No miracle for the Nati (Swiss soccer team’s nickname). Once again, the football gods smiled on Lionel Messi and his teammates, while Switzerland left the World Cup with the familiar cocktail of pride, frustration and the nagging feeling that perhaps the better team hadn’t necessarily won.

Investors know also this feeling. So far this year, one of the most frustrating trades has not been missing AI altogether. It has been owning the wrong side of it. Many investors had assumed the biggest winners would be the companies building artificial intelligence. Instead, the market rewarded those getting paid for the spending. Memory manufacturers, networking equipment providers and AI infrastructure suppliers have largely outperformed the hyperscalers themselves. For now, it seems selling shovels remains a better business than digging for gold.

Like Robert De Niro standing in front of the mirror in Taxi Driver exactly fifty years ago, frustrated investors can only mutter: « Token to me? » Because that single word may become one of the most important concepts for investors over the coming years. A token is simply the basic unit an AI model reads or generates. Roughly speaking, one token corresponds to three-quarters of a word. Every question you ask ChatGPT, every answer it produces, every image generated and every software agent executed consumes tokens.

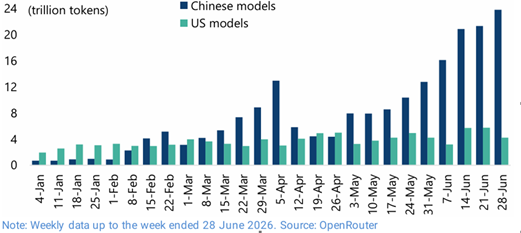

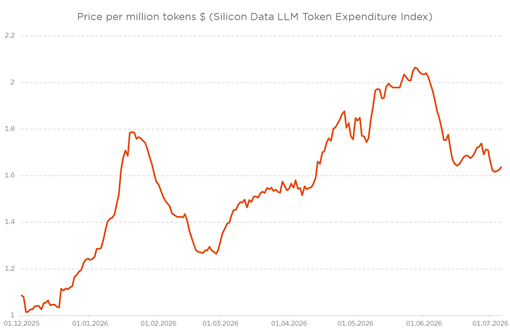

In other words, tokens have quietly become the new fuel of the digital economy. The good news, at least for investors and companies related to this trade, is that tokens’ demand is exploding. The less obvious news is that token prices are collapsing as price-sensitive companies/individuals are moving to “cheaper” models, often offered by Chinese companies, powered also by “less” costly Chinese tokens. Last week alone, several leading AI developers unveiled increasingly capable models. Their most impressive feature was arguably not intelligence, but affordability. Inference costs continue to fall at an astonishing pace as competition intensifies and models become more efficient.

Weekly usage of top 9 AI models across OpenRouter

Source: Jefferies

While that may be seen as a great news for users (if you don’t mind sending/sharing your data to China), it is potentially more complicated for investors. History suggests that when technology becomes abundant, prices tend to converge towards commodity levels. We have seen the same story play out repeatedly: memory chips, telecom bandwidth, solar panels, cloud computing. Artificial intelligence may not be immune. The obvious question therefore becomes: if the cost of this plentiful “artificial intelligence” keeps falling, who will actually make money?

Price per million tokens in $

So far, hyperscalers have justified extraordinary capital expenditure through their cloud businesses, where AI remains an attractive value-added service. But investors are increasingly asking a more uncomfortable question. What happens when hundreds of billions invested in AI infrastructure need to generate returns beyond simply attracting more cloud customers? For the moment, the maths still works. Although token prices are falling rapidly, usage is growing exponentially faster. Lower prices stimulate demand, more applications are built, more queries are processed and overall revenues continue to expand. So far, volume is comfortably offsetting price. Until it doesn’t.

At some stage, pricing may evolve towards subscription tiers or flat-rate models as providers seek to protect margins while encouraging ever-greater usage. Equally, hyperscalers may eventually decide that the era of seemingly unlimited AI capital expenditure has run its course. That is probably not tomorrow. But neither is it a risk investors can afford to ignore. Markets have spent the past eighteen months rewarding companies that enable AI investment. The next phase may prove far more selective, rewarding those capable of monetizing it. After all, building the smartest model is one thing. Building the most profitable business around it is something entirely different. As every disappointed Swiss supporter knows, dominating possession doesn’t necessarily win football matches. And in artificial intelligence, generating the most tokens may not ultimately generate the most profits. These dark clouds may simply be… a token of the approaching storm.

Economic Calendar

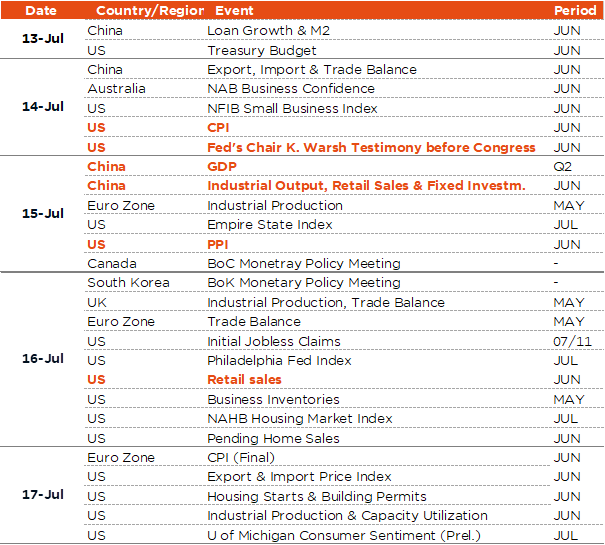

Inflation will be center stage this week for investors, with the US June CPI due on Tuesday, followed by the PPI on Wednesday. The consensus expects consumer prices declining by -0.1% MoM (+0.5% in May) but the core gauge is expected to increase by +0.2% like the prior month. As a result, the annual inflation rate should decrease to 3.8% in June from 4.2% in May, while the core index may tick down to 2.8% from 2.9%. A negative surprise (i.e. higher than expected increase on on the core / services inflation) may trigger further upward pressures on rates with potential ripple effects on equity market, forex and gold. An unfortunate coincidence eventually for the new Fed Chair Kevin Warsh, who will deliver his first testimony on monetary policy before Congress on the same date (Tuesday July 14) just after this release… Alternatively, a downside surprise may lead to a relief and a more favorable backdrop for both K. Warsh’s testimony as well as most financial assets, excl. the greenback obviously as it may help dampen rate hikes expectations.

As far as the PPI is concerned, economists foresee -0.1% MoM for the headline and +0.4% for core. Another read on inflation will also come from the consumer inflation expectations embedded in the University of Michigan consumer sentiment survey (Friday). Other US economic releases include the NFIB Small Business Optimism Index (Monday), the first regional manufacturing indices for July, i.e. the Empire State Index (Wednesday) and the Philadelphia Fed Index (Thursday), as well as some key activity indicators for June such as the retail sales (Thursday), the housing starts and the industrial production (Friday).

Elsewhere, the main highlights include China Q2 GDP and the related activity indicators for June (retail sales, industrial production, fixed investments) on Wednesday and the BoC monetary policy meeting on the same day (BoC is expected to keep rates unchanged at 2.25%).

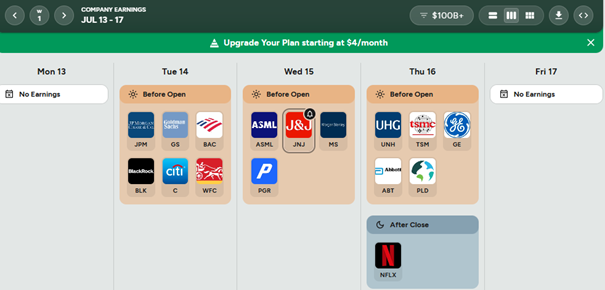

Finally, US banks will kick off the Q2 earnings season, starting with JPM, BofA, GS, WFC and Citigroup on Tuesday. Other big corporates announcing results feature ASML, TSMC, Netflix, J&J, MS and GE (see the non-exhaustive table here below).

https://earningshub.com/earnings-calendar/week-of/2026-07-13

This is a marketing communication issued by DECALIA SA. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The information and data presented in this document are not to be considered as an offer or invitation to buy or sell any securities or financial instruments nor to subscribe to any services. The information, opinions, estimates, calculations etc. contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Investments in any securities or financial instruments may not be suitable for all recipients and may not be available in all countries. This document has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Before entering into any transaction, investors should consider the suitability of the transaction to individual circumstances and objectives. Any investment or trading or other decision should only be made by the client after a thorough reading of the relevant product term sheet, subscription agreement, information memorandum, prospectus or other offering document relating to the issue of the securities or other financial instruments. Where a document makes reference to a specific research report, the document should not be read in isolation without consulting the full research report, which may be provided upon request.