The energy crisis is deepening as fighting in the Middle East intensifies. Iran has proven more resilient than expected, effectively managing a difficult situation with a government that remains organized and cohesive. By refusing to pursue de-escalation, Tehran is increasing pressure on the United States.

The well-known “TACO trade” (“Trump Always Chickens Out”) may not apply in this case. President Trump can no longer unilaterally declare an end to the conflict, nor can he single-handedly reopen the Strait of Hormuz or quickly restore damaged energy infrastructure. This creates a strategic imbalance for the United States and its allies, given Iran’s advantage in the Strait. Washington faces a limited set of difficult options: declare victory and withdraw, effectively leaving the Strait under Iranian influence; engage in a ground military operation to secure control—an option that carries significant risks for energy infrastructure and could further disrupt oil and gas prices; or pursue a compromise, which is likely to become increasingly favorable to Iran as time passes. Meanwhile, Russia is likely observing the situation with some satisfaction. Rising energy prices, combined with a temporary easing of its oil embargo, are boosting its revenues and helping sustain its war effort in Ukraine—an issue that may now receive less immediate attention from the United States and its allies.

In this context, the prospect of a short, contained conflict followed by rapid de-escalation now appears unlikely. Instead, more disruptive scenarios are emerging, with significant implications for energy prices, trade flows, global growth, and inflation in the months ahead. So far, markets have reacted swiftly, pricing in the inflationary impact of such supply shocks and the potential consequences for global monetary policy.

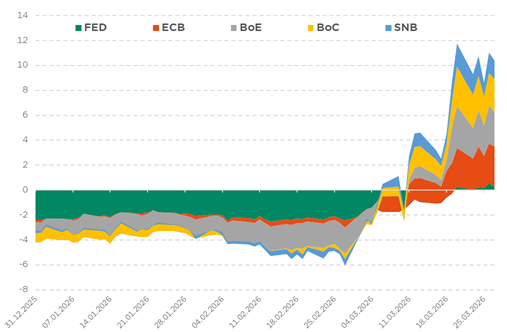

A dramatic repricing away from the “good place”: expectations of rates cuts by year-end

While investors still (rightly) question whether the Fed will raise rates in the coming months—given several factors such as its dual mandate amid a softening US labor market, the relatively lower impact of the energy shock on the US compared to Europe, and the fact that US monetary policy was not particularly accommodative before the conflict—there has nonetheless been a sharp repricing of the global monetary policy path for the remainder of the year.

It is worth emphasizing that this environment further complicates central banks’ task of delivering the right dose of policy at the right time. Monetary policy is not well suited to address supply-side shocks, making the situation particularly challenging. Central banks have generally adopted a more hawkish tone, influenced by the legacy of 2022, and—for now—appear relatively unconcerned about the potential spillover effects on economic activity. Yet, as is well understood, “higher-for-longer” rates also represent a significant headwind for both financial markets and the broader economy.

A tipping point may eventually emerge, at which central banks shift their focus more decisively toward growth concerns. In the meantime, investors are grappling with how much further long-end rates can rise, knowing that beyond a certain level, tighter financial conditions will begin to undermine growth and, ultimately, dampen inflationary pressures. This suggests a somewhat paradoxical conclusion: the more hawkish central banks become—potentially even delivering outsized rate hikes—the more this may act as a stabilizing force for long-end yields.

The next phase could therefore involve a transition in investor concerns, from an inflation shock to a growth shock. Such a shift would likely be marked by a return to negative correlation between bonds and equities—where equities sell off while bonds rally (i.e., yields decline). At that point, the front end of yield curves would likely become more anchored, as investors begin to look beyond what is increasingly perceived as a transitory inflation shock.

Let us conclude with a few observations on gold, the US dollar, and portfolio diversification more broadly. So far, gold has not behaved as a safe haven—unsurprising in an environment characterized by liquidity stress and tightening financial conditions. It has been affected by investor deleveraging, particularly among more speculative participants, as volatility has increased. Historical patterns show that during the most acute phases of past crises, gold prices often declined before eventually resuming their upward trend. In addition, while emerging market central banks had been significant buyers of gold in recent years, they have turned into net sellers in the current environment, as they seek to raise liquidity to defend their currencies. Finally, this shock has pushed interest rates higher, which—combined with a stronger US dollar—creates an additional headwind for gold. As long as rates remain elevated and the dollar firm, a sustained rebound in gold is likely to remain challenging.

In contrast, the US dollar has reasserted itself, at least to some extent, as an effective portfolio diversifier. The US is currently perceived as a relative “winner,” while traditional safe-haven assets—such as bonds, gold, or even the Japanese yen and Swiss franc—have proven less reliable in this particular episode. This underscores the importance of understanding the nature of the shock when constructing hedges: today’s environment is more complex, and asset behavior is not driven solely by real economic growth.

Looking ahead, a renewed weakening of the US dollar will depend on several factors, including the trajectory of energy prices and whether the Fed moves more quickly than other central banks to cut rates—potentially in response to fragilities in the US labor market. As for the Japanese yen, it could regain its safe-haven appeal in future risk-off episodes, provided the Bank of Japan does not remain overly accommodative for too long and some degree of fiscal credibility is restored. For now, however, the yen has struggled to act as a diversifier in the context of an oil shock, as rising rates and unfavorable terms of trade weigh on the Japanese economy—unlike the case for the US dollar. In conclusion, both investors—and to a lesser extent central banks—appear to be suffering from a form of short-term myopia. The current focus remains overwhelmingly on the immediate inflation shock and the prospect of higher interest rates, as if these dynamics were the final destination rather than part of a broader cycle. Yet, markets rarely stop at the first-order effects. Once investors begin to look beyond this “wall” of inflation and higher rates, the narrative is likely to shift meaningfully. The second-order consequences—namely weaker growth and tighter financial conditions—could come back into sharper focus. In such an environment, market reactions would likely differ significantly from what we observe today: equities and credit could face renewed and potentially stronger pressure, while other asset classes may regain their role as effective diversifiers.

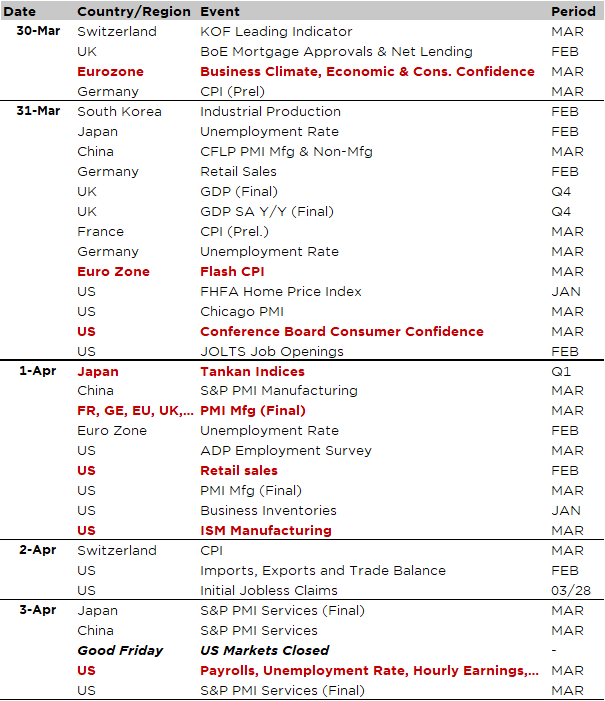

Economic Calendar

Goodbye March Madness and welcome April… fools? While we will finally leave an epic and furious first quarter, I doubt we will have time to rest yet as markets will still have to contend with a busy economic calendar this week, on top of the still perilous geopolitical context.

For sure, the impact of the Iran conflict will continue to be front and center next week, but the investors focus will start shifting back to the economic backdrop as indicators for March will now come through. The US jobs report will be the key highlight but note that it will be released on the Good Friday, when US markets will be closed. The consensus expects payrolls monthly change to bounce back in positive territory (+55k) after the -92k drop in February, with unemployment rate and wages growth basically unchanged at 4.4% and +0.3% MoM respectively. We will also get the ISM manufacturing on Wednesday, which should remain in expansionary territory (i.e. above 50) according to both the consensus and our own proprietary model based on regional indices; as well as the Conference Board’s consumer confidence on Tuesday, which must have taken a hit a hit with soaring energy prices, higher mortgages rates and falling equity markets. Other usually important economic data, such as retail sales or the JOLTS job openings will be somewhat dismissed as they cover the month of February Elsewhere, the flash CPIs for March will be the main focus in Europe on Monday and Tuesday, whilst in Asia the spotlight will be on the PMI indices in China and Japan on Wednesday (manufacturing) and Friday (services), as well as the comprehensive quarterly Tankan survey in Japan covering small and large companies in both the manufacturing and services sectors (Wednesday).

This is a marketing communication issued by DECALIA SA. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The information and data presented in this document are not to be considered as an offer or invitation to buy or sell any securities or financial instruments nor to subscribe to any services. The information, opinions, estimates, calculations etc. contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Investments in any securities or financial instruments may not be suitable for all recipients and may not be available in all countries. This document has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Before entering into any transaction, investors should consider the suitability of the transaction to individual circumstances and objectives. Any investment or trading or other decision should only be made by the client after a thorough reading of the relevant product term sheet, subscription agreement, information memorandum, prospectus or other offering document relating to the issue of the securities or other financial instruments. Where a document makes reference to a specific research report, the document should not be read in isolation without consulting the full research report, which may be provided upon request.