Sport has a habit of reminding us that trends can reverse when everyone least expects it. This past week delivered another reminder. On one side, the ultimate “remontada”: the New York Knicks clawing their way back from the brink, ultimately ending a 53-year title drought and reminding investors, once again, that no lead is ever truly safe. On the other side, the “derrumbe”, the spectacular collapse. Think Curaçao’s humbling 1-7 defeat against Germany yesterday evening in the FIFA worldcup game, or the financial equivalent of « Bob the Builder », i.e. Robert “Bob” Bull: always confident he can fix it, until the foundations suddenly reveal a few inconvenient cracks.

The question for markets this morning is simple: are we witnessing another remontada, or merely setting the stage for the next derrumbe? After more than 100 days of conflict, false dawns and escalating tensions, markets finally received what they had been waiting for: a peace agreement between the United States and Iran. According to the memorandum of understanding announced overnight, the deal includes a phased lifting of US sanctions on Iranian oil exports, the unfreezing of approximately $12bn of overseas assets and, crucially, the reopening of the Strait of Hormuz within the next 30 days, subject to mine-clearing operations. A broader 60-day negotiation process is expected to follow, notably regarding Iran’s nuclear program.

For markets, the immediate reaction appears straightforward. A reopening of the Strait of Hormuz should support a further risk-asset remontada. Energy prices are likely to continue retracing, sovereign bond yields may ease, credit spreads could tighten further and the US dollar may surrender some of its recent gains. Gold, which suffered from rising yield and a stronger US dollar recently, could also regain some of its shine in the near term.

In other words, financial conditions are becoming more accommodative almost automatically. The problem is that markets may once again be focusing on the headline while ignoring the sequel. President Trump suggested last week that inflation would fall « like a rock » once the Iran war was over. Certainly, headline inflation should move lower in coming months. Oil prices have already retreated significantly from their peak above $110 per barrel earlier this year, and a fully operational Strait of Hormuz would eventually allow additional crude supplies to reach global refineries.

Yet the key word here is « eventually ». The Strait is not fully reopened yet. Operational normalization will take time. More importantly, even if energy prices continue to decline, what happens to core inflation? This is where the story becomes more complicated.

What if the real consequence of peace is not disinflation but rather a growth reacceleration? Lower yields, tighter credit spreads, a weaker dollar and improved investor sentiment would effectively loosen financial conditions. Europe and Asia, both constrained by the recent energy shock, could see economic activity rebound. The US consumer, whose purchasing power had been squeezed by higher fuel costs, may also regain confidence. And with the Iranian front potentially moving towards closure, Washington could once again redirect its attention towards trade policy and tariffs.

We have seen this movie before. Remember how inflation was initially dismissed as « transitory » after Covid because it appeared concentrated in durable goods? Once economies reopened, price pressures migrated into services and became far more persistent than policymakers anticipated. Could a similar dynamic emerge again?

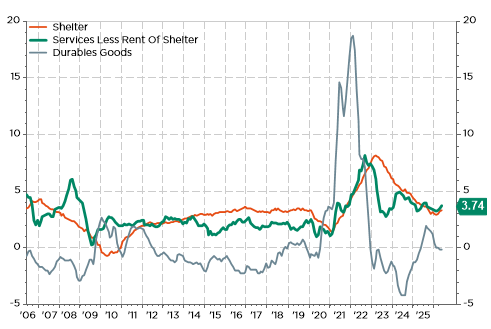

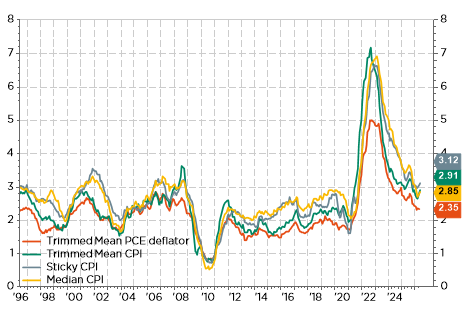

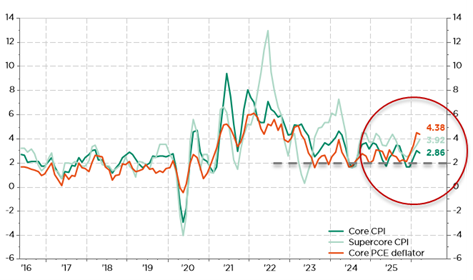

Anyway, the Federal Reserve has very little room for error. Despite the expected moderation in headline inflation, the « services less rent of shelter » component remains well above levels consistent with the Fed’s 2% objective. Several alternative and arguably more robust inflation measures tell a similar story. Moreover, core CPI, supercore inflation and core PCE have all shown signs of re-accelerating over the past three months.

See graph below.

Selected US inflation components: “services less rent of shelter” prices still flying high…

… as well as alternative inflation gauges, which remain above 2%

Q/Q% annualized rate in core inflation, supercore & core PCE

Add an US labor market that remains remarkably resilient and it becomes legitimate to ask whether unleashing animal spirits at this stage would truly help the disinflation process. One could thus even argue the opposite. Easier financial conditions, stronger growth and renewed risk-taking may end up delaying the very disinflation required to justify future Fed rate cuts. They could also fuel some of the speculative excesses that are already visible across parts of financial markets.

Which brings us back to our original question. For investors, the peace deal may indeed trigger a near-term remontada in risk assets. For inflation, however, the story may prove far less straightforward. And for the Federal Reserve, the ultimate question remains unanswered: Mr. Warsh and colleagues, what comes next for policy rates? Fed’s target rate « Remontada » or « Derrumbe »?

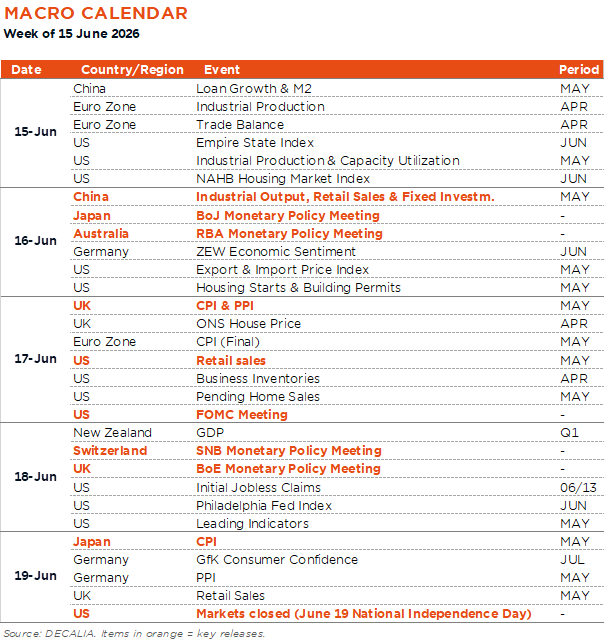

Economic calendar

Who is hiking next? Central bankers will be in the driving seat this week, with meetings, subsequent statements and decisions due from the BoJ (Tuesday), RBA (Tuesday), the Fed (Wednesday), the BoE (Thursday) and the SNB (Thursday). In terms of economic data releases, we will also get some important CPI prints in the UK (Wednesday, ahead of the BoE meeting) and Japan (Friday after BoJ meeting), and several economic activity indicators in the US and China. Last but not least, and closer to us, the G7 leaders’ summit in Evian will take place over the next few days (15-17 June, with manifestations and thus potential uprisings in Geneva already this week-end).

The main event next week will be the FOMC meeting on Wednesday evening, the first one under the new Fed Chair Kevin Warsh. Beyond the target rate decision, widely expected to be kept on hold at 3.5%-3.75%, the focus will be on how the committee (and his new Chairman) perceive inflation risks now, with the updated economic projections (SEP) and the dot plot amongst the key inputs for that. It could be tricky and bumpy as the Fed should likely turn from a dovish hold to a hawkish hold as inflation pressures are building -even if they may recede later this year but no evidence yet-, and the labor market has clearly not deteriorated further in the last few months and even improved compared to the end of last year. For the time being, easing wage pressure limit any risk of second round effects on inflation from the rise in energy prices. However, the later has also started to feed into core inflation: core services inflation shows signs of bottoming out, while other core inflation gauges have accelerated again well above 3% on a 3M percent change annualized rate. These rising inflation concerns have been already priced in by markets, which currently foresee a full 25bp of hikes by the end of the year. Most interesting maybe, with a new Fed Chair in place, the press conference may shed some light on some changes to communication going forward, possibly looking to phase out forward guidance and the dot plot, argue for a further reduction in Fed’s balance sheet or scale back on the number of press conferences…

Elsewhere, central bank meetings will also include the BoJ and RBA decisions on Tuesday, where the consensus expects a 25bps rate hike to 1.00% for the former, and no change for the later (hawkish hold at 4.35% with further increases ahead still possible), and the BoE and SNB on Tuesday. Saved by the latest UK CPI report, which showed a larger-than-expected fall in inflation in April, the BoE should keep rates steady at 3.75%… unless a big upside surprise in the May CPI report, which will be released the day before, shakes things up. Again. As far as the Swiss National Bank is concerned, it is now in a comfortable wait and see situation as its next move depends on the other major central banks, whereas the Swiss Franc isn’t appreciating anymore against key economic partners currencies. Note that the Swedish Riksbank and Norges Bank will also meet on Wednesday and Thursday, respectively. Turning to economic data, China activity indicators for May are due Tuesday. The consensus expects a modest improvement from an overall ongoing subdued growth with industrial production up around 4-5%, supported essentially by buoyant exports, while domestic demand and retail sales remain stagnant on a YoY basis. In the US, we will get May industrial production (Monday), retail sales (Wednesday), where more of the same resilient growth is expected, as well as several housing indicators over the week. Note that US markets will be closed on Friday (Juneteenth National Independence Day). In Japan, the highlight will be the May CPI report (Friday) with no major changes expected.

This is a marketing communication issued by DECALIA SA. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The information and data presented in this document are not to be considered as an offer or invitation to buy or sell any securities or financial instruments nor to subscribe to any services. The information, opinions, estimates, calculations etc. contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Investments in any securities or financial instruments may not be suitable for all recipients and may not be available in all countries. This document has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Before entering into any transaction, investors should consider the suitability of the transaction to individual circumstances and objectives. Any investment or trading or other decision should only be made by the client after a thorough reading of the relevant product term sheet, subscription agreement, information memorandum, prospectus or other offering document relating to the issue of the securities or other financial instruments. Where a document makes reference to a specific research report, the document should not be read in isolation without consulting the full research report, which may be provided upon request.