Surprises, surprises seem the norm nowadays. After 10 days of vacation, I found once again everything turned upside down when I got back to the office last week as we now find ourselves in the middle of the Iranian conflict. For better or for worse, the surprises extend to sports with Italy’s victory over England in rugby ?! Or Cagliari’s humiliating 1-3 loss to Pisa (which is all but relegated), despite playing one half with 11 against 10… Anyway, “what’s next?” remains the unchallenged key question for investors. While I am not a geopolitics expert, I will just explore some scenarios in the fog of confusion surrounding the Iran conflict and try to see where are the risks… as well as opportunities because we all too often tend to forgot (as we are busy managing the risks in these circumstances) that in the midst of every crisis, lies great opportunity too.

Investors remain obviously (and rightly) concerned about further escalation, and with each passing day they move to price in a more protracted conflict, especially as there’s been no sign of the two sides moving towards negotiations. So, the current rhetoric is only adding to the fears about an extended conflict and a sustained period of high oil prices. And when it comes to oil prices, all eyes are still on the Strait of Hormuz, and when that will begin to reopen. Financial markets have to reflect whatever impact exists from whatever does happen with oil prices over this period of time, and also the uncertainty over what is happening and how it will all transpire – hence the volatility. In other words, bad news gets priced in, then responded to; uncertainty just leaves us in exacerbated volatility.

If we can open it (the Strait of Hormuz), the oil price will likely come back down fairly quickly, the mood will change as the impacts of this war on inflation, growth and monetary policy will be contained in magnitude and time. Basically, we will return to the previous central supportive macro backdrop of supportive growth, disinflation -even if less rapid and bumpier than previously expected- and gradual monetary policy easing.

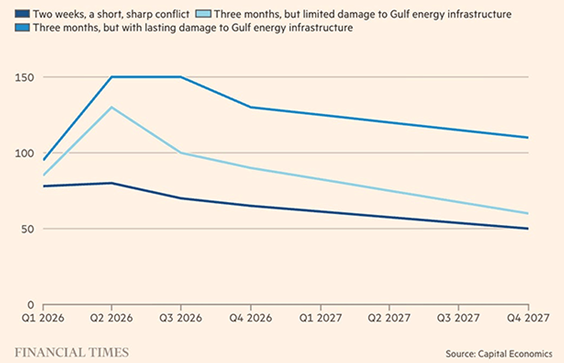

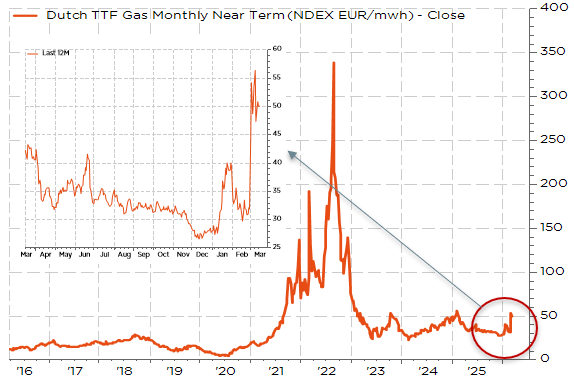

At the opposite of the scenarios’ spectrum, a conflict lasting more than a few weeks, but with longer-lasting damage to capacity, notably to Iran’s Kharg Island. In a recent paper, Capital Economics estimates there could be a loss of close to 10% of world exports of oil and LNG, with an impact into 2027. Oil prices could hit $150 a barrel and prices of gas in the EU (per megawatt hour) could hit €120. In this scenario, we will have a global supply shock quite similar to the one experienced from late-1970s to the mid-1980s.

Scenarios for Brent crude oil ($ per barrel): the most disruptive ones could have a large and prolonged effects on energy prices

Source: Financial Times, Capital Economics

However, mind the differences too with the 70-80’s stagflation: food prices were already climbing double-digits in mid-70’s, President Nixon exacerbated the price shocks with wage and price controls and had little control on oil embargo from OPEC (Iran conflict is in the hands of Trump to a large extent), America is now a net oil exporter, DM economies are now less dependent on oil (on the back of more efficiencies as well as alternative energy development) even if Europe and Asia remain net energy importer and will thus be more affected by an oil’s shock.

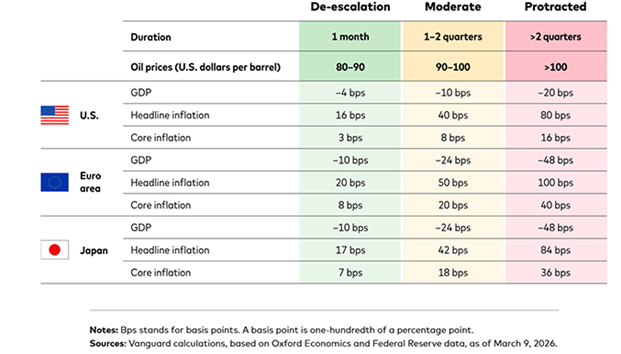

In this regard, Vanguard published an interesting report last week, giving you some idea of the impact on GDP and inflation for each region: the US does indeed relatively much better than Europe and Japan. This analysis also suggests that although the US (and global) economy remains resilient, the scale and persistence of energy disruptions raise noteworthy risks for growth, inflation, and central bank decision making… as expected.

Europe and Japan more vulnerable than US to protracted high oil prices

Source: Vanguard

Hopefully, the recent shock started from a much lower base and remains far smaller than the jump experienced in the immediate aftermath of Russia’s invasion of Ukraine. The release of barrels of oil from national reserves will help a little, but it only buys a few weeks.

European Gas price (futures contract, €/mwh): mind the step !

So, higher energy prices basically mean more inflation almost immediately, but often in a transitory way due to the base effects, while they slow economic activity with a delay -especially if high energy prices persist and monetary policies, but above all financial conditions, become tighter. As a result, this war and its subsequent consequences on (energy) inflation complicate central bankers’ life. Especially at a time, when US unemployment is getting softer, while energy price increases act as a tax increase (i.e. they generally reduce GDP)… but without the government receiving any proceeds of this “tax” (while still incurring the costs of war) at a time when government deficits are less and less “under control”.

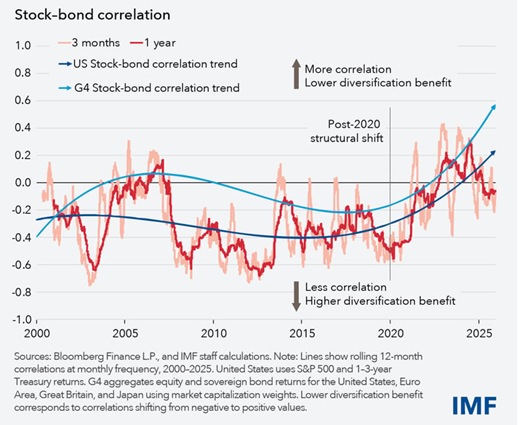

So, this stagflation-like scenario raises another important issue as it will not bode well for government debt, fiat currencies and eventually… inflation down on the road for the currencies suffering from debasement (with risks increasing when external deficits are elevated). The UK seems the most obvious example nowadays if you just look at the currency and rates volatility over the last few days or years. It also explains why (long term) government bonds haven’t acted as safe-haven. On this topic, it’s worth mentioning a recent NBER paper research “Are government bonds safe in times of war and pandemics?”, which was released with a great timing the prior month. The answer to the question posed in the title is “No, of course”. Another publication worth mentioning is the IMF’s note analyzing the stock-bond diversification: as we have repeated many times ourselves in this column, “diversification has become harder since 2020 as stocks and bonds tend to move in tandem during sharp selloffs”, posing a major issue for portfolio construction, while also adding to financial stability concerns.

Stock-Bond Diversification Offers Less Protection From Market Selloffs

Source: IMF

To conclude on a positive note, there are also investment opportunities, especially for those starting with a blank sheet or very light exposure in financial markets. Obviously, the rewards, timing and sizing depend on the endgame issue of this conflict, your starting allocation point and your risk profile, but here are a few assets I will consider almost independently of what comes next:

- Gold as it likely remains the best safe-haven asset in various risk-off scenarios (but I will be now less rosy on goldminers as they may suffer from “higher energy prices for longer”)

- High quality bonds with contained duration risks (i.e. 3-5y IG corporate bonds) as I don’t think that an oil supply shock really warrant central banks hikes

- Adding to some IT-software stocks (revival story), especially for those who are underweight

- Or, for the bravest, grab (selectively and patiently) some non-US assets.

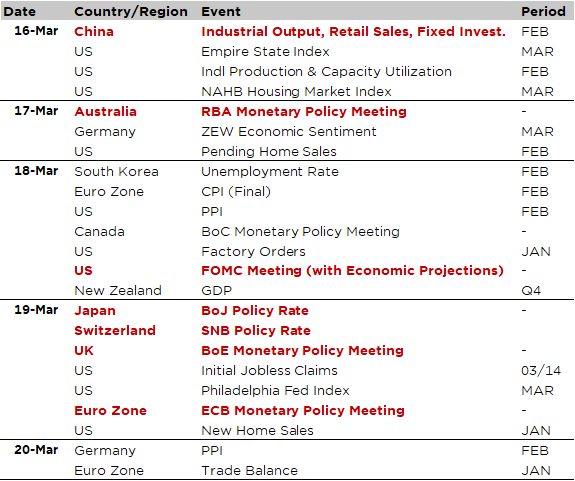

Economic Calendar

On top of the ongoing developments in Iran, its surrounding neighbors and the subsequent energy prices trajectory, monetary policy will clearly be the dominating theme of the week as all the key central banks will have a meeting and set their target rates. More importantly, investors will scrutinize closely policymakers’ wordings and thinking about the impact of the conflict in Iran on the monetary policy path going forward. The spotlight will be primarily on the Fed (Wednesday), especially as it will release its updated Summary of Economic Projections (SEP) and its famous dot plot. It will be followed then by the ECB, the BoE and the BoJ on Thursday. None of these central banks is expected to cut (or hike) rates, but the odds of a hike from BoJ aren’t nil, especially given the JPY weakness.

Other central banks making decisions next week include the RBA (Tuesday), where a 25bps hike to 4.10% is foreseen, the BoC (Wednesday), the Riksbank and the SNB (Thursday), which should all leave their rates unchanged at 2.25%, 1.75% and 0% respectively.

As far as economic data are concerned, the few notable ones that will be released are Chinese activity data for February this morning (industrial production, retail sales and fixed investment), which suggested that growth accelerated at the start of the year, driven by both strong exports and a pickup in domestic demand, and the US February industrial production this afternoon, the German ZEW survey for March on Tuesday, US February PPI on Wednesday and the US weekly jobless claims on Thursday. Both the March Empire and Philadelphia Fed manufacturing indices will also be published over the week, which will enable us to update our ISM manufacturing index model.

Finally, we will also get the earnings of FedEx, Tencent and Alibaba.

This is a marketing communication issued by DECALIA SA. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The information and data presented in this document are not to be considered as an offer or invitation to buy or sell any securities or financial instruments nor to subscribe to any services. The information, opinions, estimates, calculations etc. contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Investments in any securities or financial instruments may not be suitable for all recipients and may not be available in all countries. This document has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Before entering into any transaction, investors should consider the suitability of the transaction to individual circumstances and objectives. Any investment or trading or other decision should only be made by the client after a thorough reading of the relevant product term sheet, subscription agreement, information memorandum, prospectus or other offering document relating to the issue of the securities or other financial instruments. Where a document makes reference to a specific research report, the document should not be read in isolation without consulting the full research report, which may be provided upon request.