Apocalypse Not Now! We’ve avoided the worst in two ways—at least for now! First, because even though this weekend’s negotiations came to nothing, other than an even stricter U.S. blockade of the Strait of Hormuz aimed at economically suffocating Iran, we’ve at least avoided the immediate destruction of a civilization… Second, because Cagliari won a crucial match for its survival in Serie A (a 1-0 victory over Cremonese). In both cases, relief is certainly warranted, even though we’re not completely out of the woods yet, since we can’t assume that victory depends solely on the possibility that our opponents will collapse.

Anyway, the odds of a short and sharp conflict with the price of Brent returning to pre-conflict level by mid-year have evaporated as it has been six weeks already since the Strait of Hormuz, where circa 20% of global oil and LNG transits (on top of fertilizers and other goods), has been blocked. So, the best case now remains that the disruption does not extend beyond spring, with oil prices remaining around current level of $100/bbl before retracing in the second part of the year. Near term risk involves a squeeze in oil prices above $120/bbl and potentially a spike much higher (>$150/bbl) if further infrastructures are hit and/or boots land on the ground.

For the time being, in the absence of any better geopolitical insights than the consensus, we stick with our core view that we will avoid a recession (i.e. we expect a gradual, bump, muddling through de-escalation). However, sustained higher energy prices will neutralize the tailwinds from OBBBA related stimulus in the US and from the German fiscal boost in Europe, while putting some more fragile economies at risk (India and Turkey for example), on top of exacerbating political tensions, worsening public deficits trajectories and impeding a proper monetary policy medicine (not suited for supply shock). If you also consider the current positive correlation between bonds and equities returns with few safe havens, some cautiousness is still warranted, either by reducing somewhat equity and other risk-on assets exposure, or by adding tactical hedges when opportunities arise. In sports, as in war, it will be foolish to celebrate before the game is over. And to paraphrase Yogi Berra: it ain’t over til the blockade isn’t over.

In the meantime, here are a few “real-time” financial indicators to watch in order to assess if markets start to be more concerned about growth (than inflation):

- Bonds-equities correlation revert to negative if growth fears start dominating (with equities down and bonds up)

- Defensive equities outperforming cyclicals. In the same vein, cyclical currencies underperforming defensive ones (AUD losing ground against CHF for example)

- Credit spreads widening (much) further

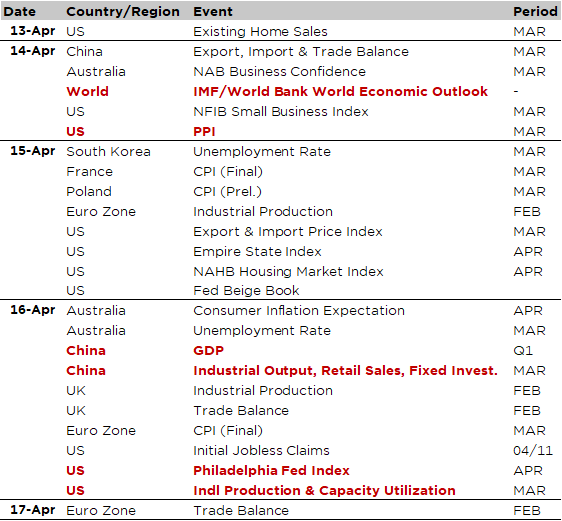

Economic Calendar

Considering the “known” macro agenda, the main event will be the IMF/World Bank Spring meetings through the week, which include several central bankers’ speeches (such as BoJ Governor Ueda, ECB President Lagarde or BoE Governor Bailey) as well as the release of the latest World Economic Outlook on Tuesday. It will be key to hear about policymakers’ thoughts on the impact of the conflict in Iran, and see how the IMF/World Bank economic forecasts have changed/evolved due to the conflict in Iran.

As far as “pure” economic data are concerned, we will get the March PPI (Tuesday) and industrial production (Thursday) among the main highlights from the US. Some interesting surveys to assess the current business mood will also be released: the NFIB Small Business Index (Tuesday), the NAHB Housing Market Index (Wednesday) or the Philadelphia Fed manufacturing index for April (Thursday). Moving to China, the Q1 GDP and March economic activity data (industrial output, retail sales and investment) will be out on Thursday. More of the same is expected, i.e. decent growth overall -around officials GDP real growth target of 4.5%- supported essentially by strong exports. While China is relatively well insulated from this energy supply shock, thanks to its energy self-reliance barbell of coal & green energy, it may be hurt if this energy crisis leads to a global economic slowdown.

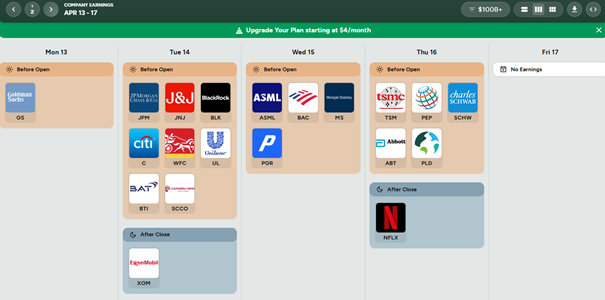

Finally, the focus will also be on the start of the Q1 earnings season, with reports due from several US financials (GS, JPM, C, BAC, MS), but also TSMC, ASML, Netflix in the Tech/Communication Services sectors, and other more traditional (read “old economy”) companies such as J&J, Pepsi, Unilever, BAT or Exxon. Overall, earnings growth is expected to be close to 20%, a four-year high, on the back of a broadening across sectors (even if it is still led by mega-cap tech companies), but with the corollary that the potential beat should be thus modest (given the higher expectations this time).

https://earningshub.com/earnings-calendar/week-of/2026-04-13

This is a marketing communication issued by DECALIA SA. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The information and data presented in this document are not to be considered as an offer or invitation to buy or sell any securities or financial instruments nor to subscribe to any services. The information, opinions, estimates, calculations etc. contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Investments in any securities or financial instruments may not be suitable for all recipients and may not be available in all countries. This document has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Before entering into any transaction, investors should consider the suitability of the transaction to individual circumstances and objectives. Any investment or trading or other decision should only be made by the client after a thorough reading of the relevant product term sheet, subscription agreement, information memorandum, prospectus or other offering document relating to the issue of the securities or other financial instruments. Where a document makes reference to a specific research report, the document should not be read in isolation without consulting the full research report, which may be provided upon request.