Now that the Serie A season is drawing to a close and Cagliari Calcio has officially secured survival after yesterday’s 2-1 victory against Torino, it is time to look ahead… And there will be no shortage of sporting distractions over the coming weeks: the ATP Gonet Geneva Open, followed by Roland-Garros, the NBA Finals, the Champions League final, and the FIFA World Cup fast approaching (opening match on June 11).

For the nostalgic among us, Roland-Garros was -and still is- an important milestone, or rather a major distraction, for every sports-loving student: landing right in the middle of exam revision periods, which inevitably suffered greatly because of it (at least in my days), it also signaled the arrival of summer and the sense that holidays were finally just around the corner.

And, much like back then, these major sporting events will coincide with a number of equally important developments from a geopolitical perspective (including the top-of-mind potential reopening, or not, of the Strait of Hormuz), alongside crucial macroeconomic data on growth and inflation. All of this will culminate by mid-June with the G7 meeting in Evian and a fireworks’ display of central bank meetings, highlighted by Warsh’s first appearance as the new Chairman of the Fed.

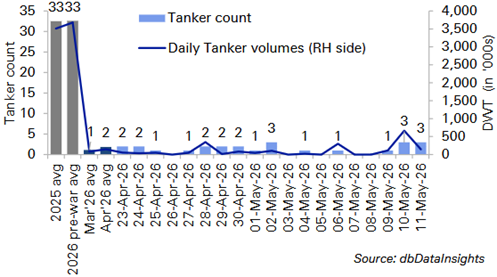

Indeed, the ECB will meet on June 11, followed by the BoJ on June 16, the Fed on June 17, and both the BoE and the SNB on June 18. And there is a strong chance that at least three of them (namely the ECB, the BoJ and the BoE) could deliver a +25bps hike, especially if the Strait of Hormuz remains partially blocked by then. As a reminder, even once maritime traffic resumes, it would still take roughly two weeks to restore normal shipping flows and another four to six weeks for cargos to reach refineries and feed through the global supply chain.

Tanker activity exiting the Strait of Hormuz

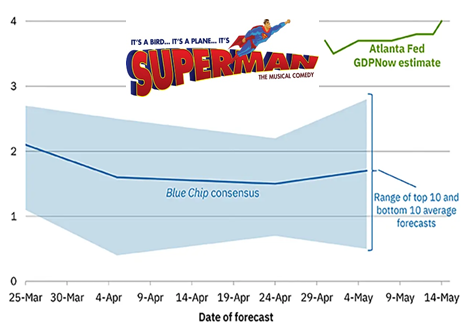

This comes at a time when macro data continue to prove surprisingly resilient. Global manufacturing activity remains supported by powerful structural trends (AI-related capex, energy infrastructure spending and defense investment) all of which are being amplified by fiscal support and public spending programs. Meanwhile, the US consumer is still benefiting from a remarkably low unemployment rate (4.3% in April along some net jobs creation), plus tax relief measures and targeted subsidies linked to the OBBBA. As a result, the Atlanta Fed GDPNow model forecasts +4.0% real US GDP growth a.r. for this quarter, on the back of recently released stronger than expected US retails sales and industrial production readings.

Atlanta Fed GDPNow real GDP estimate for 2026_Q2: it’s a bird, it’s a plane, no it’s the US economy!

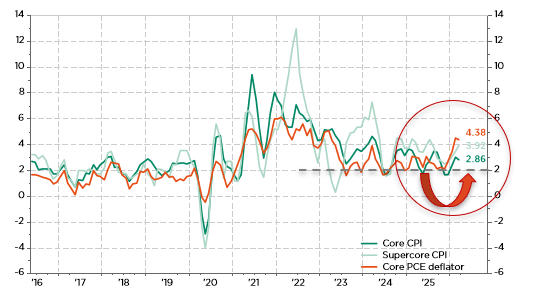

Against this backdrop, headline inflation is likely to continue moving higher, with the next inflation prints due just ahead of the central bank meetings. Core inflation measures have also tended to surprise on the upside recently. In the US in particular, the 3-month annualized pace of several “supercore” inflation gauges (i.e. excluding the most volatile energy and food components) has moved back decisively above the symbolic 2% threshold, reinforcing the view that underlying price pressures remain sticky.

Q/Q% a.r. in US core inflation, supercore & core PCE

In this environment, the upcoming leadership transition at the Fed could prove particularly challenging for Kevin Warsh. Much like a top athlete preparing for a major final or event, he will need to spend the coming weeks carefully building credibility and internal consensus. He will notably have the difficult task of aligning the Committee around the policy statement – especially after the last meeting revealed three dissents favoring a more neutral stance rather than the prevailing dovish bias. He will then face what is likely to be an especially sharp press conference and Q&A session, made even more sensitive by the release of updated economic projections and the closely watched dot plot.

As central banks prepare to step back onto the court next month, markets are now finally starting to price how the macro backdrop dynamics may change. For months, investors have been pricing a fairly comfortable rally, driven essentially by AI boom and the semiconductors and other hardware benefiters , but also -more importantly- resilient growth, eventual disinflation and the prospect of easier monetary policy. But the game may now be entering a far more physical and tactical phase.

Because while growth remains surprisingly solid, inflation is refusing to stay inside the lines. Supply-side tensions linked to the Strait of Hormuz, structurally strong capex cycles and persistent labor market tightness are all keeping pressure on prices and thus pushing again yields higher. In other words, the equity rally may not be over – but the central banks’ “unforced errors” margin is becoming increasingly thin, whereas the interest rate gravity is adding a ceiling glass.

This is precisely where the Fed’s upcoming transition matters. Just like a player suddenly inheriting Centre Court expectations midway through a Grand Slam, Kevin Warsh could find himself under immediate pressure to deliver both consistency and authority. Markets will scrutinize every sentence of the statement, every nuance of the dot plot and every answer during the press conference. One poorly timed shot, one communication mistake, and volatility could rapidly regain the upper hand. And unlike tennis, central banking does not allow challenge reviews once credibility is lost. So yes: be ready for some hikes, smashes and kicks… but beware of own goals and uprisings. Because in this late stage of the cycle, monetary policy is no longer a smooth baseline rally. It is becoming a tie-break played in increasingly difficult conditions, with markets oscillating between aggressive positioning and sudden risk aversion.

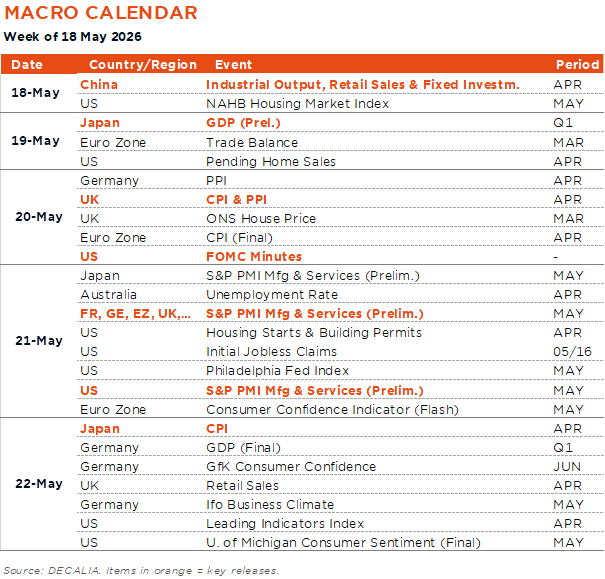

Economic calendar

This week’s key economic indicators include the Chinese economic activity indicators, which were released this morning (more below), Japan Q1 GDP preliminary reading (Tuesday), April inflation in UK (Tuesday) and in Japan (Friday), as well as the global flash PMI indices for May (Thursday). Investors will obviously remain focused on the impact of the Iran conflict and higher energy prices on business activity and prices dynamics. So far, manufacturing is still booming on the back of structural trends (AI capex, energy infrastructure, defense) as illustrated last Friday with better than expected US industrial production data (+0.7% in April vs. +0.3% expected) or a further increase in Empire manufacturing index in May (up to 19.6 from 11.0, while consensus expected a reading of 7.0), whereas the services activity seems slowing down.

In China, activity data came a bit weaker but remain in line with previous months trends: sluggish retail sales and domestic demand, weak fixed investment and especially real estate sector and an overall more resilient industrial production, driven by strong exports growth (in industrial sales for export accelerated to a 46-month high of 10.6% YoY).

In Japan, Q1 real GDP is expected to accelerate somewhat from the previous quarter to +0.4% from +0.3% QoQ, whereas nominal GDP growth should stay quite stable around +0.8%-0.9% QoQ (with GDP deflator remaining above 3% yoy). Speaking about prices in Japan, April CPI will be released on Friday. The consensus foresees core CPI inflation excl. fresh food and energy ticking down but remaining above 2% (2.4% in March) and closer to 3% when stripping out administered prices of the core inflation (this is a new prices gauge introduced and followed by the BoJ since the beginning of the year in order to closely monitoring the underlying trend of inflation).

Moving on to Europe, but still speaking about an economy suffering chronically from a higher inflation than elsewhere in DM, the UK CPI will be released on Tuesday. The consensus points to a… decrease in the inflation annual rate, due to an important base effect, in spite of a widely expected MoM acceleration. As a result, headline and core CPI should drop to 3.0% and 2.6% in April, respectively, from 3.3% and 3.1%. In Germany, the Ifo survey for May will be due on Friday.

Finally, in the US, the calendar will be rather quiet. The main economic data releases feature the housing starts and building permits for April, the Philadelphia Fed mgf index and the final reading of University of Michigan consumer sentiment for May. More importantly, we will get the FOMC minutes on Wednesday.

Wrapping up as usual with the earnings season, which is now really coming to an end, Nvidia’s results (Wednesday) will be closely watched, as well as the earnings from big US retailers (Walmart, Home Depot and TJX).

This is a marketing communication issued by DECALIA SA. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The information and data presented in this document are not to be considered as an offer or invitation to buy or sell any securities or financial instruments nor to subscribe to any services. The information, opinions, estimates, calculations etc. contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Investments in any securities or financial instruments may not be suitable for all recipients and may not be available in all countries. This document has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Before entering into any transaction, investors should consider the suitability of the transaction to individual circumstances and objectives. Any investment or trading or other decision should only be made by the client after a thorough reading of the relevant product term sheet, subscription agreement, information memorandum, prospectus or other offering document relating to the issue of the securities or other financial instruments. Where a document makes reference to a specific research report, the document should not be read in isolation without consulting the full research report, which may be provided upon request.