We aren’t yet out of the woods. That’s true both for the Cagliari Calcio, who lost logically against Inter on Friday evening, as well as for the energy shock resulting from the conflict in Iran. However, in both cases, the relief observed since the previous week-end thanks to the victory against Cremonese and the fragile ceasefire, respectively, makes sense as they narrowed the distribution of possible outcomes. In other words, they reduced the negative fat tail probabilities! In the meantime, markets continue to be driven mainly by energy prices moves: equities and bonds down when oil prices are up, with the greenback benefiting somewhat and credit & gold suffering in this context; and vice versa!

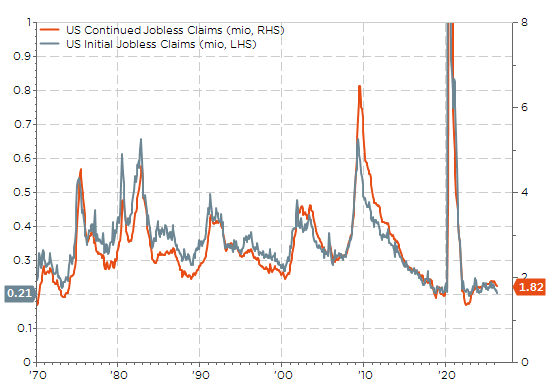

As a result, this sloppy and fragile ceasefire marked an inflexion point as the worse seems behind us, paving the way for markets to refocus on fundamentals rather than being almost exclusively driven by oil price volatility. It thus allowed equity markets to make new all-time high, helped by resilient economic activity data so far and a strong start of earnings season. In this context, US banks results showed broad based double-digit average earnings growth, supported by robust loan growth but also trading and banking activities, Tier-1 ratio in a continuing improvement trend, which also demonstrates some form of discipline without any credit quality deterioration despite ongoing easing lending standard and capital redeploying. Turning back to the economic data, US weekly initial and continuing jobless claims have been stuck just above 200k and 1’800k respectively over the last 6 weeks.

Weekly initial jobless claims & continued claims: a comforting view

Conscious that the labor market is often a lagged economic indicator, the manufacturing sector -usually considered as la leading indicator of the business cycle- is also showing a surprising resilience according to our US ISM manufacturing index proprietary model. Based on the Empire and Philadelphia Fed mfg regional indices, which were released last week, the US ISM mfg index is forecasted to increase further in April (the official data will be released on May 1st), well above the 50 threshold’s level separating contraction to expansion in industrial activity. If it really happens, it may add another layer of upward pressures on US rates and comfort Fed’s current wait and see stance, with absolutely no hurry to cut rates. Note that US industrial sector is also benefitting from structural tailwinds such as re-shoring, as well as AI capex and subsequent infrastructure boom -quite insulated from the negative energy shock as long as it doesn’t morph into a more severe growth or financial crisis-.

US ISM Manufacturing proprietary model: still defying gravity

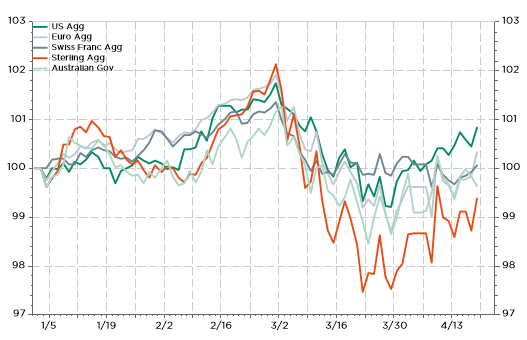

Considering the fixed income market, bonds have recovered only about half of the last month losses, which is consistent with the fact that the blockade of the Strait of Hormuz won’t be resolved soon in the sense that even assuming a rapid & strong peace deal, without further energy infrastructure damages, it will take several weeks to restore normal energy flows in the region and several months for the world energy markets to get back close to a pre-conflict situation. As a result, energy prices may hang around current levels of $90 per barrel for quite a long time. The good news is that the fragile ceasefire and the subsequent decrease of oil barrel below $100 has removed the urgency for most central banks, especially in Europe, to hike. The bad news, with energy prices at current levels for longer and significant disruptions to the supply chain, is that there will clearly be a lasting impact on the rates structure given that inflation will also remain stickier, above central banks’ target, for longer.

Selected Aggregate Bond Indices: a half recovery

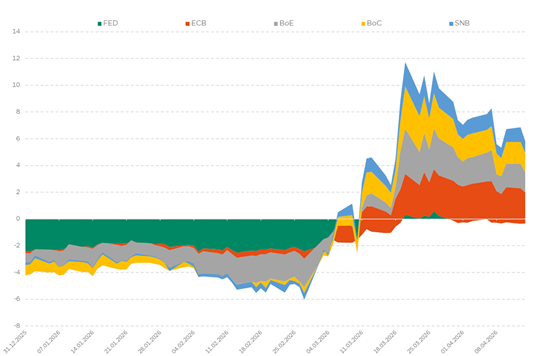

Expectations of major central banks rate cuts/hikes by year-end:

a less dramatic repricing than one month ago but still a far away from the good place prevailing before the conflict

So, central bankers will continue to have some headaches in the next few weeks. In one hand, they are now tempted to dial down the urgency of a monetary response in order to avoid a disorderly de-anchoring of inflation expectations. On the other hand, term premium may creep up if they don’t act (or cut too soon for the Fed) whereas energy prices spike again and/or… economy proves much more resilient than expected. Framing a long term desire to lower rates while acknowledging that current conditions do not necessarily justify imminent cuts will be indeed the first challenge of the next Fed Chairman. In this context, it’s probably wiser to continue to favor carry in the belly of the curve with IG credit quality, including peripheral govies such as Italy, Spain or France despite the political risks ahead.

Economic Calendar

While investors will continue to focus on the “reliability” of the US-Iran ceasefire -officially set to expire on Tuesday-, the main event could be the Senate confirmation hearing of Kevin Warsh as new Fed Chairman (Tuesday) given the implications it may have for the conduct of the US monetary policy in the months and years ahead.

Moving to economic data, key highlights include the US retail sales for March (still on Tuesday) as well as the flash global PMI indices for April on Thursday. Note that US retail sales are expected to jump in excess of +1.0% MoM in March as they will be lifted by the marked increase in gasoline prices… as these figures are released in nominal terms! As a result, the control group (excluding auto, gas & food), which feeds directly into GDP calculus, is likely to exhibit a much sober gain (+0.2% expected). On top of the flash PMI manufacturing and services headline figures, investors will also scrutinize the price components and other sub-indicators signaling potential disruptions due to the ripple effects from the war.

Speaking about prices, several inflation reports will be released across the world this week but two of them may be particularly important given how topical this issue has become over the last few years in these countries: the UK CPI (Wednesday) and Japan CPI (Friday). In this context, these figures may influence quite directly the next BoE and BoJ monetary policy decisions, which will take place as soon as the following week. Finally, we will get two sentiment indicators from Germany: the ZEW survey (Tuesday) and the Ifo survey (Friday)

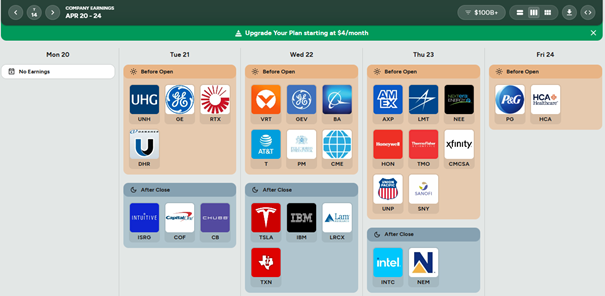

To conclude with the earnings season (see a non-exhaustive list at the end of this email), it will start to be packed and busy with many big caps reporting from different sectors, including Tesla, Intel, SAP, P&G, Blackstone, Amex, Lockheed Martin, Halliburton or Freeport-McMoRan to name a few.

https://earningshub.com/earnings-calendar/week-of/2026-04-20

This is a marketing communication issued by DECALIA SA. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The information and data presented in this document are not to be considered as an offer or invitation to buy or sell any securities or financial instruments nor to subscribe to any services. The information, opinions, estimates, calculations etc. contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Investments in any securities or financial instruments may not be suitable for all recipients and may not be available in all countries. This document has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Before entering into any transaction, investors should consider the suitability of the transaction to individual circumstances and objectives. Any investment or trading or other decision should only be made by the client after a thorough reading of the relevant product term sheet, subscription agreement, information memorandum, prospectus or other offering document relating to the issue of the securities or other financial instruments. Where a document makes reference to a specific research report, the document should not be read in isolation without consulting the full research report, which may be provided upon request.