintain an accommodative bias, or at least the option to cut rates if necessary, in the event that preliminary August CPIs are in line with or below expectations (the consensus points to 2.1% yoy in Germany, 1.8% in Italy and 1.0% in France, whereas the overall Eurozone August flash CPI is due next week).

Note also that the negative revision to German Q2 GDP last Friday, which finally shrank by -0.3% instead of -0.1% previously released, was widely expected due to a drop in industrial production in June, likely related to a (temporary) pull-back after the surge in German production/exports before the US tariffs come into force. Moreover, it is already “old” story vs. the more recent improvement in preliminary July German PMI.

Speaking about Q2 GDP, we will also get the figures from both Switzerland (Thursday, +0.1% expected after +0.5% in Q1) and Sweden (Friday). In the United States, the second estimate of Q2 GDP growth (Thursday) may or may not highlight a sharper slowdown in domestic consumption/demand, as well as showing some adjustments to the extraordinary contributions from net exports and inventories seen in the 1st estimate (due to the distortions caused by tariffs). However, the big piece of news will undoubtedly be the consumer price deflator (PCE deflator) that will be released on Friday along with the personal consumption and disposable income for July. The consensus expects core PCE rising again +0.3% MoM in July after +0.3% in June, which would push the YoY % change to +2.9% from +2.8%. It also foresees resilient consumption (+0.3% in real terms) and income (+0.5%), both accelerating somewhat compared to the previous month. While not decisive, these figures could influence the Fed’s next decision in September and therefore significantly alter the probabilities in the event of major surprises.

Before that, other notable US economic data releases include new home sales (today), the Conference Board’s consumer confidence survey and durable goods new orders (both Tuesday) and weekly jobless claims (Thursday).

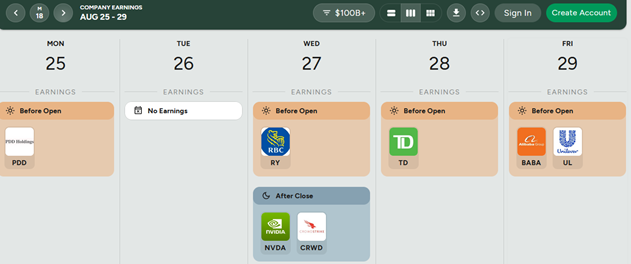

Finally, in terms of corporate results, there will also be a major event… with Nvidia’s publication after the US market closes on Wednesday evening, while we will get Alibaba results on Friday.

Non-exhaustive list of major earnings releases over the week (market cap > $100bn)

Source: https://earningshub.com/earnings-calendar/week-of/2025-08-25

This is a marketing communication issued by DECALIA SA. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The information and data presented in this document are not to be considered as an offer or invitation to buy or sell any securities or financial instruments nor to subscribe to any services. The information, opinions, estimates, calculations etc. contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Investments in any securities or financial instruments may not be suitable for all recipients and may not be available in all countries. This document has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Before entering into any transaction, investors should consider the suitability of the transaction to individual circumstances and objectives. Any investment or trading or other decision should only be made by the client after a thorough reading of the relevant product term sheet, subscription agreement, information memorandum, prospectus or other offering document relating to the issue of the securities or other financial instruments. Where a document makes reference to a specific research report, the document should not be read in isolation without consulting the full research report, which may be provided upon request.